Your First Investing Decisions That Matter: Time Horizon, Risk Capacity, and an Asset Allocation You Can Stick With

Most new investors start in the wrong place. They look for the best stock, the best ETF, or the perfect entry point. Those choices usually matter less than people think.

The first decisions are simpler and more important: What is this money for? When will you need it? How much loss can you absorb financially and emotionally without bailing out? Those answers determine your asset allocation, and for most beginners, asset allocation matters more than security selection.

That is the core idea here: successful investing usually starts with portfolio design and behavior control, not prediction. A simple stock-bond-cash mix you can hold through bad markets is often worth more than a theoretically better portfolio you abandon at the worst time. Research on investor return gaps has repeatedly shown that behavior, especially poor timing decisions, can pull actual investor results below fund results.[^1]

Your first investing decisions matter more than your first stock pick

If you buy a low-cost diversified portfolio and keep contributing, you are already doing much of what drives long-term outcomes. Costs matter. Taxes matter. Savings rate matters a lot. But for a beginner, the biggest avoidable mistake usually is not choosing the wrong ticker. It is choosing a level of risk that looks fine in a spreadsheet and feels unbearable in real life.

That is why diversification guidance from the SEC’s Investor.gov and major firms such as Vanguard focus so heavily on portfolio construction rather than stock-picking contests.[^2]

Why allocation and behavior usually matter more than early security selection

A beginner deciding between a total U.S. stock market fund and an S&P 500 fund is making a relatively small decision. A beginner deciding between 90% stocks and 50% stocks is making a much bigger one.

The second choice changes the ride.

A portfolio that drops 15% in a bad year and one that drops 35% are not the same experience. If the deeper drop causes you to stop contributing, sell out, or avoid investing for years, the “higher-return” portfolio was not actually better for you.

Choose a portfolio you can survive, not just one that looks good on paper

That word matters: survive.

The right beginner portfolio is not the one with the highest expected return in theory. It is the one that gives your money a reasonable chance to grow while remaining financially and behaviorally survivable through ugly periods.

Start with the goal, not the market

Before choosing percentages, separate your money by purpose.

A lot of confusion disappears once you stop asking, “What should my allocation be?” and start asking, “What is this specific pool of money supposed to do?”

Match each pool of money to a purpose

Your emergency fund is not your retirement account. Your house down payment is not your IRA. Graduate school in five years is not the same problem as retirement in thirty.

That sounds obvious, but many investors still apply one portfolio to all their money and then wonder why they feel stuck.

Time horizon is not just age

Age is a shortcut. Sometimes a useful one, but still a shortcut.

A 30-year-old may reasonably invest retirement savings aggressively while keeping a home down payment mostly in cash because that money will be spent in two years. Same person, same age, different job for the money.

This is one of the most important beginner ideas: the time horizon belongs to the goal, not just the investor.

A simple three-bucket framing

| Time horizon | Primary objective | Typical posture |

|---|---|---|

| Under 3 years | Stability and liquidity | Mostly cash or very stable assets |

| 3 to 10 years | Balance growth and capital preservation | Mix of stocks, bonds, and some cash |

| 10+ years | Long-term growth | Mostly stocks, with bonds or cash as ballast if needed |

This is not a formula. It is a starting framework.

Cash is often the safer tool for money needed soon. Stocks may be “safer” for preserving purchasing power over decades, but not for money you need next year.

