International Diversification in an AI-Heavy Market: How to Diversify Within the AI Capex Cycle

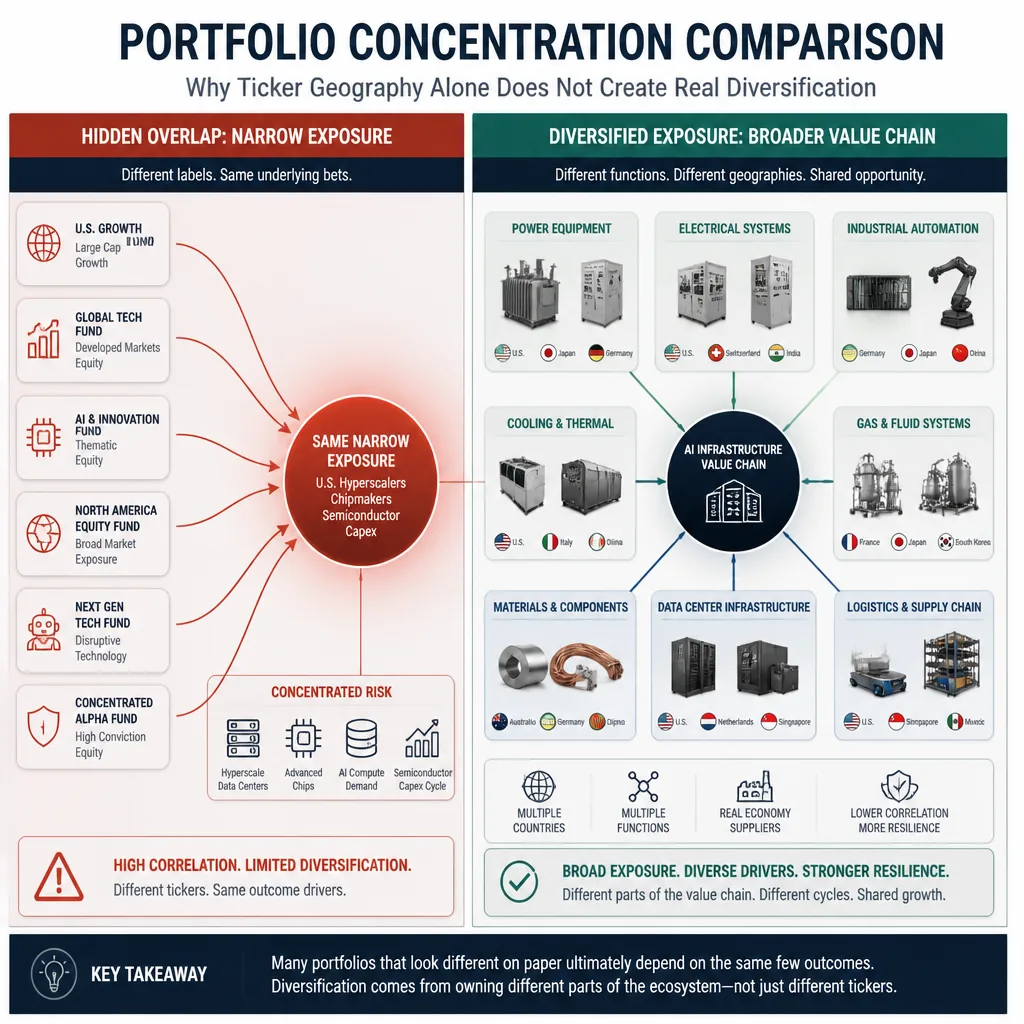

Many portfolios are more concentrated than they look.

You can own a broad U.S. index fund, a semiconductor ETF, a “global innovation” strategy, and a few individual AI winners and still be making essentially the same bet: that a small group of U.S. hyperscalers keeps spending heavily on chips, data centers, and model infrastructure. Microsoft and Alphabet have both signaled sustained AI infrastructure investment, while the International Energy Agency has pointed to rising data-center electricity demand and growing infrastructure bottlenecks.[^1][^2]

That matters because international diversification in an AI-heavy market does not have to mean cutting AI exposure. Often, the better move is to broaden exposure across the global systems that make the buildout possible: power equipment, cooling, automation, materials, and selected logistics. The key question is not just where a company is listed. It is how AI demand reaches that company’s income statement.

