Most investors make the same mistake with future-facing themes: they ask which story sounds biggest, not which trend is most likely to show up in earnings, cash flow, and capital allocation before 2027.

That distinction matters. A theme can be economically important and still be a poor investment if expectations are already extreme, margins disappoint, or the path from excitement to profits takes longer than the market is willing to wait.

The trends worth watching now are not necessarily obscure. Some are already widely discussed. The harder question is where investable opportunity still exists, what could go wrong, and which signals would show that a thesis is becoming real rather than merely popular.

Emerging investing trends for 2027: what matters most

If you want the short version, five themes stand out heading into 2027:

- AI shifts from infrastructure spending to monetization

- Industrial policy and supply-chain redesign keep capital spending elevated

- The energy transition becomes more selective, with power and grid bottlenecks taking center stage

- A higher cost of capital continues to reshape valuations and business models

- Market dispersion may create more room for selectivity than broad beta alone

These themes matter because each has a plausible route into business results. Hyperscalers are already spending heavily on AI infrastructure.[^1] U.S. manufacturing construction has surged as semiconductor and industrial projects move forward.[^2] Electricity demand expectations are rising again, partly because of data centers and electrification, putting grid investment and reliability back in focus.[^3] And even if policy rates ease somewhat, the era of nearly free capital that defined much of the 2010s still looks far away.[^4]

That does not mean the returns will be easy. Some of these trades may already be crowded. Others depend heavily on policy, permitting, or execution. The opportunity is real. So is the risk of overpaying for it.

How to think about 2027 trends without chasing headlines

Good trend investing is less about prediction than filtration. The job is to separate structural change from narrative momentum.

A powerful theme is not always a good investment

This is where many investors slip. Technological change can be real, demand can be real, and the stocks most closely tied to the story can still disappoint.

Usually that happens for one of three reasons:

- expectations got too high

- competition reduced profit capture

- the investment cycle arrived before the monetization cycle

The dot-com era is still the clearest example. The internet changed everything. Many investors still lost money because they paid for certainty long before the economics were visible.

The same logic applies now. AI may reshape software, labor productivity, and enterprise spending. Clean power investment may rise for years. Strategic manufacturing may remain politically important. None of that guarantees that the most obvious securities offer the best forward returns.

What matters more than the story: timing, valuation, and expectations

“Priced in” is often used lazily, but the basic idea is simple. If investors already expect rapid growth, strong results may not be enough. A company has to beat assumptions that are already demanding.

That is why trend investing works better when you track three things at once:

- the durability of the driver

- the visibility of earnings and cash flow

- the gap between reality and expectations

A theme gets interesting when those three line up. It gets dangerous when only the story is strong.