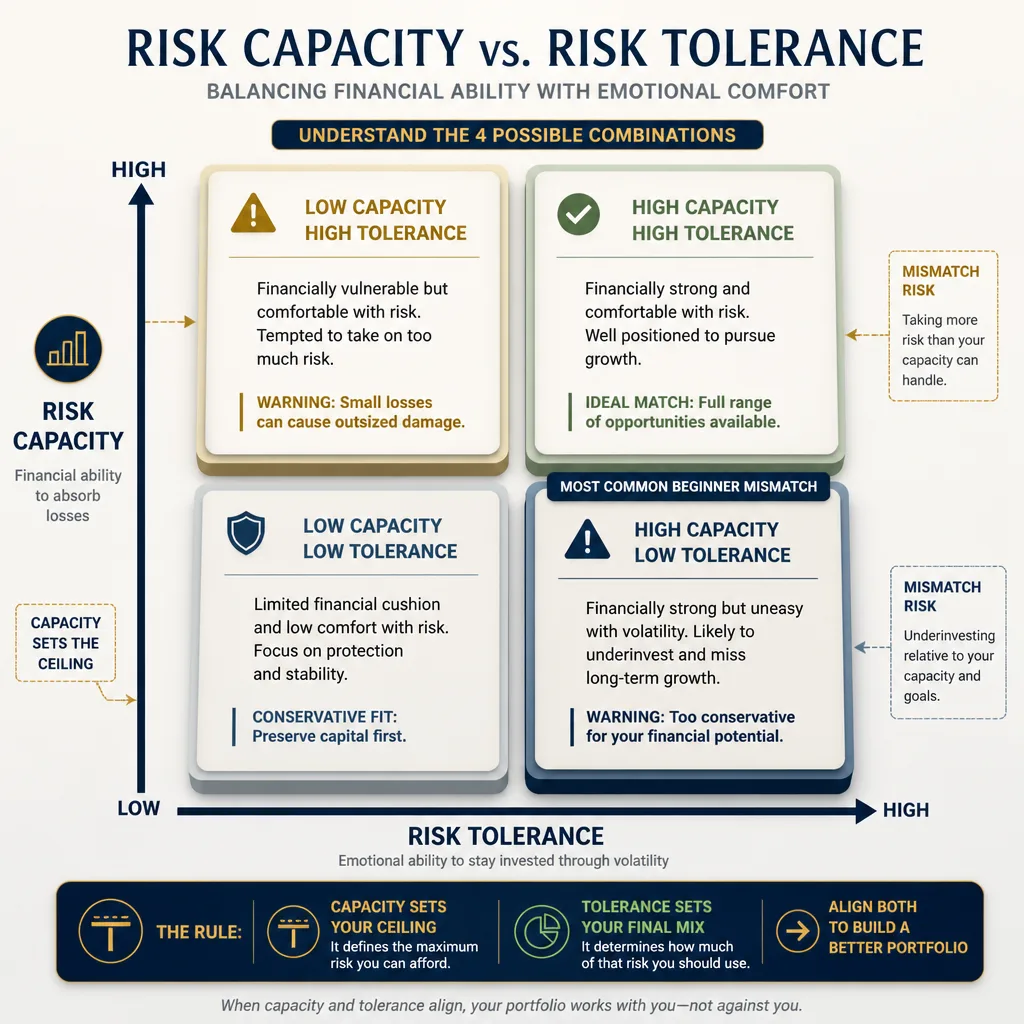

Risk capacity and risk tolerance are different

This is where many generic articles fall short.

Risk capacity

Risk capacity is your financial ability to absorb losses without derailing the goal.

If your job is stable, you have a solid emergency reserve, little high-interest debt, flexibility on timing, and you can keep contributing during downturns, your capacity for risk may be fairly high.

If you are saving for a fixed down payment in 24 months, have uneven income, and little backup cash, your capacity is lower no matter how “aggressive” you feel.

Risk tolerance

Risk tolerance is your emotional ability to watch volatility without abandoning the plan.

How did you react the last time markets dropped? Do you check your account every day? Would a 25% decline make you want to “wait until things calm down”? If so, your practical tolerance may be lower than you think.

How to use both

A useful rule:

- Capacity sets the ceiling

- Tolerance shapes the usable allocation

If you have low capacity, you should not take high risk just because you feel comfortable with it. If you have high capacity but low tolerance, taking the mathematically optimal amount of risk may still be a mistake because you will not stick with it.

A common mismatch looks like this: a 27-year-old saving for retirement may have the capacity to hold mostly stocks, but if a 30% decline would cause them to sell, 100% equities is not a good real-world portfolio.

The reverse happens too. Someone may love risk, read market forums all day, and feel invincible, but if the money is for a wedding next year, capacity is still low.