That is the central idea here: if you want to diversify an AI-heavy portfolio, diversify the function you own inside the AI capex cycle, not just the country code attached to the ticker.

International diversification does not have to mean leaving the AI trade

Why many portfolios are more AI-concentrated than they appear

The hidden issue is overlap.

Different funds can hold the same mega-cap platforms. Different “AI baskets” can still depend on the same GPU cycle. Even foreign-listed companies may remain tightly tied to the same end customers, the same semiconductor capex budgets, and the same sentiment swings that drive U.S. AI leaders.

That is why simply adding non-U.S. technology exposure is not automatic diversification. ASML is a good example. It is clearly central to the global AI buildout, and its 2025 disclosures linked growth in logic and memory demand to AI-related semiconductor demand.[^3] But from a portfolio-construction standpoint, it may not reduce your dependence on the same chip capex cycle and the same narrow set of advanced-node customers.

The real question: diversify the revenue drivers, not just the geography

A better test is simple: when AI capex rises, who actually gets paid?

If the answer is still “the same few chipmakers and cloud platforms,” you may have changed wrappers without changing exposure. If the answer is “electrical equipment vendors, industrial-gas suppliers, cooling specialists, or factory-input providers serving broader customer sets,” the diversification may be more meaningful.

That is the shift investors need to make. Geography matters, but revenue pathways matter more.

A better lens: the AI capex spillover map

From GPU demand to physical-world bottlenecks

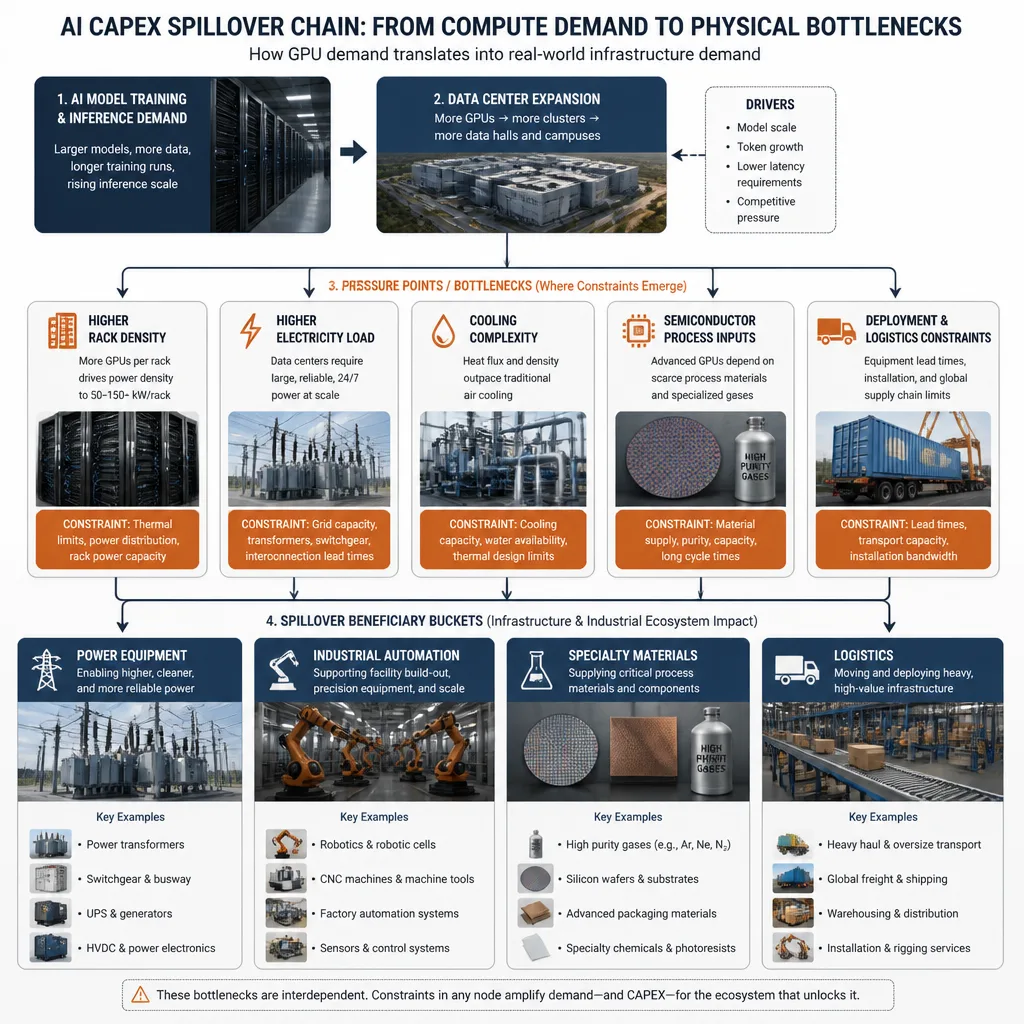

AI is often discussed as a software story. At this stage of the cycle, it is still very much a physical buildout story.

