Buffer ETF vs. Treasury Ladder vs. Put-Spread Hedge: Comparing the Real Cost

The hard part of downside management is not finding products that sound protective. It is figuring out what you are actually paying, how you are paying for it, and whether that tradeoff makes sense in your account and market environment.

That is why buffer ETFs, Treasury ladders, bond ETF barbells, and put-spread overlays should not be treated as interchangeable hedges. They solve different problems. A buffer ETF wraps an options strategy inside a fund. A Treasury sleeve gives up some equity exposure in exchange for certainty and liquidity. A bond ETF barbell adds flexible fixed-income ballast, but also duration and mark-to-market risk. A put spread keeps more equity beta intact, but makes the insurance cost explicit.[^1][^2]

So the useful question is not, “Which hedge is best?” It is: what risk are you transferring, what does it cost after fees and taxes, and what market path would make that choice look worthwhile in hindsight?

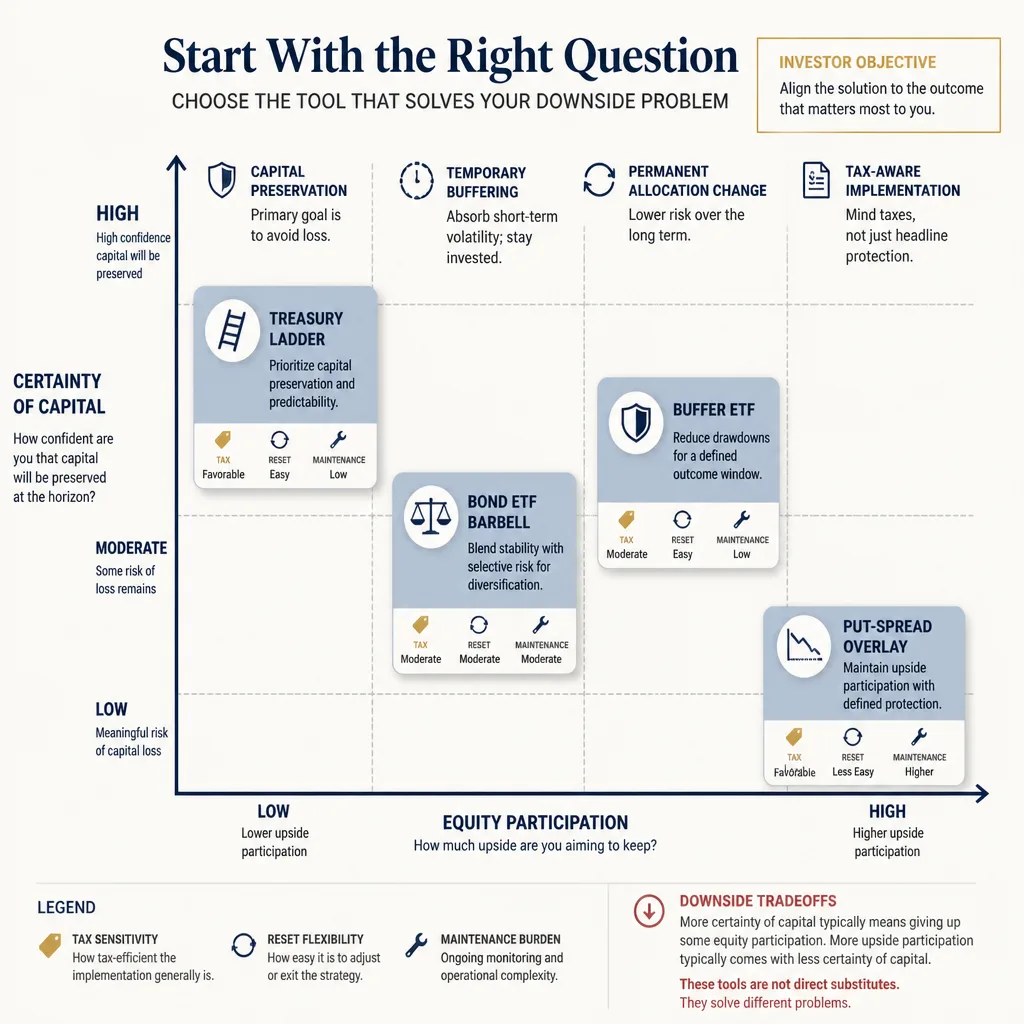

Start with the actual problem you want to solve

Most mistakes happen before the math starts.