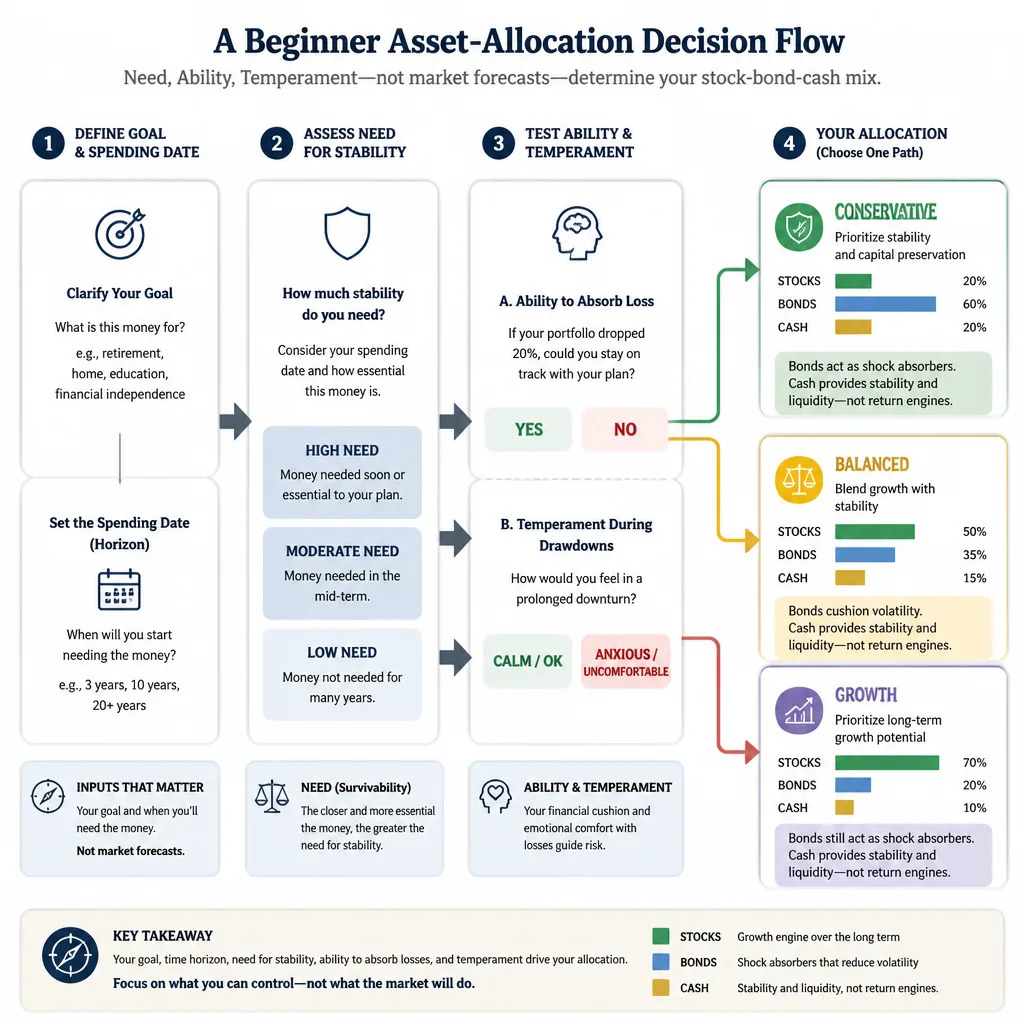

A practical framework for choosing a stock-bond-cash mix

A simple decision tool is Need, Ability, Temperament.

- Need: When does this money need to be spent?

- Ability: What happens if it falls sharply?

- Temperament: What will you honestly do if that happens?

If your allocation fails any one of those tests, it probably needs adjustment.

Step 1: Decide how much of this money needs stability

Start with money that cannot afford a large drawdown.

Emergency reserves, upcoming tuition, tax payments, and near-term home purchases usually belong mostly in cash or similarly stable holdings. Holding cash here is not a mistake. It is doing its job.

Step 2: Put long-horizon growth capital mostly in equities

For money you will not need for 10 years or more, equities have historically offered higher expected long-run returns than bonds or cash, though with larger drawdowns.[^3] That is why stocks are the growth engine.

For many beginners, that means retirement money can usually support a substantial equity allocation, assuming risk capacity and behavior support it.

Step 3: Use bonds as shock absorbers, not return engines

Bonds are often misunderstood.

They are not in the portfolio because they are expected to beat stocks over long periods. They are there to reduce volatility, provide liquidity, and give you something steadier to rebalance from when stocks fall. In 2008, diversified stock-bond portfolios generally fell far less than all-stock portfolios. In 2022, both stocks and many bond segments fell, which is a useful reminder that bonds reduce risk but do not eliminate losses every year.[^4]

Step 4: Keep it simple enough to maintain

Most beginners do not need seven funds and tactical tilts.

A simple portfolio might use:

- a broad stock index fund or ETF

- a broad bond fund or ETF

- cash in a high-yield savings account or money market fund for near-term needs

That can be implemented in a 401(k), IRA, or brokerage account depending on the goal and account availability.