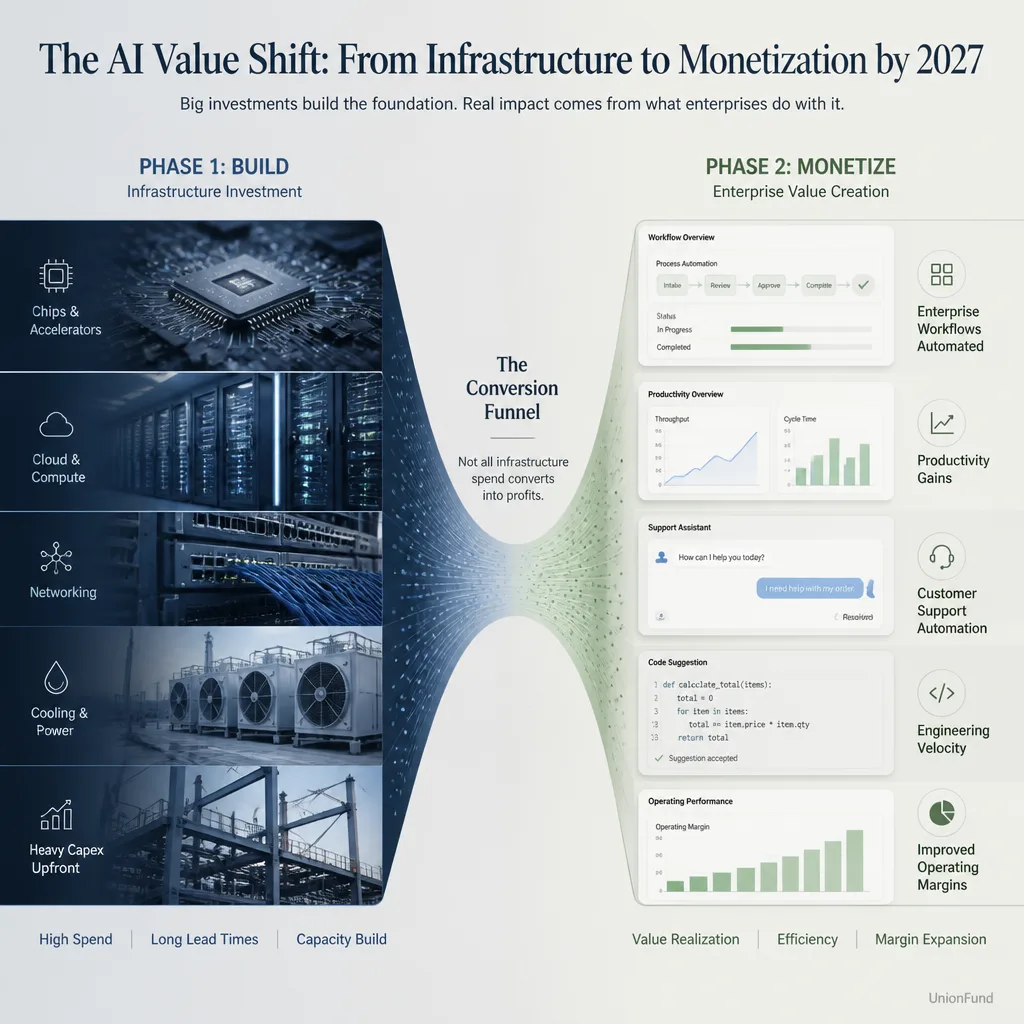

Trend 1: The next phase of AI moves from infrastructure to monetization

The first phase of the AI boom was easy to spot. Chip demand, cloud capacity, and data-center spending showed up quickly in guidance and capex plans from companies such as Microsoft, Alphabet, Amazon, and Meta.[^5]

By 2027, the market may care less about who is spending and more about who is earning.

Why this trend could remain durable

The case is straightforward. Enterprise adoption is still early, model performance keeps improving, and major companies are treating AI as core infrastructure rather than an experimental side project.[^6]

The most credible beneficiaries may extend beyond the headline names. Think about:

- enterprise software companies that can charge for AI-driven workflow gains

- data infrastructure and networking firms supporting heavier workloads

- power and cooling suppliers tied to data-center buildouts

- businesses that use AI to improve margins rather than sell AI directly

That last group is easy to miss. If AI lowers service costs, speeds up coding, improves ad targeting, or reduces support headcount, some of the best winners may be ordinary-looking businesses with better unit economics.

Where investors may be overestimating upside

The weak point in the bullish case is monetization. Plenty of companies can show AI activity. Fewer can show durable pricing power from it.

There are real risks. Open-source models may limit moats. Inference costs may stay higher than expected. Customers may resist paying large premiums for features that quickly become standard. Regulators may also shape product design and liability.

So the AI theme looks credible. The assumption that all visible leaders will keep compounding at the same rate does not.

What to watch before treating AI as a 2027 winner

Watch for evidence that AI is broadening beyond capex headlines:

- AI-related revenue becoming material in software results

- enterprise IT budgets shifting from pilot projects to recurring deployments

- falling inference costs

- margin improvement tied to AI-enabled productivity

- earnings revisions broadening beyond a handful of mega-cap firms

If the gains remain concentrated in infrastructure suppliers, the theme may still be real but narrower than many investors expect.

Trend 2: Industrial policy, supply-chain redesign, and the return of capital spending

For years, investors were trained to prefer asset-light growth. That instinct may be less useful in a world where resilience, domestic capacity, and strategic manufacturing matter more.