If your real goal is capital preservation, a Treasury ladder or T-bill sleeve is often the cleanest answer. If your goal is staying invested in equities while reducing part of a drawdown, then you are comparing option-based structures, whether they sit inside a buffer ETF or are built directly with an overlay.

That distinction matters because these tools change the portfolio in very different ways.

Drawdown reduction is not the same as capital preservation

A buffer ETF can reduce part of an equity drawdown over a defined outcome period, but it is still an equity-linked position. It does not offer principal certainty. Treasury bills and ladders come much closer to capital preservation if held to maturity. A bond ETF barbell sits between the two: less risky than equities, but still exposed to market pricing every day.

A temporary buffer is different from a permanent allocation change

A put-spread overlay and a buffer ETF are temporary structures. Their outcomes depend on strikes, caps, and reset dates. A Treasury sleeve is different. It is a structural allocation choice: lower equity risk, lower upside, and more certainty.

Taxes can change the ranking

On a pre-tax chart, several structures can look similar. After taxes, they often do not. Treasury interest is subject to federal tax but generally exempt from state and local income taxes, which can materially improve after-tax results for investors in high-tax states.[^1][^2] Listed broad-based index options may fall under Section 1256 rules, while ETF options and fund wrappers can be treated differently.[^1] That is not a footnote. It can materially change the comparison.

The four lenses that matter most

If you want a fair comparison, use the same four lenses every time.

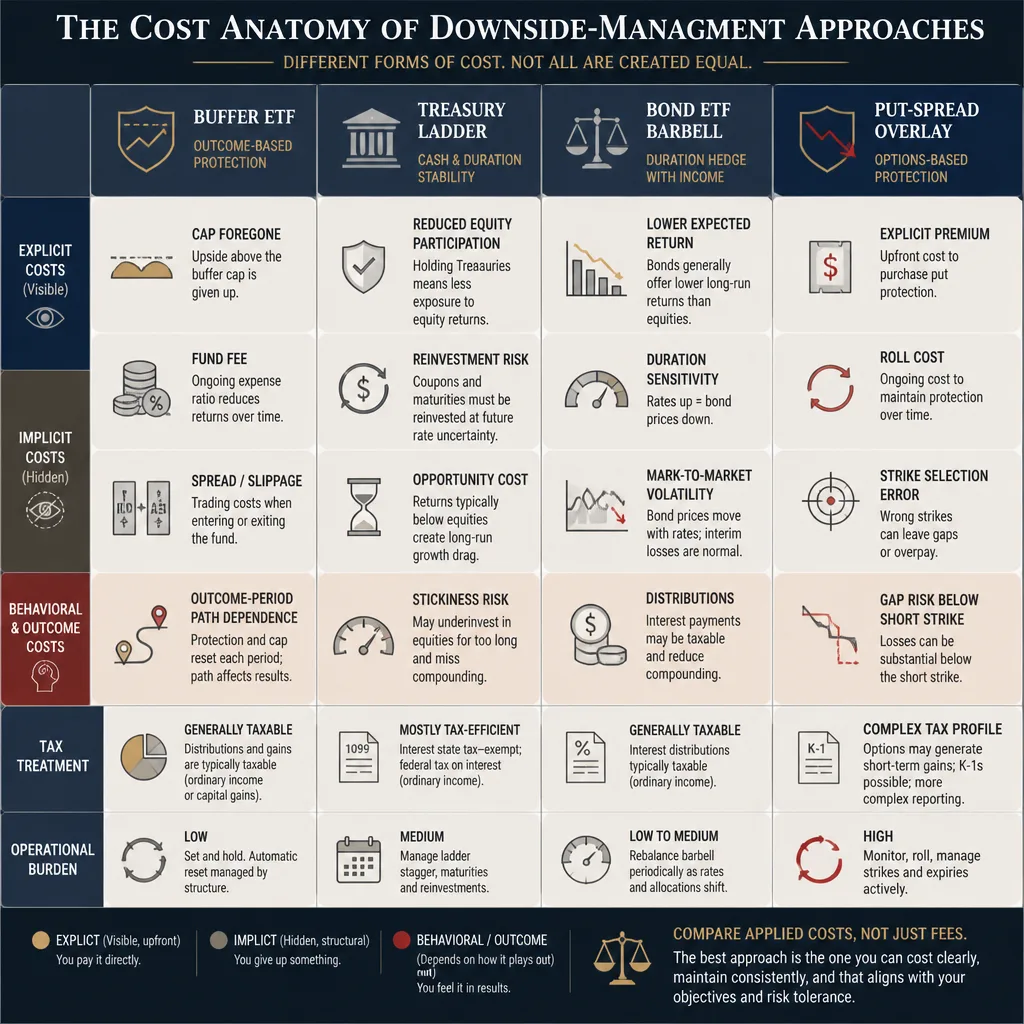

Expected return drag

Every downside-management tool has a cost:

- Buffer ETF: capped upside, plus fund fees and trading friction

- Treasury ladder: less equity participation

- Bond ETF barbell: lower expected return than equities, plus duration risk

- Put-spread overlay: explicit premium and roll cost

The key point is simple: the cost is real even when it does not show up as a line item.

Tax treatment

Taxes are part of the strategy, not an afterthought. Treasuries can look more competitive in taxable accounts because of their state-tax exemption.[^1][^2] Index options can be taxed differently from ETF options. Buffer ETF taxation can also vary by structure and prospectus, especially when FLEX options are involved, so broad generalizations are risky.[^1][^3]

Reset and rebalance mechanics

Mechanics shape outcomes more than many investors expect.

- Buffer ETFs reset outcome periods and caps

- Ladders mature and need reinvestment

- Bond ETF barbells require duration management and rebalancing

- Put spreads need to be rolled on schedule

A strategy can look elegant on paper and still fail in practice if the maintenance burden is too high.

What has to happen for the strategy to work?

This is the most useful question in the whole comparison.

If equities rally sharply, capped structures often lag. If rates are attractive and your tax profile favors Treasuries, safe assets may compare better than expected. If implied volatility is rich, put protection can be expensive. If volatility is moderate and preserving beta matters, a direct overlay can look cleaner than a packaged cap.

Buffer ETFs: simpler to own, costlier than they first appear

The main appeal of a buffer ETF is convenience. The options are already inside the fund. You do not have to choose strikes or manage roll dates yourself.

That convenience is real. So is the cost.