Simple example allocations and when they make sense

These are educational starting points, not personalized advice.

Conservative example

A portfolio around 30% stocks / 50% bonds / 20% cash can make sense for money with a medium horizon, low flexibility, or an investor who cannot withstand major losses.

This is not “safe” in every sense. It may still lose purchasing power after inflation over time. But it may be more appropriate for a goal where stability matters more than maximum growth.

A real-world example: someone planning to start grad school in five years and needing most of the funds available on schedule.

Balanced example

A portfolio around 60% stocks / 35% bonds / 5% cash fits many investors with a medium-to-long horizon who want growth but need a smoother ride than an all-stock portfolio.

This is often where beginners find out whether they can stay disciplined. In severe periods, a balanced allocation can still fall meaningfully, roughly in the mid-teens to mid-20% range depending on the exact mix, rebalancing approach, and period examined. That is painful, but often more survivable than a 100% stock drawdown.

Growth example

A portfolio around 80% to 90% stocks / 10% to 20% bonds / minimal cash may fit long-horizon retirement investors with strong emergency reserves, stable income, and proven ability to hold through declines.

This can be reasonable. It is not reckless by definition. But it fails if the investor mistakes a long horizon for high tolerance.

Why these are only starting points

The same allocation can be wise for one person and wrong for another.

A conservative allocation is not automatically safer if it leaves a 30-year goal underfunded. A growth allocation is not automatically smarter if it causes panic selling in the first real bear market.

Sanity-check the portfolio before you fund it

This is the step many beginners skip.

Ask what a bad year could look like

Do not ask whether your portfolio is “moderate.” That word is too vague.

Ask what a severe year might look like. Historically, stocks have suffered very large declines, including a peak-to-trough drop of more than 50% during the 2007–2009 financial crisis.[^5] Mixed portfolios have generally fallen less, but they still lose money in hard periods.

Exact figures vary by asset definitions, timeframe, and rebalancing assumptions. Think in rough ranges, not promises.

Translate percentages into dollars

If you have $20,000 invested:

- a 20% drop means about $4,000 down

- a 30% drop means about $6,000 down

- a 40% drop means about $8,000 down

If you have $100,000 invested:

- a 20% drop is $20,000

- a 30% drop is $30,000

- a 40% drop is $40,000

This is a better behavioral test than labels. If seeing that number makes you think, “I would sell and wait,” the allocation is probably too aggressive.

Pair the allocation with a contribution plan

A contribution plan changes the psychology.

Instead of making one giant timing decision, you commit to a process. Maybe that means investing $500 per month into your 401(k), IRA, or brokerage account. Ongoing contributions do not guarantee better returns, but they can reduce paralysis and make downturns easier to handle because lower prices mean new money buys more shares.

That is one reason simple automated plans work so well in practice.

Stress test with one honest question

If markets fell sharply next month, what would you actually do?

Would you keep contributing? Rebalance? Stop checking the account? Or hit sell?

Your honest answer matters more than your theoretical appetite for risk.

The beginner mistake is changing the plan at the worst time

A decent allocation held consistently usually beats a better-looking one abandoned in a crash.

That is not motivational fluff. It is the central practical problem of investing.

Why consistency matters more than a slightly “better” portfolio

If one portfolio has slightly lower expected returns but you can actually hold it, it may produce better real investor outcomes than a more aggressive mix you sell after a 35% decline. This is the same broad logic behind behavior-gap research like Morningstar’s Mind the Gap, which has documented the cost of mistimed investor cash flows.[^1]

How to automate contributions and rebalance lightly

Keep maintenance simple.

A beginner-friendly approach:

- automate contributions each month

- review once or twice a year

- rebalance if allocations drift meaningfully from target

“Meaningfully” does not need to be hyper-precise. Many investors use either a calendar rule, such as annual rebalancing, or a drift rule, such as rebalancing when an asset class moves several percentage points away from target.

The point is to control risk, not trade constantly.

When it makes sense to adjust the allocation

Good reasons to change your allocation:

- the goal changed

- the spending date moved closer

- your income, debt, or emergency reserves changed materially

- you discovered the portfolio is behaviorally unworkable

Bad reasons:

- scary headlines

- last year’s top-performing fund

- a market drop that makes you want certainty

- a market rally that makes you feel invincible

What to do next

Write down four things today: the goal, the spending date, the target allocation, and the monthly contribution amount.