More compute means more racks, higher power density, more cooling complexity, more interconnection needs, and more pressure on grid equipment and site development. The IEA reported that data-center electricity demand surged 17% in 2025 and highlighted tightening supply chains in transformers, turbines, chips, and planning approvals.[^2] In other words, GPU demand spreads outward into real-world bottlenecks.

Four spillover buckets worth watching

The most useful way to think about international AI beneficiaries is by function:

Power equipment and electrification

Switchgear, transformers, power distribution units, busways, cabling, backup power, and cooling-linked electrical architecture.Industrial automation

Controls, building systems, efficiency software, factory systems, and automation vendors that help increase throughput or manage energy intensity.Specialty materials and process inputs

Industrial gases, semiconductor chemicals, substrates, thermal-management inputs, and precision components needed upstream.Logistics and enabling infrastructure

Transport, warehouse systems, and supply-chain bottleneck solvers. This is usually the least direct bucket and should be treated accordingly.

Why second-order beneficiaries can diversify better

Second-order beneficiaries can offer better diversification because they often have different customer mixes, operating cycles, and valuation anchors.

A power-infrastructure company may benefit from data-center demand, but it may also serve utilities, buildings, and industrial customers. An industrial-gas supplier may see stronger electronics demand while still operating through long-cycle contracts and installed-site relationships rather than pure market enthusiasm. That broader base can reduce dependence on a single narrative, even if it can also limit upside during the most euphoric phases of the trade.[^4][^5]

Where to look outside the U.S.

Power and electrification

This is probably the clearest spillover category today.

Schneider Electric is a useful example because its exposure is tied to the physical requirements of AI-ready data centers rather than software-platform economics. The company has described AI clusters as creating power-density and infrastructure challenges, and it has launched offerings around modular data centers, liquid cooling, high-power busway, PDUs, and switchgear.[^6] Its 2025 results also showed sharp acceleration in data-center-related demand, including very strong growth in the pure data center segment.[^4]

The portfolio point is not “buy Schneider.” It is to notice the type of exposure. You are owning the electrical and facility layer of the buildout, where grid access, power quality, and deployment speed matter.

Industrial automation

This category is more nuanced.

Some automation companies can benefit because AI capex raises demand for higher-throughput manufacturing, more efficient facilities, and more resilient infrastructure operations. But the link is usually broader than AI alone. In most cases, you are buying a business with several demand drivers, not a pure-play AI beneficiary.

That can still be attractive. In fact, it may be preferable if your goal is resilience rather than maximum thematic torque. The tradeoff is that attribution becomes less clean. Strong results may come from electrification, reshoring, efficiency spending, or a broader industrial recovery as much as from AI itself.

Specialty materials and process inputs

This is one of the better hunting grounds for spillover exposure.

Industrial-gas and process-input suppliers often sit deep enough in the chain to benefit from semiconductor capacity expansion without necessarily trading like headline AI names. Linde expanded ultra-high-purity gas supply to Samsung’s semiconductor complex in South Korea in 2025 and said demand from semiconductor manufacturers and AI-related digital infrastructure remained strong.[^5] Air Liquide likewise pointed to electronics growth supported by carrier-gas sales and production-unit startups tied to advanced manufacturing activity.[^7]

These businesses can be useful because AI demand is often incremental, not the whole story. That matters. If AI is additive to an already durable business, you may gain exposure to the capex cycle without tying the full investment case to one theme.

ASML also fits here, but as a cautionary sub-case. It is highly relevant to AI infrastructure spending, yet it may not provide much diversification from semiconductor beta.[^3]

Logistics and enabling infrastructure

This is the weakest direct link and deserves caution.

