Managing Other People’s Money: A Practical Playbook for Mandates, Risk Budgets, and Client Trust

Managing outside capital sounds like an investing job. In practice, it is just as much a governance job.

Clients rarely leave in the easy months. Relationships usually break when losses expose something softer and more dangerous: vague objectives, sloppy benchmarks, unclear discretion, or communication that only starts after the damage is done. The hard part is not just choosing securities. It is building a mandate and risk framework you can still defend when performance is weak.

A good process does not guarantee good outcomes. Markets do not offer that bargain. What it can do is reduce avoidable mistakes, make risk-taking easier to understand, and keep clients from discovering your real rules in the middle of a drawdown.

Managing other people’s money is a governance job first

The product is not returns alone. It is a process the client can understand, evaluate, and live with.

That matters because most portfolios look coherent when markets cooperate. The real test comes later. If a client asks, “Was this loss expected under the mandate, or did you quietly change the game?” a performance chart is not enough.

This is the central truth: your mandate, risk budget, and communication system matter most when returns are least flattering. An Investment Policy Statement and a benchmark are not paperwork. They are anti-improvisation tools. They define what the portfolio is trying to do, what kind of pain is acceptable, and where discretion ends.

That is why fiduciary process tends to emphasize suitability, documentation, consistency, and clarity rather than outcome guarantees.[^1][^2] Good governance will not rescue a bad strategy. But weak governance can ruin a sound one.

Start with an IPS that constrains behavior, not one that decorates a file

A weak IPS is broad enough to justify almost anything. A useful IPS narrows the field before pressure arrives.

At minimum, it should spell out the parts that actually govern decisions:

- objective and return need

- time horizon

- liquidity needs

- tax considerations

- legal or regulatory constraints

- eligible and prohibited investments

- diversification and concentration limits

- benchmark choice

- rebalancing policy

- roles, authority, and reporting responsibilities

Professional guidance on IPS design consistently treats these as core because they turn goals into rules, not just preferences.[^3]

The minimum fields that actually matter

The important distinction is not whether the IPS is long or short. It is whether it reduces ambiguity.

“Long-term growth with moderate risk” is not a usable instruction. It sounds reasonable, but it leaves almost every hard judgment unanswered. Moderate relative to what? How much drawdown is tolerable? Is the account benchmark-aware or outcome-aware? Are illiquid assets allowed? Do taxes shape trading decisions?

A more useful version is less elegant and far more practical: preserve purchasing power after withdrawals, keep twelve months of expected liquidity needs in short-duration instruments, avoid single-issuer exposure above a stated limit, and evaluate active equity decisions against a benchmark aligned with the investable universe.

That kind of language gives everyone less room to improvise.

Choose a benchmark that fits the mandate, not one that flatters the manager

Benchmark choice is often treated as an administrative detail. It is not. The benchmark shapes expectations, active risk, attribution, and even what counts as success.

If you run a benchmark-aware U.S. equity mandate, a broad index such as the Russell 3000 or S&P 500 may make sense, depending on the actual universe. If you run an income-focused taxable family portfolio, that same benchmark may mislead. A blended policy benchmark, or one tied to required distributions and capital preservation, may be more honest.

A flattering benchmark is more dangerous than a demanding one. It can make the portfolio look skilled while quietly distorting construction and risk-taking.

Write clauses that still work in bad markets

Bad markets expose soft language. Strong IPS drafting anticipates that.

Useful clauses answer questions like:

- What happens if liquidity needs rise suddenly?

- Can cash levels move meaningfully off target?

- Who can approve a temporary breach?

- When does a tactical overweight become a mandate change?

- How quickly must a breach be reviewed or reported?

The point is not legal theater. It is to keep the portfolio from becoming a moving target under stress.

What weak language sounds like

Weak: “The portfolio may invest flexibly across asset classes to pursue attractive risk-adjusted returns.”

Useful: “The portfolio may deviate from policy weights within pre-defined ranges. Deviations outside those ranges require documented approval, stated rationale, and a review date.”

The first preserves freedom. The second preserves trust.

Turn client goals into a risk budget the strategy can actually respect

A return target describes what the client wants. A risk budget describes what the portfolio is allowed to endure while pursuing it.

That sounds obvious, but many mandates still treat risk as a single number detached from strategy design. A better approach is to choose the risk measure that fits the actual job.

