How to Start Investing in 2026: A 60-Minute Setup for Your First Portfolio

Most beginners do not get stuck because investing is too hard. They get stuck because every early decision feels permanent. Which account? Which broker? How many funds? Stocks or bonds? U.S. or global? Invest now or wait?

The usual mistake is trying to solve all of that perfectly before opening anything.

A better approach is to build a minimum viable portfolio: a simple, diversified, automated setup that is good enough to start and sturdy enough to survive headlines. For most first-time investors, that matters more than theoretical optimization.

If you can choose the right account, buy one diversified fund or a simple stock-bond mix, automate contributions, and define one rebalancing rule, you are already ahead of many people who spend months researching and never begin.

How to start investing in 2026 without getting stuck

The fastest safe answer is simple:

- Choose the right account for the goal.

- Pick a basic diversified portfolio.

- Automate contributions.

- Rebalance rarely and by rule.

That is the whole system.

Why beginners overthink the first portfolio

Beginners often assume they need the best platform, the best allocation, the best tax setup, and the best market entry point before they can invest.

They do not.

What they need is to avoid obvious mistakes. Do not invest emergency cash you may need next month. Do not ignore high-interest debt. Do not put retirement money in the wrong kind of account if a tax-advantaged option is available. Beyond that, waiting often costs more than starting with a simple plan.

There is also a subtle trap here: optimization feels productive. Researching ten ETFs feels safer than buying one broad fund. In practice, complexity usually creates more ways to second-guess yourself later.

The article’s promise: a 60-minute minimum viable setup

This guide is not about the perfect portfolio. It is about building a first durable system.

By the end, you should be able to decide:

- which account to open

- what to buy

- how much to contribute

- when to rebalance

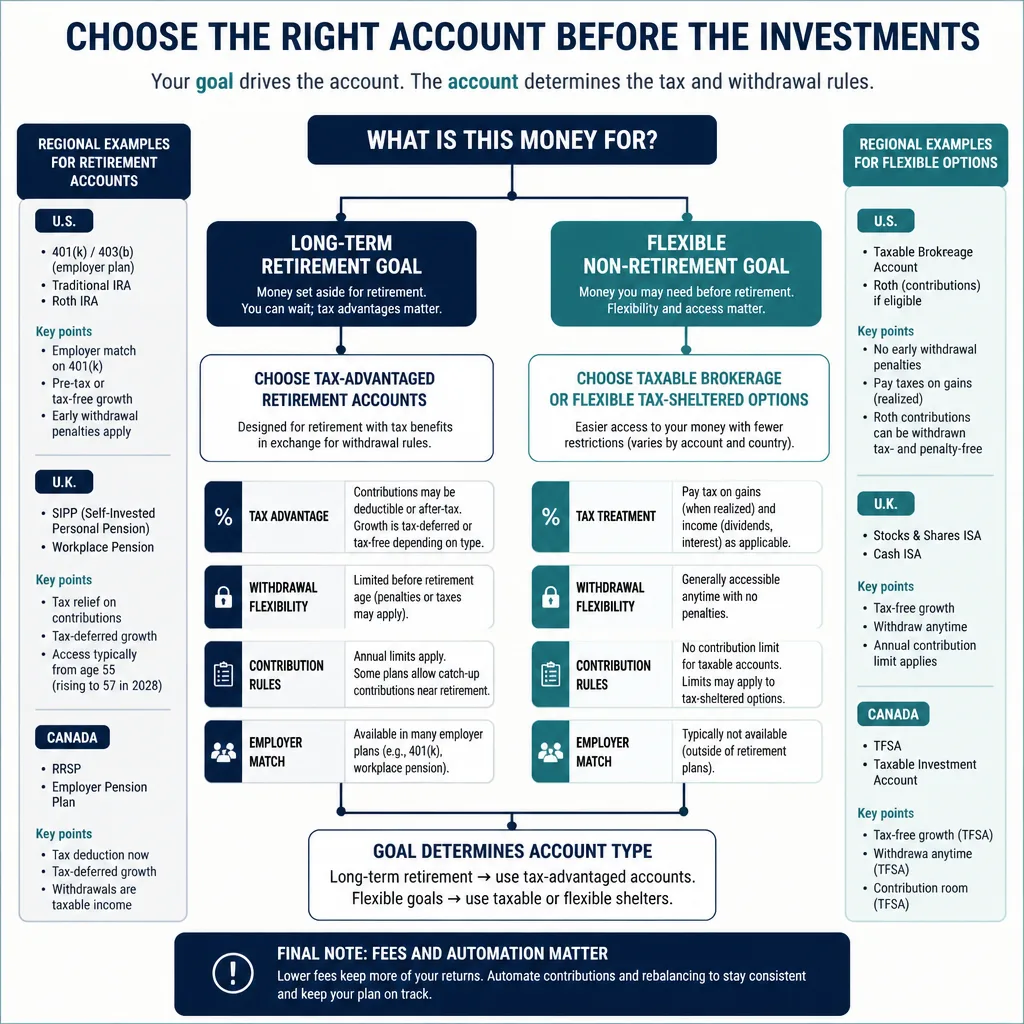

Step 1: Choose the right account before you choose investments

Account choice is not just paperwork. It affects taxes, withdrawal flexibility, contribution rules, and sometimes employer matching. Over time, that can matter as much as fund selection.[^1]

A useful sequence is:

goal -> account -> portfolio -> automation -> rebalance

That order cuts through a lot of noise.

Start with a tax-advantaged account if the goal is long term

If the money is for retirement or another long-horizon goal, a tax-advantaged account is often the first place to look.

In the U.S., that usually means an employer plan such as a 401(k) or an IRA. In the U.K., common starting points are an ISA or a pension wrapper such as a SIPP, with practical guidance from MoneyHelper. In Canada, the broad equivalents are the TFSA and RRSP.

The details differ by country and can change. The broader point does not: if your government offers a tax shelter for long-term investing, consider that before using a plain taxable account.

When a taxable brokerage account makes more sense

A taxable brokerage account can be the better starting point if:

- you may need the money before retirement age

- you want fewer withdrawal restrictions

- local retirement wrappers are less attractive in your situation

- you have already used the tax-advantaged options available to you

Some beginners get paralyzed here. They assume choosing taxable means they got it wrong. Not necessarily. A good account you understand and actually fund is usually better than the ideal account you never open.

A simple regional lens

At a high level:

- U.S.: retirement accounts like IRAs and 401(k)s often provide tax advantages, but contribution and withdrawal rules matter.[^1]

- U.K.: ISAs are valued for flexibility and tax treatment; SIPPs are more retirement-focused and more restrictive, but powerful for long-term saving.[^2]

- Canada: TFSAs and RRSPs have different tax mechanics, so the better choice depends on income, timeline, and flexibility needs.[^3]

This is intentionally high-level because tax advice is country-specific and changes over time. Official sources are more reliable than old forum threads.

What matters more than account perfection

Once you narrow the account type, keep your platform checklist boring:

- low account and fund fees

- access to broad index funds or ETFs

- easy automatic contributions

- low or no minimums

- decent usability

- withdrawal and transfer rules you understand

For a first account, convenience matters. Automation that actually works is more valuable than a broker with 400 features you will never use.