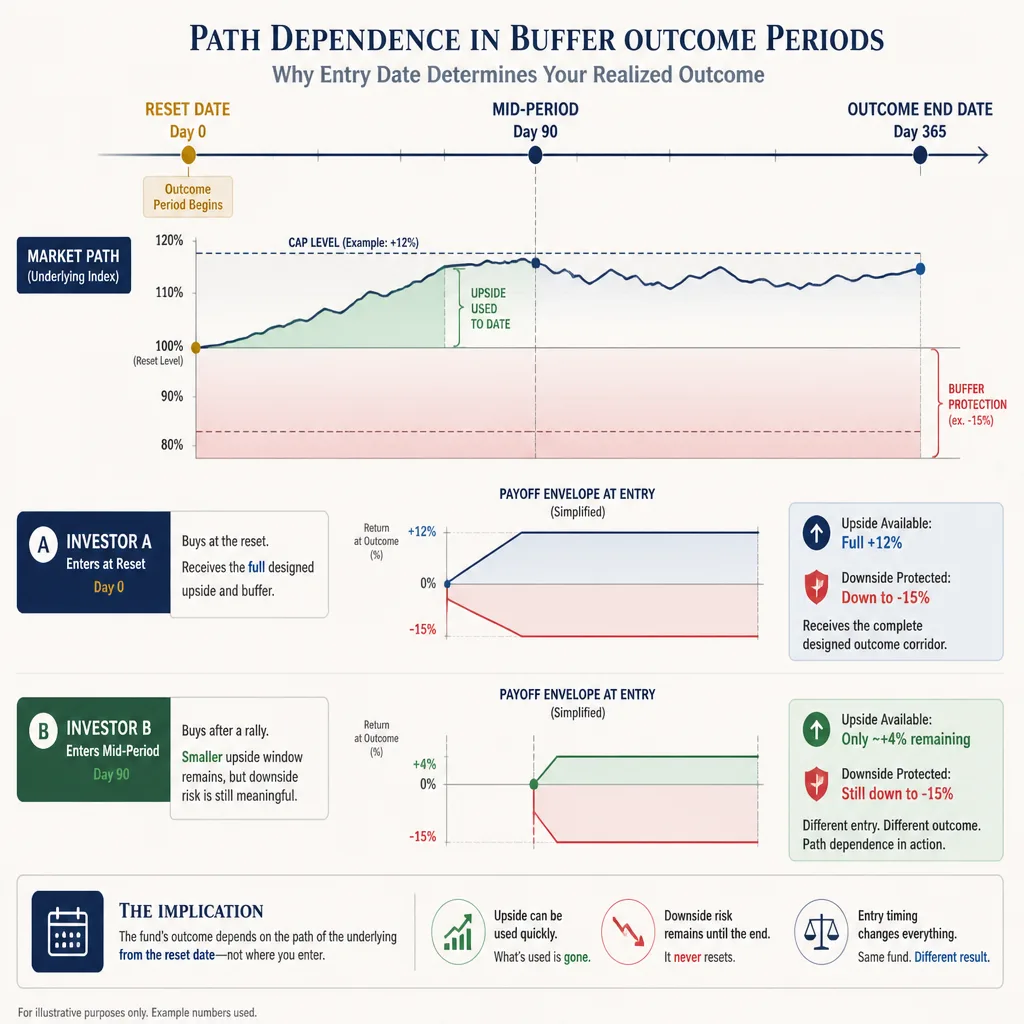

Outcome periods create path dependence

Buffer ETFs are built around a defined outcome period. Prospectuses typically make clear that the advertised cap and buffer are designed for investors who buy at the start of that period and hold through the end.[^3] If you buy mid-period, your payoff may look very different from the headline marketing.

This is the underappreciated trap. If the fund has already risen substantially, much of the upside cap may already be gone. You may have limited remaining upside while still carrying meaningful downside risk if the market reverses.[^3]

The drag comes from more than the expense ratio

Investors often focus on the stated fee and miss the larger cost: foregone upside.

A simple way to think about it:

- the options budget helps fund the buffer

- the cap is part of what pays for that protection

- the fund fee adds wrapper friction

- bid/ask spreads and slippage add another layer

In strong bull markets, the cap often becomes the dominant cost. In flatter or mildly down markets, the tradeoff can look much better.

Tax treatment is less straightforward than many assume

This area requires caution. Many defined-outcome ETFs use FLEX options, but that does not mean they receive the same tax treatment as directly held broad-based listed index options.[^1][^3] Fund-level treatment, distribution character, holding period, and the specific prospectus structure all matter.

For taxable investors, the right question is not “Are options tax-efficient?” It is “Which instrument, in which wrapper, in which account?”

Best fit and common disappointment points

A buffer ETF fits investors who want a packaged, rules-based structure and are willing to trade upside for simplicity.

It tends to disappoint when:

- the investor buys mid-outcome period

- available caps are low

- the market rallies strongly

- the investor mistakes a sleeve-level buffer for broad portfolio protection

Treasury ladders and T-bills: simple, explicit, and often underrated

A Treasury sleeve is often the most honest answer to “I want less downside.”

But it helps to call it what it is: not a hedge overlay, but an asset-allocation decision.

You are not insuring equities. You are replacing part of them.

When you move dollars from equity into T-bills or a Treasury ladder, you are not hedging existing equity exposure. You are reducing it. That means less drawdown, but also less participation when equities rise.

If certainty is the goal, that tradeoff is a feature, not a flaw.

Tax benefits can make the comparison look better than expected

Treasury bills, notes, and bonds are subject to federal income tax, but their interest is generally exempt from state and local income taxes.[^1][^2] For investors in high-tax states, that can make after-tax yield meaningfully more attractive than a casual pre-tax comparison suggests.

That is one reason T-bills can compete surprisingly well with packaged downside products.

Reinvestment risk and duration still matter

A ladder is simple, but it is not static. Every maturity creates a reinvestment decision. Staying very short reduces price volatility but increases reinvestment uncertainty. Extending maturity can lock in yield, but adds duration exposure.

That tradeoff matters more than many investors think, especially when rates move quickly.

When a Treasury sleeve tends to win

A Treasury sleeve usually looks best when:

- certainty is the top priority

- short-term rates are attractive

- the account is taxable and state taxes matter

- expected equity upside is modest relative to the cap you would give up elsewhere

It will lag badly in a strong equity bull market. That is the price of safety.

Bond ETF barbells: flexible, liquid, and easy to misclassify

A bond ETF barbell is often the middle-ground choice: some short-duration ballast, some intermediate- or longer-duration exposure, and full intraday liquidity.