When volatility is useful and when it is not

Volatility is useful when return variability itself matters, the portfolio is reasonably diversified, and the strategy is not tightly benchmark-relative. It is common because it is measurable and comparable.[^4]

Its weakness is just as important. Volatility does not tell the client how bad a path can feel. It can understate tail risk, liquidity stress, and the emotional reality of a fast 15% loss.

Tracking error for benchmark-aware mandates

For benchmark-aware portfolios, tracking error is often the more relevant primary measure because it asks a cleaner question: how far is the portfolio allowed to deviate from its benchmark?[^5]

That fits an active U.S. equity mandate much better than a generic volatility cap. In that setup, the client often cares less about total market noise than whether active decisions stayed within the expected range of benchmark-relative risk.

Maximum drawdown for clients who feel risk in dollars, not standard deviations

Some clients do not experience risk as annualized variance. They experience it as capital impairment, spending disruption, or an account value they cannot emotionally or practically absorb.

In those cases, drawdown framing can be more intuitive. But it has a trap. Drawdown controls can become procyclical if they force de-risking after losses without clear rules. If drawdown is central, the mandate should define what action follows, who decides, and whether breaches trigger immediate trades or formal review.

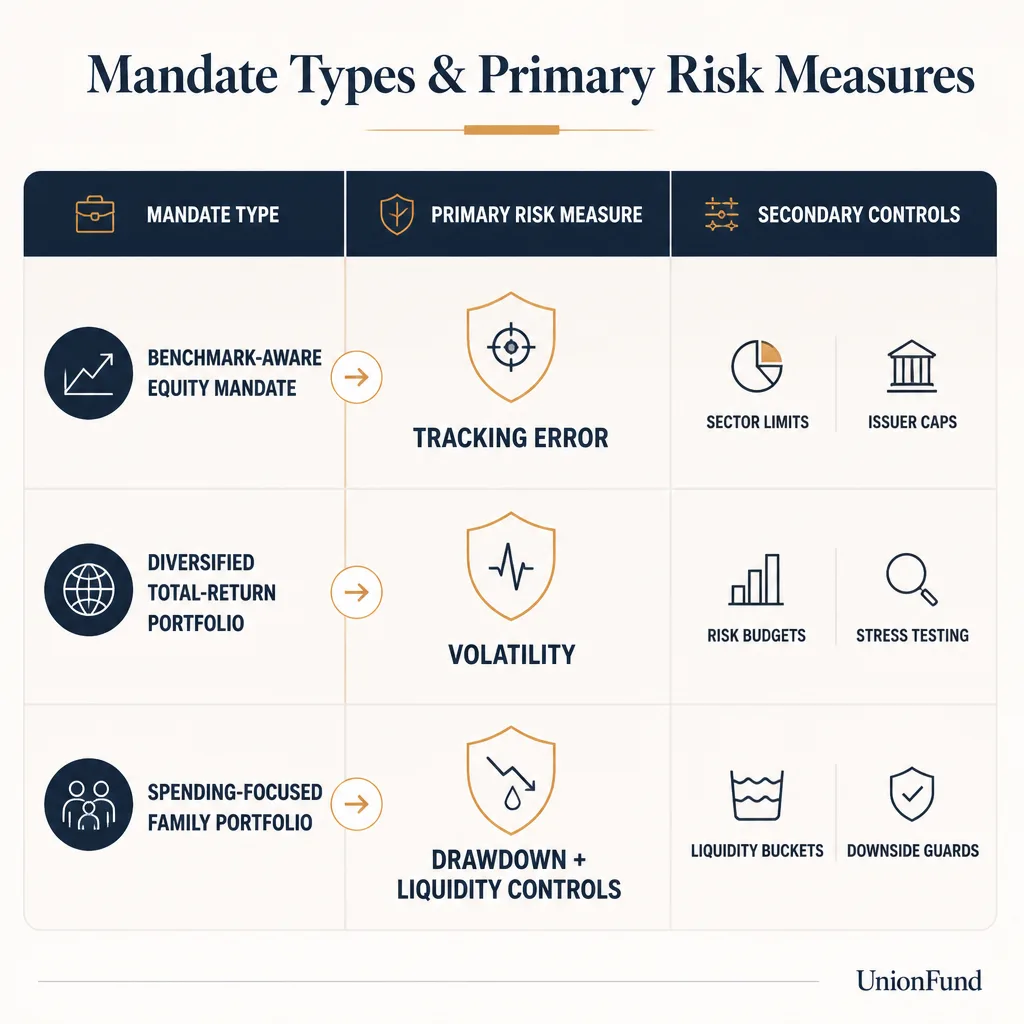

Match the metric to the strategy

A simple way to think about it:

- benchmark-aware equity mandate: tracking error first, with concentration and sector guardrails

- diversified total-return portfolio: volatility as the main lens, with liquidity and stress-test overlays

- family portfolio with spending needs: drawdown and liquidity may matter more than benchmark-relative risk

One metric is rarely enough. In practice, a primary measure usually works best when paired with secondary controls such as issuer caps, liquidity buckets, stress testing, or leverage limits.