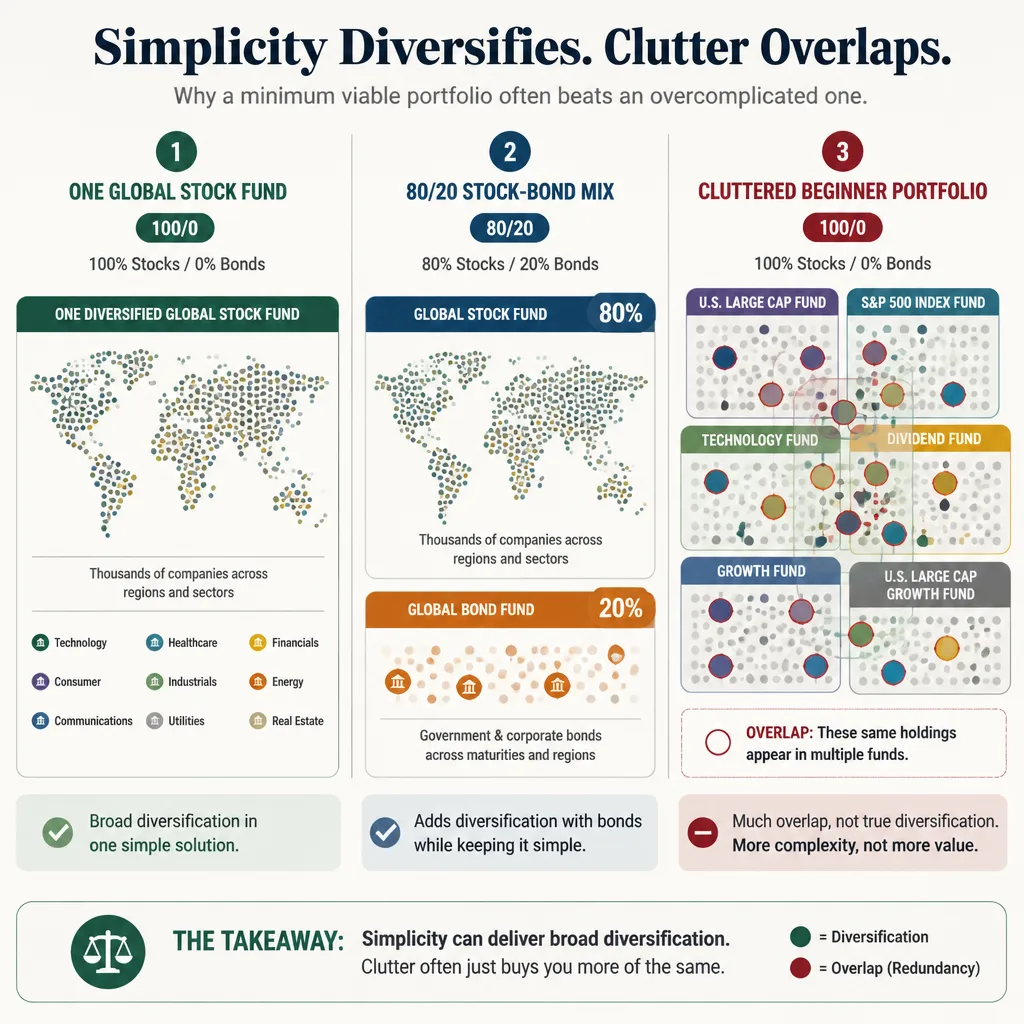

Step 2: Build a minimum viable portfolio

For most beginners, a first portfolio should do three things:

- diversify broadly

- stay understandable

- be easy to maintain

That usually points to one fund or two.

The simplest default: one broad stock fund, or a stock-bond pair

A one-fund portfolio can be completely reasonable if that fund already owns a broad global basket of stocks. One fund is not automatically simplistic. In many cases, it is more diversified than a six-fund beginner portfolio full of overlap.

If you want lower volatility, use two building blocks:

- a broad global stock index fund

- a broad investment-grade bond index fund

This is the key point many beginners miss: diversification comes from underlying holdings, not from collecting more ticker symbols.[^4]

How to choose your stock-bond mix

There is no universally correct starter allocation.

A better rule is to look at two things:

- Time horizon: How long until you may need the money?

- Behavioral durability: How much volatility can you handle without bailing out?

Expected returns matter. But realized returns depend on whether you stay invested. A portfolio that looks optimal on paper but causes you to sell during a 35% drawdown is not optimal in real life.

Example starter allocations: 100/0, 80/20, 60/40

These are not prescriptions. They are useful defaults.

100/0: all stocks

This can make sense if you have a very long time horizon, stable income, cash reserves, and a genuine ability to tolerate large declines.

The upside is higher expected long-term growth. The downside is obvious: steep drawdowns happen, and they can last. If a 40% decline would cause you to panic, this is too aggressive no matter how old you are.

80/20: mostly stocks, some bonds

For many beginners, this is the practical middle ground.

You still get substantial equity exposure, but the bond sleeve can reduce volatility and make the portfolio easier to stick with. That does not guarantee higher returns. It may simply improve the odds that you behave well.

60/40: balanced growth and stability

This is a reasonable option for shorter horizons, lower risk capacity, or anyone who knows they will struggle with equity-heavy swings.

It will usually have lower expected long-term returns than 100/0. It may also be the allocation you can actually hold through rough markets.