Why this is bigger than a short-term policy story

The CHIPS and Science Act and the Inflation Reduction Act helped accelerate the shift, but the deeper driver is geopolitical and operational, not just legislative.[^7] Companies and governments want redundancy in semiconductors, energy systems, and critical supply chains.

That is why U.S. manufacturing construction has risen sharply, especially in computer, electronics, and electrical segments.[^2] Similar logic is visible in parts of Europe and Asia, even if the policy mix differs.

Potential beneficiaries include:

- semiconductor equipment and fabrication ecosystems

- industrial automation

- capital goods suppliers

- logistics and infrastructure providers

- utilities serving new industrial loads

The execution and margin risks investors often miss

Announced spending is not the same as profitable spending.

Obvious, yes. Easy to forget, also yes. Large projects can run into labor shortages, permitting delays, cost overruns, and weak returns on capital. A factory opening is good for headlines. It is not automatically good for shareholders.

This is a theme where second-order beneficiaries may sometimes be cleaner than project owners themselves. Equipment vendors, engineering firms, and specialized suppliers may carry less balance-sheet risk than companies trying to build entire strategic ecosystems from scratch.

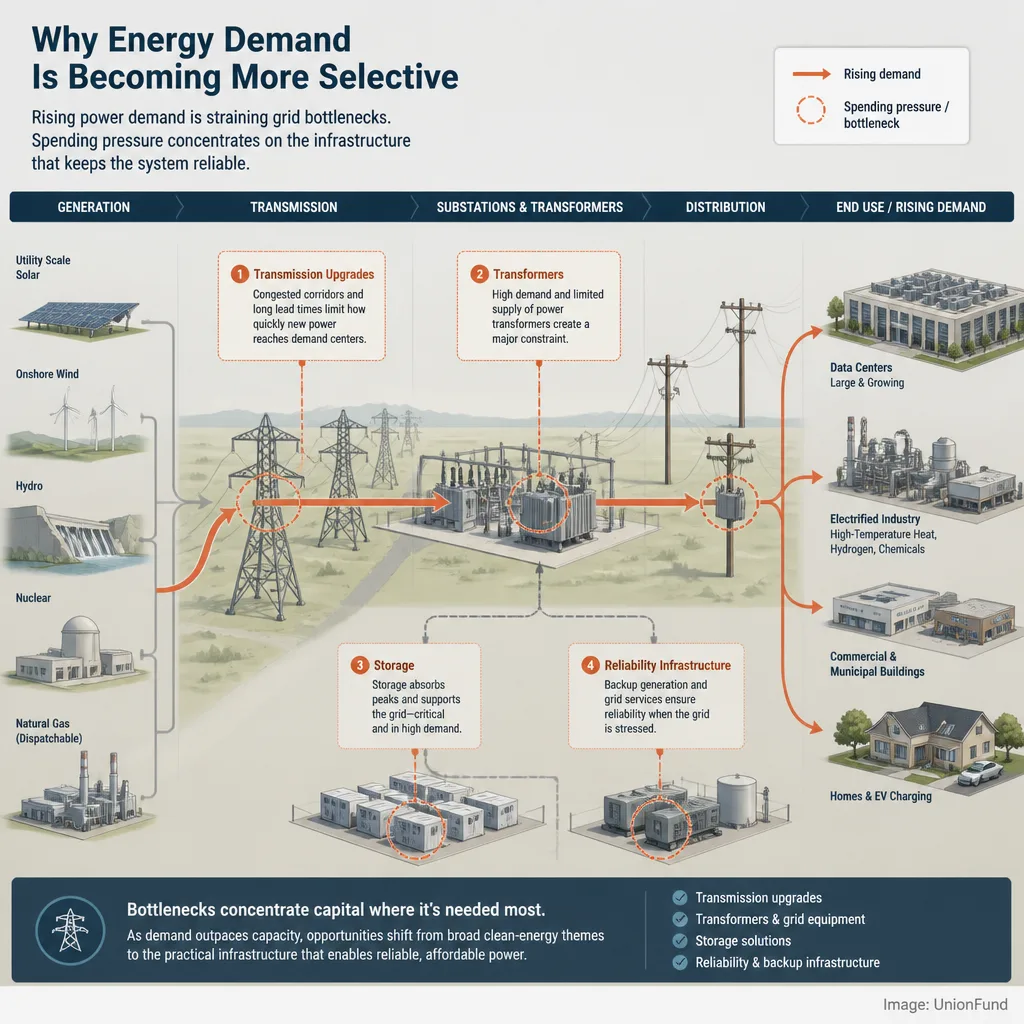

Trend 3: The energy transition becomes more selective

Broad clean-energy enthusiasm has already been tested by higher rates, policy uncertainty, and uneven demand. By 2027, the investable energy story may look narrower and more practical.

Why energy demand could reshape the opportunity set

The power system is under pressure from several directions at once: electrification, industrial demand, grid aging, and rapid data-center growth.[^3][^8]

That points investors toward bottlenecks, not slogans.

More interesting areas may include:

- transmission and grid modernization

- transformers and electrical equipment

- battery storage

- natural gas backup generation

- nuclear and uranium exposure where policy support improves

This is one of the clearest cases where second-order beneficiaries may matter more than the most talked-about green brands. If utilities and grid operators are forced to spend, earnings power can become easier to see.

Why some green narratives may struggle by 2027

Not every transition segment has the same economics. Some remain heavily dependent on subsidies, favorable financing, or unusually tight supply-demand conditions. Solar manufacturing, EV supply chains, and hydrogen are obvious examples where long-term promise can coexist with poor near-term profitability.