Add ranges, escalation triggers, and breach protocols

A risk budget should not be a number floating in a slide deck. It needs operating rules.

That usually means defining:

- a target range rather than a point estimate

- what counts as a breach

- who gets notified

- whether market-driven breaches are treated differently from intentional ones

- how exceptions are documented

- when the position must be reviewed again

This is where measurement becomes governance.

Position sizing is where philosophy becomes exposure

Every manager says they believe in discipline. Position sizing is where that belief becomes visible.

Use limits that reflect both conviction and liquidity

Even strong ideas need containment. Common controls include single-name limits, sector or industry caps, country limits where relevant, and sizing rules tied to actual liquidity rather than theoretical exit assumptions.

That last point matters more than many managers admit. Liquidity is not just a security characteristic. It is a portfolio characteristic. A portfolio full of individually tradable assets can still become hard to adjust if the client needs cash quickly or if correlated positions all need to move at once.

Define when discretion is allowed

Discretion should not be informal. It should be pre-defined.

A practical rule is simple: if a manager can override a limit, the IPS or mandate should say under what conditions, who approves it, how long it can last, and when it must be revisited. Otherwise, “temporary flexibility” turns into silent process drift.

Concentration usually creeps in

Concentration rarely arrives as one dramatic trade. It usually builds through appreciation, repeated exceptions, benchmark changes, or correlated exposures disguised as diversification.

A portfolio can hold 40 securities and still be one macro bet. That is why look-through exposure and factor awareness matter, especially when using funds, derivatives, or strategies with embedded leverage.

Pre-commit against hidden leverage and correlated bets

Hidden leverage is broader than borrowing. It can sit in derivatives, structured products, short-volatility exposure, leveraged funds, or a portfolio built around the same economic driver in different wrappers.

Pre-commitment helps. Define gross and net exposure limits where relevant. Require look-through reviews. Stress-test the portfolio against a few obvious regimes. You are not trying to predict every shock. You are trying to avoid being surprised by your own exposures.