Why simplicity usually wins

Owning a U.S. total market fund, an S&P 500 fund, a tech ETF, a dividend ETF, and a growth fund does not mean you are five times more diversified. It often means you own many of the same companies again and again.

That is not diversification. It is clutter.

There is no strong universal evidence that beginners need more moving parts to succeed. The case for simplicity is partly behavioral and partly practical: fewer decisions, fewer chances to tinker, fewer tax headaches, and less confusion when markets fall.

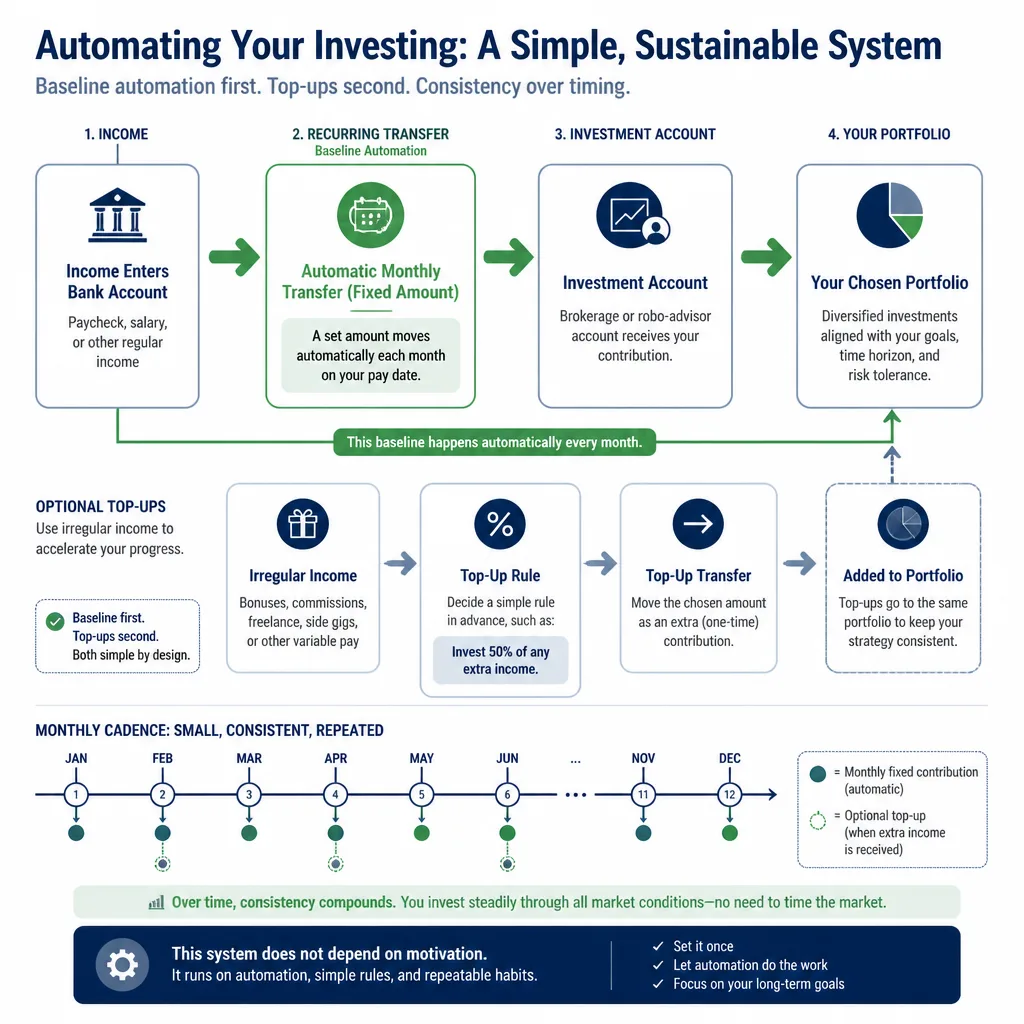

Step 3: Automate contributions so the plan does not depend on motivation

Automation does not guarantee better returns. What it usually does is reduce friction, procrastination, and the temptation to wait for a “better” entry point.

That matters because market timing is notoriously difficult, and missing major rebound periods can materially hurt long-run results.[^5]

Set a fixed monthly amount, not a market-timing rule

A clean default is to invest a fixed amount every month.