Then choose low-cost diversified funds that clearly map to that allocation. Many investors use broad stock index funds, broad bond funds, and a cash reserve in a savings or money market vehicle. If simplicity helps you stay disciplined, a well-chosen target-date fund can also be a reasonable implementation tool, though its built-in glide path may not match every goal.

Finally, set a review schedule. Not a reaction schedule.

If you want a durable investing habit, stop asking what to buy next and start asking whether your portfolio matches the job the money needs to do, how much loss you can really absorb, and whether the plan is simple enough to survive the next bad year.

Conclusion

The most important first investing decision usually is not picking the right stock. It is choosing a stock-bond-cash allocation that fits the goal, respects the time horizon, and can survive both market volatility and your own behavior.

Start with the purpose of the money. Separate risk capacity from risk tolerance. Use bonds and cash deliberately. Then stress test the plan in dollar terms before you fund it.

If your portfolio can survive a bad year without forcing a bad decision, you are much closer to a good allocation than someone chasing the perfect fund. In investing, a simple plan you can hold is often more powerful than a clever plan you cannot.

FAQ

What should my first investment allocation be?

It should match the purpose of the money, when you will need it, and how much loss you could realistically endure without selling. As a starting framework, money needed within about 3 years usually belongs mostly in cash or very stable assets; money for 3 to 10 years may justify a mix of stocks, bonds, and cash; money for 10+ years can usually take more stock exposure if your risk capacity and behavior support it.

What is the difference between risk capacity and risk tolerance?

Risk capacity is your financial ability to absorb losses without derailing your goal. Risk tolerance is your emotional ability to stay invested when losses happen. You may have high capacity but low tolerance, or low capacity but high tolerance. A workable allocation needs both.

Why is time horizon more important than age alone?

Age is only a rough shortcut. What matters more is when this specific money will be spent. A 30-year-old may invest retirement savings aggressively while keeping a house down payment in cash if it will be needed in two years. Different goals can require different allocations at the same age.

How much of my portfolio should be in stocks, bonds, and cash?

There is no universal percentage that fits everyone. In general, stocks are the long-term growth engine, bonds can reduce volatility and provide rebalancing capital, and cash is useful for near-term spending, emergency reserves, and sometimes behavioral stability. The right mix depends on your horizon, financial flexibility, and ability to stay disciplined in a downturn.

Should beginners be 100% in stocks?

Not always. Some investors with a very long horizon, stable income, strong emergency savings, and high tolerance for volatility may be able to hold 100% stocks. But many beginners overestimate how calm they will be during a large drawdown. If a 30% to 50% drop would make you sell, a slightly less aggressive allocation may work better in practice.

What role do bonds play in a beginner portfolio?

Bonds are not mainly there to beat stocks. Their role is to act as shock absorbers, provide liquidity, and give you something steadier to rebalance from when stocks fall. They can still lose money in some years, as 2022 reminded investors, but they usually reduce overall portfolio volatility compared with an all-stock mix.

When does holding cash make sense for an investor?

Cash makes sense for emergency savings, planned spending in the next few years, and situations where a modest reserve helps prevent forced selling from your long-term portfolio. Cash may reduce long-run returns, but it can still be the right tool when stability and flexibility matter more than growth.

How do I know if an allocation is too risky for me?

A useful test is to convert a bad year into dollars. If your planned portfolio could plausibly fall 20% or more in a severe period, ask yourself what that would mean for your actual balance. If the likely loss would force you to sell, delay the goal, or lose enough sleep to abandon the plan, the allocation may be too aggressive.

What if the market falls right after I start investing?

That is uncomfortable but normal. If your allocation was built around the right goal and time horizon, a decline right after you start does not automatically mean the plan was wrong. Ongoing contributions can help because they turn a single entry decision into a continuing process, though they do not guarantee better returns.

How often should I rebalance my portfolio?

A simple beginner approach is to review the portfolio once or twice a year, or rebalance when the allocation drifts meaningfully from target. The goal is to keep risk aligned with the plan without encouraging constant tinkering.

When should I change my asset allocation?

Change it when the goal changes, the spending date gets closer, your financial situation changes materially, or you discover the current mix is behaviorally unworkable. Headlines, recent market returns, or fear alone are usually poor reasons to redesign the portfolio.

Are risk tolerance questionnaires enough to choose an allocation?

They can be useful, but they are not enough on their own. Many questionnaires miss factors like emergency savings, debt, job stability, concentrated income risk, and whether the money has a fixed near-term use. They should support judgment, not replace it.