A company like KION Group can fit the broader framework because warehouse automation and intralogistics benefit from supply-chain modernization and throughput needs.[^8] But that is not the same as saying it is a direct AI data-center beneficiary. The connection is more adjacent: if AI investment drives broader industrial and logistics upgrades, these firms can participate. That is plausible, but it is not the highest-conviction part of the theme.

Stretch the idea too far and you risk buying companies that merely sound adjacent.

How to tell real diversification from “U.S. tech beta in another wrapper”

Revenue concentration: who actually pays the company?

Start with the customer base.

If a non-U.S. company still depends heavily on a small number of hyperscalers, colocation operators, or advanced semiconductor customers, the diversification benefit may be limited. If it serves a broader mix of utilities, industrial operators, fabs, OEMs, and service customers, the portfolio behavior may be meaningfully different.

Order visibility versus narrative exposure

Management saying “AI” is not evidence.

Better signals include backlog growth, capacity agreements, explicit data-center or electronics demand commentary, and proof that customers are committing to actual deployment. Schneider’s supply-capacity agreements tied to rising data-center demand are a better signal than generic AI language.[^9]

Installed base, service revenue, and replacement cycles

A company with a large installed base and recurring service revenue often behaves differently from a pure capex beneficiary.

That does not make it better. It makes it different. Service and replacement cycles can smooth outcomes, while one-time project exposure can create more volatility.

Valuation behavior

This is a practical but underused test.

If a stock trades like a daily referendum on U.S. AI sentiment, it may not provide much diversification even if the business is domiciled elsewhere. If it responds more to order books, margin execution, service growth, or local industrial conditions, that is a sign the exposure may be functionally distinct.

A practical screening framework for investors

Step 1: Start with the bottleneck

Do not begin with a list of tickers.

Start with a bottleneck: power availability, transformer lead times, cooling density, semiconductor process inputs, or throughput constraints. This keeps the thesis tied to economics rather than branding.[^2]

Step 2: Identify non-U.S. suppliers with pricing power or scarce capacity

Look for companies that occupy a constrained layer of the chain. Scarce capacity, long lead times, qualification barriers, or embedded customer relationships are all encouraging signs.

Step 3: Check whether AI is incremental demand, not the entire story

This is one of the most useful filters.

If AI is the whole valuation story, you may simply be rebuilding concentration in a new wrapper. If AI adds demand to an already viable business, you may be finding better-balanced exposure.

Step 4: Stress-test customer concentration, cyclicality, and policy risk

Then do the hard part.

Ask how the thesis holds up if hyperscaler spending pauses, if an industrial downturn hits, if the local currency strengthens, or if policy and trade friction increase. International diversification helps only if the new risks are worth the concentration you remove.

Portfolio construction: how to use these exposures without overfitting the theme

Blending direct and indirect AI exposure

For most investors, these holdings should complement core AI exposure, not replace it.

A sensible portfolio often mixes direct AI leaders, selective semiconductor exposure, and second-order infrastructure or materials beneficiaries. That structure preserves upside to the theme while reducing dependence on one narrow layer of the stack.

Position sizing by sensitivity, not story appeal

Size positions based on economic sensitivity, not on how compelling the narrative sounds.

A power-equipment name with broad end markets may deserve a different weight than a semiconductor equipment name whose earnings are much more directly tied to the capex cycle. Lower sensitivity can mean lower upside, but it can also make the position easier to hold through volatility.

When ETFs may be more sensible than single-name bets

If disclosure is weak, project risk is binary, or your confidence in company-specific execution is limited, an ETF may be the better vehicle.

That is especially true in categories like industrials or international infrastructure, where the theme may be real but single-name attribution is messy.

What can go wrong

Capex digestion after a buildout surge

This is the big one.

Even if the long-term AI trend remains intact, short-term spending can overshoot and then pause. Indirect beneficiaries may still fall if customers spend a period digesting a burst of orders.[^2]

Margin disappointment despite strong demand

Demand alone does not guarantee earnings quality.

Microsoft has itself flagged margin pressure from scaling AI infrastructure.[^1] Suppliers can face their own version of that problem through input costs, execution bottlenecks, project mix, or under-earning during rapid growth.

Geopolitical, currency, and regulatory complications

International exposure can improve diversification, but it also adds FX risk, local regulation, and governance variation. Those risks are real and should be treated as part of the investment case, not as background noise.