Not “only when the market drops 10%.” Not “after the election.” Not “once rates stabilize.”

Just monthly.

That shifts your system from prediction to process.

Choose an amount you can sustain

A good starter amount is one you can keep investing during a normal bad month.

That may sound modest. It is actually durable.

A beginner who invests $300 per month for years is in a far better position than someone who starts at $1,000, feels stretched, and stops after three months. Early on, consistency matters more than heroics.

If you can increase later, do it. Raises, bonuses, and debt payoff milestones are good moments to step up contributions.

What to do if your income is irregular

If your income moves around, do not force a rigid number that sets you up to fail.

A practical version is:

- set a low automatic baseline you can almost always afford

- add top-ups from larger paychecks, commissions, or bonuses

- if useful, tie top-ups to a rule, such as 10% or 15% of irregular income

That keeps the habit alive without overcommitting.

Step 4: Use one rebalancing rule and leave it alone

Rebalancing is maintenance. It is not a forecasting tool or a magic return enhancer.[^6]

Its main job is to keep your portfolio’s risk roughly aligned with your plan.

What rebalancing does and does not do

Rebalancing means bringing your portfolio back toward its target mix after markets move.

If stocks rise a lot, your 80/20 portfolio may drift to 86/14. Rebalancing nudges it back.

What it does not do:

- guarantee higher returns

- predict market turns

- eliminate losses

Treat it as risk control, not performance engineering.

Two simple methods

Most beginners only need one of these:

- Calendar-based: check once or twice a year

- Threshold-based: rebalance only when an allocation drifts by, say, 5 percentage points from target

Either can work. What matters is having a rule before emotions get involved.

A simple written version might be:

I contribute monthly, hold a global stock fund and a bond fund at an 80/20 target, and only rebalance in January or if either allocation drifts by more than 5 percentage points.

That is enough.

Why frequent tinkering usually hurts

Frequent changes create two problems.

First, they raise behavioral risk. The more often you check and adjust, the more likely you are to react to noise.

Second, in taxable accounts, unnecessary trades can create tax consequences. Exact rules vary by country, but the general point is stable: overactivity has costs.[^1][^2][^3]

The two mistakes that derail new investors

These are usually more damaging than picking the “wrong” fund from a shortlist of good options.

Mistake 1: Starting with too much complexity

Complexity feels sophisticated. For a beginner, it is often just a larger surface area for mistakes.

A portfolio with seven funds, three themes, and a watchlist of tactical ideas may be interesting. It is rarely necessary. If each new position adds monitoring, explanation, and temptation, the portfolio becomes harder to hold.

A first portfolio should be boring enough to survive your moods.

Mistake 2: Changing the plan after headlines, crashes, or rallies

This is the classic failure mode.

Stocks fall 15%, and a new investor decides to “wait for clarity.” Stocks rally hard, and the same investor decides they “missed it” and buys a hot sector instead.

Neither move is based on process.

Investor behavior has long been a weak point in real-world results. Studies often show that the timing of investor cash flows can reduce realized returns relative to the funds themselves, though the exact size of that gap is debated and depends on methodology.[^7] The direction of the problem matters more than the exact number: reacting to headlines usually makes long-term investing worse.

A 60-minute checklist for your first portfolio

This is what “good enough to launch” looks like.

Minutes 0–15: account choice

Decide:

- Is this money for retirement or a flexible non-retirement goal?

- Is there a tax-advantaged account in my country that fits that goal?

- Does my employer offer a retirement plan or match?

- Which platform gives me low fees and easy automation?

Minutes 15–35: portfolio selection

Choose one of these broad setups:

- one globally diversified stock fund

- a two-fund portfolio: global stock fund + bond fund

Then choose a target mix:

- 100/0 if you can truly tolerate major volatility

- 80/20 if you want growth with some ballast

- 60/40 if stability matters more

Minutes 35–50: automation setup

Set up:

- automatic transfers from your bank account

- automatic investment into your chosen fund or allocation

- a sustainable monthly amount

If income is uneven, set a baseline plus a top-up rule.