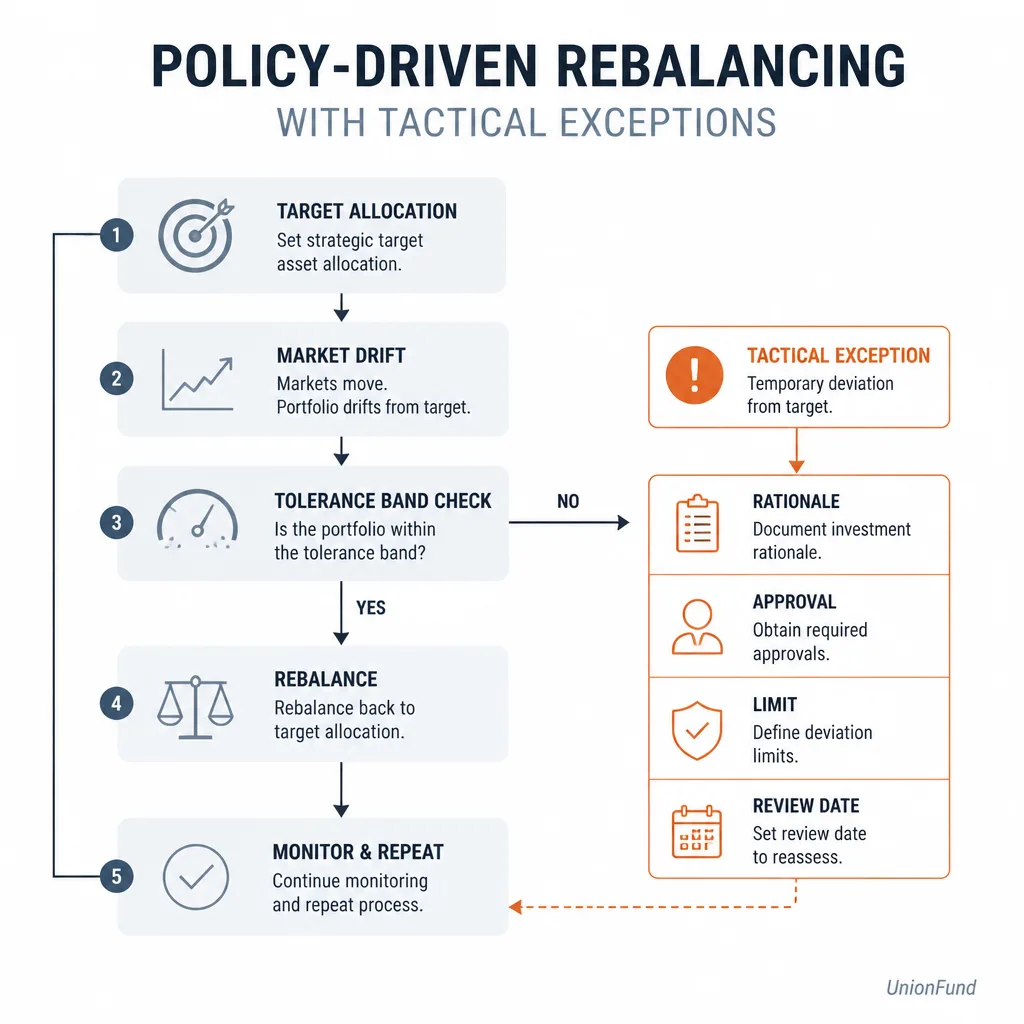

Rebalancing should be policy-driven, with tactical deviations treated as exceptions

Rebalancing is one of the clearest places where process either exists or it does not.

Calendar-based versus threshold-based rebalancing

Calendar rebalancing is simple. Threshold-based rebalancing is often more sensible because it reacts when weights actually drift.[^6] In taxable accounts, the answer gets more complicated. Taxes, realized gains, and cash-flow needs may matter as much as pure allocation discipline.

So the question is not which method is universally best. It is which method fits the account.

When tactical deviations are justified

Tactical deviations can be legitimate. But they should be treated as exceptions to policy, not a quiet replacement for it.

That means the deviation needs a rationale, a sizing limit, and a review date. If it does not expire or get re-approved, it is not tactical anymore. It is just drift with a better label.

How to document temporary overweights or underweights

Keep it plain:

- what changed

- why it changed

- what limit was overridden, if any

- how long the deviation is expected to remain

- what would cause reversal or extension

A short exception memo is often more useful than a long narrative no one revisits.

Do not let market narratives replace policy

Every market cycle produces a story that seems too obvious to ignore. That is exactly when policy matters most. Narratives are persuasive because they arrive with social proof. Policy is useful because it does not care.

Performance reporting should separate outcome from process

Clients need performance reporting. They do not only need performance reporting.

What to include beyond returns

A useful report typically includes:

- returns and benchmark context

- attribution

- risk taken

- mandate compliance

- notable positioning changes

- any breaches, exceptions, or unresolved issues

If you report only returns, clients are forced to infer process from outcomes. That is a poor habit in a noisy business.

Standards such as GIPS help formalize fair presentation and consistency, even if many client reports go beyond strict standards language.[^7]

Explain underperformance without sounding defensive

A good framework is blunt and calm:

- what happened

- whether it was consistent with the strategy’s expected behavior

- what, if anything, has changed in the process or thesis

That is usually better than trying to win the argument with macro commentary.

Clients need to know whether the process worked

A benchmark-aware strategy can underperform for valid reasons. An income portfolio can lag equities in a rally for valid reasons. The point of reporting is not to excuse outcomes. It is to help the client distinguish expected behavior from broken behavior.

More reporting does not automatically build more trust. Cleaner reporting usually does.

Client trust is built between drawdowns, then tested during them

Trust is rarely created in the middle of a bad quarter. By then, you are collecting on expectations you either set properly or did not.

Set the communication cadence before stress arrives

Set the cadence early. Monthly reporting, quarterly calls, and explicit protocols for unusual market stress are often more useful than ad hoc outreach that appears only when losses become uncomfortable.

The habit matters because silence gets interpreted. Usually badly.