That flexibility is useful. It is also different from a ladder.

A bond ETF is not a hold-to-maturity ladder

A Treasury ladder gives you known maturity values if you hold the securities to maturity. A bond ETF does not. Even defined-maturity ETF families are still funds whose shares trade and whose market values fluctuate until they terminate or mature.[^4]

That makes them useful implementation tools, but not direct substitutes for owning individual bonds.

Flexibility comes with mark-to-market risk

A barbell can help investors manage liquidity and yield exposure more actively. But the tradeoff is price volatility. If rates rise, the ETF’s market value can fall, even if its role in the portfolio is meant to be defensive.

That is fine if you want tradable ballast. It is less helpful if your real objective is a known dollar amount at a known date.

Taxes still require instrument-level thinking

Bond ETFs can be operationally convenient, but taxable investors still need to think through distribution character, turnover, and whether the chosen funds carry the same state-tax advantages as direct Treasuries. “Bond exposure” is not a tax category.

When a barbell makes sense

A bond ETF barbell is often the better choice when liquidity and tactical rebalancing matter more than maturity certainty.

It is less compelling when the real objective is principal preservation or liability matching at a known date.

Put-spread overlays: direct insurance, explicit cost, higher maintenance

A put-spread overlay is the cleanest “keep the equity, buy some protection” structure in this comparison.

It is also the least forgiving operationally.

The protection is targeted, not complete

A basic put spread buys downside protection over a chosen range. It can cushion losses between the long put strike and the short put strike, but not necessarily beyond that range. The exact payoff depends on the strikes and tenor.

So the hedge is not free, and it is not complete. It is targeted insurance.

The real comparison is explicit cost versus implicit cost

This is the right comparison against a buffer ETF.

With a put spread, the premium is explicit. You can see the cost. With a buffer ETF, part of the cost is implicit because you give up upside through the cap. Neither approach is automatically cheaper. The better choice depends on volatility pricing, strike selection, and how much upside you think you are surrendering.

In high-volatility markets, direct option protection can be expensive. In more moderate-volatility conditions, it can be more efficient than many investors assume.

Tax treatment depends on the instrument and the account

Broad-based listed index options may be treated as Section 1256 contracts, with mark-to-market treatment and blended 60/40 tax character.[^1] ETF options may not receive that treatment. Straddle rules and account type can complicate things further.[^1]

So “options are tax-efficient” is too vague to be useful. Instrument choice matters.

Operational burden is where good ideas often fail

This is where many otherwise sensible overlay plans break down.

You need clear rules for:

- how far out to hedge

- which strike range to protect

- how often to roll

- what to do if volatility spikes before the next roll

- how much basis risk or gap risk you can tolerate

A buffer ETF may be less precise in theory, but for investors who will not maintain an overlay consistently, the wrapper may be the better real-world solution.

A practical comparison

| Approach | Main cost | Best account fit | Operational burden | Usually wins when... |

|---|---|---|---|---|

| Buffer ETF | Capped upside plus fund friction | Often IRA or simplicity-first taxable use | Low | You want packaged downside management, can accept a cap, and expect flat, choppy, or moderately up markets |

| Treasury ladder / T-bills | Lower equity participation | Especially strong in taxable accounts with state-tax sensitivity | Low to medium | Safety, liquidity, and after-tax certainty matter more than preserving beta |

| Bond ETF barbell | Lower expected return than equities plus duration and mark-to-market risk | Flexible in taxable or tax-advantaged accounts, depending on holdings | Medium | You want liquid fixed-income ballast and tactical rebalancing flexibility |

| Put-spread overlay | Explicit premium plus roll risk | Best where tax and instrument choice are handled deliberately | High | You want to preserve equity beta and can execute consistently, especially when volatility pricing is reasonable |

The comparison mistakes that matter most

Confusing a stated buffer with portfolio-level protection

A 10% or 15% buffer on one sleeve is not the same as protecting the whole portfolio. Investors often overstate how much total drawdown risk they have reduced.

Ignoring entry date and reset mechanics

This is probably the biggest buffer ETF mistake. Outcomes depend heavily on when you buy, when the fund resets, and how much cap remains.[^3]

Using pre-tax assumptions in taxable accounts

For many investors, especially in high-tax states, Treasury state-tax exemption can materially change the comparison.[^1][^2]

Mistaking simplicity for low cost

A product can be easy to own and still expensive in expected-return terms. Buffer ETFs are the clearest example.