Minutes 50–60: write your one-paragraph investment rule

Write it in plain English. Example:

My goal is long-term investing. I will use a tax-advantaged account where appropriate, invest monthly into a simple diversified portfolio, and avoid changing my allocation because of market news. I will review the account once a year and only rebalance if my target allocation drifts materially.

This sounds small. It is not. Pre-committing to a rule before volatility arrives is one of the most useful things a beginner can do.

What matters after setup

Once the account is open and funded, the game changes.

The main question is no longer “Did I choose perfectly?” It is “Can I keep this going?”

Track progress by savings rate and consistency, not daily returns

Daily returns are noisy and often emotionally unhelpful.

Early on, better signals are:

- contribution consistency

- savings rate

- whether your asset mix still fits your goals

- whether you are staying invested

A simple portfolio with regular contributions can do a lot of work quietly over time.[^4]

When to upgrade the portfolio later, if ever

You do not need to “graduate” from a simple portfolio just because you learned more.

Change the setup only if something material changed:

- your goals changed

- your timeline changed

- your original allocation was emotionally too aggressive or too conservative

- tax rules or account access changed

- you found a simpler structure, not a more exciting one

That last point matters. The first portfolio is not supposed to impress anyone. It is supposed to function.

Conclusion

For most beginners, the best first portfolio is not the most optimized one. It is the one you can understand, automate, and stick with when markets get uncomfortable.

That usually means choosing the right account for the goal, buying one diversified fund or a simple stock-bond mix, investing on a fixed schedule, and rebalancing by rule instead of emotion.

If you are stuck, shrink the task. You do not need a final investing philosophy today. You need a durable first system.

Done well, your first hour of setup can remove years of hesitation. In investing, starting with a sensible plan usually matters far more than perfecting one.

FAQ

What is the fastest safe way to start investing in 2026?

Keep the first setup simple: choose the right account for your goal, buy one diversified fund or a basic stock-bond mix, automate contributions, and use a clear rebalancing rule. The goal is a durable system, not a perfect portfolio.

Should I open a retirement account or a taxable brokerage account first?

Usually, a tax-advantaged retirement account comes first if the money is for long-term goals and your region offers one. A taxable brokerage account can make more sense when flexibility, easier access, or non-retirement goals matter more. The right choice depends on tax rules, withdrawal constraints, and your timeline.

Can I start investing with just one fund?

Yes. A single globally diversified fund can be enough for a first portfolio if it already holds broad stock market exposure. For some investors, a one-fund setup is simpler and more diversified than owning several overlapping funds.

How do I choose between 100/0, 80/20, and 60/40?

Use two filters: your time horizon and your ability to stay invested during market declines. A higher stock allocation may offer higher expected long-term returns, but only if you can hold it through large drawdowns. A slightly more conservative mix can be the better real-world choice if it helps you stick to the plan.

How much should I invest each month as a beginner?

Start with an amount you can sustain even in a normal bad month. Consistency matters more than ambition at the beginning. If your income is irregular, use a low baseline contribution and add top-ups when income is higher.

Should I wait for a better time to invest?

Usually no. Waiting for the perfect entry point often turns into delay. Market timing is extremely difficult in practice, and missing strong recovery periods can meaningfully reduce long-term results. Automation helps reduce this behavior risk, though it does not guarantee better returns.

How often should a beginner rebalance a portfolio?

For most beginners, simple and infrequent is enough. A common approach is to rebalance once or twice a year, or only when your allocation drifts by a set amount such as 5 percentage points. Rebalancing is mainly a risk-control tool, not a return-maximizing strategy.

What are the biggest mistakes new investors make?

Two common mistakes are starting with too much complexity and changing the plan after scary headlines, crashes, or rallies. Both increase the odds of confusion, second-guessing, and poor timing decisions.

What should I do if the market falls right after I invest?

If your portfolio matches your timeline and risk tolerance, the default response is usually to keep contributing and avoid reacting. Early declines are uncomfortable, but changing a long-term plan because of short-term moves is one of the most common ways investors hurt their results.

Should I build an emergency fund or pay off debt before investing?

Often, yes. If you have no cash buffer or carry high-interest debt, fixing that first can be the better move. Investing works best when you are not likely to sell during a short-term cash emergency and when guaranteed debt costs are not overwhelming uncertain market returns.