A real theme can still be a bad trade when capital intensity is high and returns are thin.

Trend 4: Higher-for-longer capital costs change which business models work

Even if central banks cut rates from peak levels, investors should not assume a full return to the ultra-cheap capital regime of the 2010s.[^4][^9]

The market impact goes beyond bond yields

A higher cost of capital changes much more than discounted cash-flow models. It affects refinancing risk, acquisition math, property values, private-market marks, and how patient investors are willing to be.

Commercial real estate is the obvious pressure point, but not the only one. Any business model that depends on constant cheap funding becomes more fragile when real yields stay elevated and lending standards tighten.[^10]

What kinds of companies may benefit or suffer

This environment tends to favor:

- strong free cash flow

- low leverage

- pricing power

- short-duration earnings, meaning profits are visible sooner rather than far in the future

It tends to pressure:

- speculative growth with weak margins

- highly leveraged real estate structures

- small firms dependent on external financing

- private-market strategies built on easy refinancing assumptions

The key insight is simple: a decent business becomes more valuable when capital is scarce, and a fragile business becomes more obviously fragile.

Trend 5: Active management may regain relevance in a less uniform market

This is the most conditional theme on the list, but it is still worth watching.

Why broad beta may not tell the full story

Recent years have been marked by high index concentration, especially in the S&P 500.[^11] When leadership is narrow, owning the index can feel like owning the winners by default. A more uneven market can change that.

If earnings dispersion widens, sector fundamentals diverge, and regulation hits companies unevenly, selectivity becomes more useful. That does not automatically mean traditional active funds win. It does suggest that equal-weight approaches, factor tilts, or carefully targeted active exposure may become more relevant.

Where investors should stay skeptical

The caution matters. Long-run evidence from SPIVA and other scorecards still shows that many active managers underperform after fees.[^12]

So the claim here should stay modest. The environment may become more favorable for selection. That is not the same as saying most selectors will suddenly outperform.