Treating bond funds and ladders as interchangeable

They are not. A ladder offers maturity certainty. A bond ETF offers liquidity and flexibility. Those are different benefits.

How to choose

If simplicity matters most

A buffer ETF can make sense, but only if you understand the outcome period, the current cap, and how sensitive results are to your entry date.

If after-tax certainty matters most

Start with T-bills or a Treasury ladder. In many taxable accounts, especially in high-tax states, this is the most straightforward solution.

If preserving equity exposure matters most

A simple index put-spread overlay deserves the closest look. It is often the cleanest way to keep beta while buying targeted protection, assuming you can handle the operational burden.

If implementation discipline is the real constraint

Be honest about that. The best hedge in theory is useless if you will not maintain it. Many investors are better served by a simpler product or a safer allocation than by a sophisticated overlay they will not roll correctly.

Conclusion

The right comparison is not buffer ETF versus Treasury ladder versus put spread in the abstract. It is which cost you are most willing to bear.

A buffer ETF asks you to pay with upside and wrapper friction. A Treasury sleeve asks you to accept lower equity participation. A bond ETF barbell asks you to accept duration and mark-to-market movement in exchange for flexibility. A put-spread overlay asks you to pay an explicit premium and manage the position well.

That is the framework that matters. Not the label. Not the sales pitch. Ask one question every time: what am I paying, in what form, and what market path would make that payment worth it?

FAQ

Are buffer ETFs a direct substitute for a Treasury ladder or T-bills?

Not really. A buffer ETF is an equity-linked structure with capped upside and defined-outcome mechanics. A Treasury ladder or T-bill sleeve is mainly an allocation choice that trades equity participation for principal certainty and income.

What matters most when comparing downside-management strategies?

The most decision-useful variables are expected return drag, tax treatment, reset or rebalance mechanics, and the market conditions required for the strategy to outperform its alternatives.

Why can a Treasury ladder look better in taxable accounts than investors expect?

Because Treasury interest is generally subject to federal income tax but exempt from state and local income taxes.[^1][^2] That can improve after-tax results, especially for investors in high-tax states.

What is the main tradeoff in a buffer ETF?

Convenience. The investor gets a packaged downside buffer, but pays through capped upside, fund fees, trading friction, and outcome-period rules that can make realized results differ from the headline buffer.[^3]

Why does purchase timing matter with buffer ETFs?

Because the stated cap and buffer are designed for a specific outcome period. Buying after that period has started can leave less upside available while still exposing the investor to downside if markets move against the position.[^3]

How is a bond ETF barbell different from a Treasury ladder?

A bond ETF barbell is liquid and flexible but remains mark-to-market. A Treasury ladder offers known maturity values if held to maturity, which makes it a different tool for investors who care more about certainty than tradability.[^4]

When does a put-spread overlay make more sense than a buffer ETF?

Usually when an investor wants to preserve equity beta and is willing to pay an explicit insurance cost rather than surrender upside through a cap. It tends to fit more disciplined investors who can manage rolling and strike selection.

Are put-spread hedges always too expensive?

No. Their efficiency depends heavily on implied volatility, tenor, strike design, and roll frequency. In some regimes they can be more efficient than giving up upside in a buffer ETF. In others, they are simply costly insurance that expires unused.

Do taxes differ between index options and ETF options?

They can. Broad-based listed index options may receive different tax treatment than ETF options, and fund wrappers can differ again.[^1] That is why after-tax comparisons should be instrument-specific.

Which approach is usually simplest to maintain?

A buffer ETF is often the simplest operationally because the options are packaged inside the fund. Treasury ladders are also straightforward, though they require reinvestment decisions. Put-spread overlays usually require the most ongoing discipline.

What does a bond ETF barbell need to outperform the alternatives?

It usually needs the investor to value liquidity, tactical flexibility, and tradable fixed-income ballast more than hold-to-maturity certainty. It is often the better fit when rebalancing flexibility matters more than principal certainty at a specific date.

Can investors combine these approaches instead of choosing only one?

Yes. Many investors may be better served by combining tools—for example, holding a Treasury sleeve for certainty while adding a smaller options overlay for targeted downside protection—rather than expecting one product to solve every risk-management problem.