What to say during drawdowns

During difficult periods, clients usually need three things:

- what happened

- whether the portfolio behaved within the expected rules

- what actions, if any, the process now requires

A simple example: “The portfolio’s underperformance came mainly from active sector positioning and stayed within the expected range of benchmark-relative risk. No mandate limits were breached. We reduced one position due to revised liquidity assumptions, not because the policy changed.”

That is clearer than reassurance without substance.

What not to say when clients are anxious

Avoid vague optimism. Avoid pretending short-term pain is irrelevant. Avoid language that implies the rules are being rewritten midstream.

Clients can tolerate losses better than they can tolerate the feeling that nobody is steering.

Pre-commitment reduces reactive decisions on both sides

Pre-committed rules are not just for managers. They also protect clients from making permanent decisions based on temporary stress. Behavioral finance has long shown that losses are experienced asymmetrically.[^8] Good communication design works with that reality instead of pretending it away.

The common failure modes are usually visible before they become fatal

Most portfolio failures do not begin as disasters. They begin as exceptions no one wants to classify as exceptions.

Style drift is often just a series of “temporary” choices made under performance pressure.

Hidden leverage usually starts as a more efficient expression, not an explicit decision to take dangerous risk.

Concentration creep often comes from winners, not fresh conviction.

Liquidity mismatch shows up when portfolio terms and client cash needs were never properly reconciled.

Benchmark mismatch quietly poisons attribution and expectations long before anyone names it.

Process drift is the deepest problem of all. It is what happens when a bad stretch turns policy into suggestion.

These are technical failures on the surface. Underneath, they are governance failures.

A defensible investment process is the best form of client service

The cleanest operating framework is also the most durable one.

Define the mandate precisely. Choose a benchmark that fits the job. Match the risk budget to the strategy instead of forcing a universal metric. Put real rules around position sizing, rebalancing, and discretion. Document exceptions. Communicate before trust is needed, not after it starts to erode.

Managing other people’s money will always involve uncertainty. The point of good process is not to remove that uncertainty. It is to make sure the uncertainty belongs to markets, not to your own behavior.

FAQ

What is the most important document when managing other people’s money?

Usually it is the Investment Policy Statement, or IPS. A strong IPS does more than summarize goals. It defines objectives, time horizon, liquidity needs, constraints, benchmark choice, and the rules that limit improvisation when markets get difficult.

How is a risk budget different from a return target?

A return target describes what the client wants. A risk budget defines how much uncertainty, benchmark deviation, or drawdown the portfolio can reasonably absorb while pursuing that objective. The two should be linked, but they are not the same thing.

Should every portfolio use volatility as its main risk measure?

No. Volatility can be useful for diversified, liquid portfolios, but it is not universal. Benchmark-aware mandates may be better managed with tracking error, while some client-outcome portfolios are better framed around drawdown, liquidity, or capital impairment risk.

What makes a benchmark appropriate for a client mandate?

An appropriate benchmark should match the opportunity set, investable universe, and purpose of the strategy. It should help evaluate results honestly rather than flatter the manager. A poor benchmark can distort portfolio construction and performance interpretation.

How should position sizing be governed in a client portfolio?

Position sizing should be tied to explicit limits such as issuer caps, sector ranges, liquidity constraints, and look-through exposure rules. If discretion is allowed, it should be documented in advance, with conditions for when exceptions are permitted and who approves them.

What is the difference between rebalancing policy and tactical deviations?

Rebalancing policy is the standing rule for bringing the portfolio back toward target weights, often using calendar dates or tolerance bands. Tactical deviations are temporary exceptions based on a view. They should be documented clearly and revisited on a defined schedule.

How should performance be reported to clients during weak periods?

Good reporting separates process from short-term outcomes. That usually means showing returns alongside benchmark context, risk taken, attribution, mandate compliance, and a plain explanation of what happened, what has changed, and what has not.

What usually breaks client trust faster: bad returns or bad communication?

Often it is the combination of both, but weak communication usually makes bad performance harder to tolerate. Clients can accept difficult periods more readily when expectations, downside behavior, and decision rules were discussed before the drawdown began.

What are the most common failure modes when managing outside capital?

Common failures include style drift, concentration creep, hidden leverage, liquidity mismatch, benchmark mismatch, and process drift under performance pressure. These usually build gradually and are easier to prevent with clear mandate language and exception governance.

Is this article investment or legal advice?

No. It is an educational guide to portfolio governance and client communication. Specific fiduciary, regulatory, tax, and mandate requirements depend on client type, jurisdiction, and account structure.