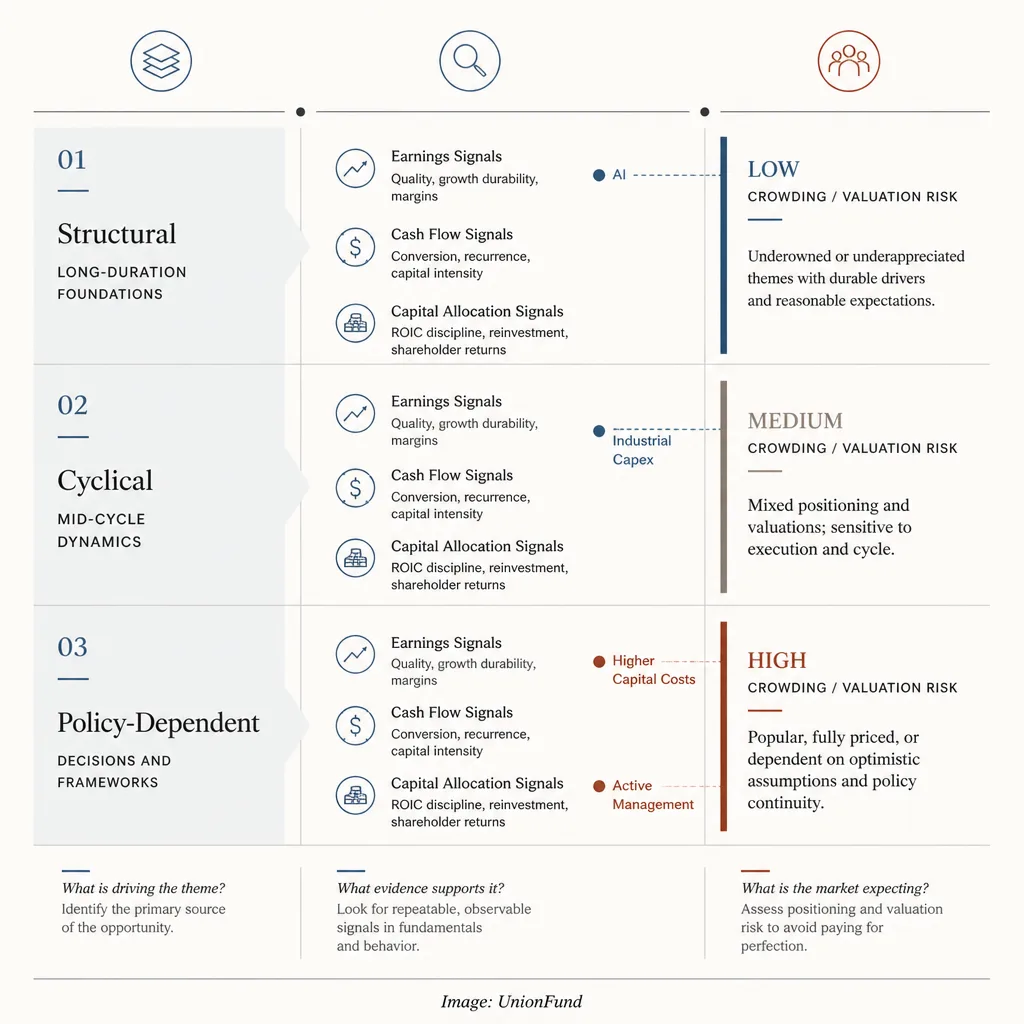

Which trends look investable, and which are mostly narratives

A useful way to rank these themes is to ask four questions: Is the driver durable? Is the earnings impact visible? How policy-dependent is it? How crowded is the trade already?

| Theme | Durability | Earnings visibility | Policy dependence | Crowding risk |

|---|---|---|---|---|

| AI monetization | High | Medium, improving | Medium | High |

| Industrial policy/capex | Medium-high | Medium | High | Medium |

| Selective energy infrastructure | High | Medium-high | Medium | Medium |

| Higher capital costs | High | High | Low-medium | Lower as a theme, high in affected sectors |

| Active management/dispersion | Medium | Indirect | Low | Low |

The most investable themes are often the ones with a clear structural driver and still-developing earnings visibility. That is one reason selective energy infrastructure and second-order AI beneficiaries may deserve more attention than the loudest narrative leaders.

A simple framework for evaluating 2027 investment themes

Is the driver structural, cyclical, or policy-dependent?

Structural drivers tend to last. Cyclical drivers can reverse quickly. Policy-driven drivers can be powerful, but they carry implementation risk.