False positives

This is the most common mistake.

Some businesses add “AI” to presentations without showing backlog, pricing power, capacity expansion, or customer demand that actually converts into revenue. If you cannot trace the pathway from AI capex to orders to margins, you probably do not have an investable spillover thesis.

The investor takeaway

Diversify across functions in the AI buildout, not just across countries

The best version of international diversification in an AI-heavy market is not a geographic rotation away from U.S. tech. It is a wider exposure to the global systems the AI buildout depends on.

Focus on economic linkage, not marketing language

That means asking harder questions. Which bottleneck am I owning? Who pays this company when AI capex rises? Is AI incremental demand or the entire story? Does this stock actually behave differently from my existing AI holdings?

Those questions lead to better diversification than simply buying foreign-listed tech.

Conclusion

If your portfolio already has heavy exposure to U.S. AI winners, the next step is not necessarily to reduce the theme. It may be to express it better.

The AI capex cycle is not confined to platforms and chips. It spills into electrical systems, cooling architecture, process materials, industrial inputs, and supply-chain infrastructure. That is where international diversification can become genuinely useful: not by changing the headline theme, but by changing the economic function you own within it.

The practical takeaway is straightforward. Start with bottlenecks. Follow the revenue pathway. Prefer real orders over AI storytelling. And remember that a foreign ticker is not automatically a diversifier if the same U.S. demand engine still sits underneath it.

FAQ

What does international diversification in an AI-heavy market actually mean?

It means broadening AI exposure beyond U.S. mega-cap platforms and chip leaders by owning non-U.S. companies that benefit from the same buildout through different economic functions. The goal is not to abandon AI, but to diversify how AI demand reaches your portfolio.

How can investors diversify within the AI capex cycle instead of away from it?

Start with the physical bottlenecks created by AI infrastructure spending: power distribution, cooling, factory automation, specialty materials, and supply-chain throughput. Then look for international companies whose revenue rises because those bottlenecks need to be solved, rather than companies that simply trade on AI headlines.

Why are many AI portfolios less diversified than they appear?

Because different funds, sectors, and even geographies can still depend on the same underlying drivers: U.S. hyperscaler capex, semiconductor demand, and a narrow group of sentiment leaders. Geographic variety does little if the revenue base and valuation behavior remain tied to the same buyers.

Which non-U.S. sectors are most relevant to AI capex spillover?

The strongest categories are usually power and electrification, industrial automation, specialty materials and process inputs, and selected logistics or enabling infrastructure. These areas can benefit from data-center expansion, grid constraints, semiconductor capacity growth, and supply-chain upgrades.

How do you tell real diversification from U.S. tech beta in another wrapper?

Look at who pays the company, how concentrated its customers are, whether AI demand is incremental or dominant, and what drives the stock in practice. If the company still rises and falls mainly with U.S. semiconductor sentiment or a handful of hyperscaler buyers, the diversification benefit may be limited.

Are non-U.S. semiconductor companies always good diversifiers for AI exposure?

No. Some are highly relevant to AI but still tightly linked to the same semiconductor capex cycle and customer concentration that dominate U.S. AI portfolios. A foreign listing changes the geography, but not necessarily the factor exposure.

What is an AI capex spillover beneficiary?

It is a company that benefits from second-order demand created by AI infrastructure spending rather than from direct ownership of AI platforms or software. Examples include suppliers of switchgear, cooling systems, industrial gases, substrates, factory controls, or warehouse automation.

What metrics should investors use to screen for international AI beneficiaries?

Useful signals include backlog growth, capacity agreements, service revenue, installed base expansion, pricing power, customer diversification, and explicit exposure to data-center, utility, semiconductor, or infrastructure demand. Management mentioning AI is much less useful than evidence of order flow and economic linkage.

Should these international AI exposures replace core U.S. AI holdings?

Usually not. For most investors, they work better as complements to core AI exposure because they often offer different operating drivers and less concentrated factor risk, though sometimes with lower direct sensitivity to AI upside.

What are the main risks of diversifying within the AI capex cycle internationally?

The biggest risks include a capex slowdown after a surge, margin pressure despite strong demand, customer concentration, cyclical weakness in industrial or utility markets, and international complications such as currency, regulation, governance, or geopolitics. There is also a risk of false positives, where a company sounds AI-linked but has weak economic leverage to the cycle.