Reshoring is a good example. The resilience trend looks structural. Specific subsidy outcomes are policy-dependent.

Is the opportunity visible in earnings, cash flow, or only in storytelling?

This filter removes a lot of weak thematic ideas.

If a company cannot explain where the revenue, margin, or cash-flow lift will come from, you may be looking at a story rather than an investment case.

How crowded is the trade already?

Crowding shows up in stretched valuation multiples, one-sided sentiment, and the assumption that strong growth is inevitable.

A crowded trade can keep working. It just becomes less forgiving. When expectations are high, execution has to be close to flawless.

What investors should watch between now and 2027

A smart watchlist is better than a bold forecast.

Monitor these signals:

- real yields and central bank guidance from the Federal Reserve, ECB, and Bank of England

- credit spreads and bank lending standards

- enterprise AI spending and cloud growth tied to AI workloads

- earnings revisions outside the biggest technology names

- manufacturing construction and capital goods orders[^2]

- utility capex plans, power demand forecasts, and grid bottlenecks from sources such as the IEA and EIA[^3]

- valuation spreads and market breadth

- commercial real estate stress and refinancing calendars

- policy shifts affecting chips, energy permitting, trade, and subsidies

The point is not to predict every move. It is to notice when a theme starts showing up in hard data.

Conclusion

The most important themes heading toward 2027 are likely to be the ones that move from narrative to measurable economics.

AI is the clearest example. The story is already enormous. The next question is who actually monetizes it. Industrial policy and supply-chain redesign look durable, but they are more likely to reward disciplined execution than big announcements. The energy transition may offer better opportunities in bottlenecks and infrastructure than in broad clean-tech enthusiasm. And a world with more expensive capital should keep separating robust business models from fragile ones.

One principle is worth keeping in view: the best trend is not the one attracting the most attention. It is the one becoming visible in earnings, cash flow, and capital allocation before the market fully treats that visibility as obvious.

FAQ

What are the most important investing trends to watch for 2027?

The most credible themes heading into 2027 likely include AI moving from infrastructure spending to monetization, industrial policy and supply-chain redesign, selective energy and grid investment, the effects of higher capital costs, and greater market dispersion that could reward selectivity.

How can investors evaluate future investment trends without chasing hype?

Start by asking whether the driver is structural, cyclical, or policy-dependent. Then check whether the theme is visible in earnings, cash flow, and capital allocation rather than only in headlines. Finally, assess valuation, crowding, and what assumptions the market has already priced in.

Is AI still likely to be a major investing theme by 2027?

Possibly, but the focus may shift. By 2027, investors may care less about raw AI infrastructure spending and more about which companies turn AI into recurring revenue, productivity gains, pricing power, or margin improvement. That makes monetization and execution more important than narrative strength alone.

What does it mean when a trend is already priced in?

A trend is partly priced in when stock prices and valuation multiples already reflect high expectations for future growth. That does not mean the trend is false. It means strong business performance may no longer be enough if results fail to exceed what investors already expect.

Why could the energy transition become more selective by 2027?

Because the investable opportunity may center less on broad clean-energy enthusiasm and more on bottlenecks that force real spending. Grid equipment, transmission, storage, backup generation, and nuclear-related areas may matter more than segments that remain heavily exposed to policy shifts, oversupply, or weak unit economics.

How does a higher-for-longer cost of capital affect investing trends?

Even if rates fall from peak levels, capital may remain more expensive than it was in the 2010s. That tends to favor companies with strong free cash flow, lower leverage, and shorter-duration earnings, while putting pressure on business models that rely on cheap financing or distant profit expectations.

Could active management become more relevant by 2027?

It could become more relevant in parts of the market if earnings dispersion, regulation, and sector differences widen. Investors should still stay skeptical. A more favorable environment for stock selection does not erase the long-running evidence that many active managers underperform after fees.

What signals should investors monitor between now and 2027?

Useful signals include central bank rate paths, real yields, credit spreads, earnings revisions, AI-related enterprise spending, manufacturing construction, semiconductor and grid capex, power demand forecasts, utility investment plans, valuation spreads, and market breadth.