Liquidity Mismatch Is the Silent Killer: How to Stress-Test Portfolios When Clients Can Withdraw Anytime

A portfolio can look diversified, income-producing, even conservative on a volatility screen, and still break at the moment that matters: when clients want cash in a stressed market.

That is liquidity mismatch. Usually not a dramatic day-one collapse, but an operational failure. Withdrawals rise, market depth disappears, and the assets you can sell are not the ones you want to sell.

Most portfolio conversations still focus on return, drawdown, and correlation. Those matter. But if clients can withdraw at any time, the harder question is this: can the portfolio raise cash when cash is needed without damaging what remains? That is a portfolio design problem, not just a market problem.

Liquidity mismatch starts in portfolio design

Liquidity risk is often treated as a niche issue for funds with gates, lockups, or private holdings. That is too narrow. Even a plain multi-asset portfolio can be mismatched if client cash needs are short-term and the assets expected to fund them become costly to sell under stress.

The issue has two sides:

- Supply: what the portfolio can turn into cash, how quickly, and at what likely cost

- Demand: what clients may withdraw, when they may need it, and how behavior changes under stress

A portfolio holds up only if those two still match when markets stop behaving normally.

What investors often miss

The common mistake is to confuse daily pricing or daily tradability with dependable liquidity.

An asset may trade every day and still be hard to exit in meaningful size. Bid-ask spreads widen. Depth vanishes. Quoted prices remain, but executable prices get worse. In credit markets, that distinction matters. The ability to trade is not the same as the ability to raise cash efficiently.

Private assets create a more obvious version of the same problem. They may not reprice every day, but the absence of visible volatility is not the same as safety. Sometimes it only means repricing happens more slowly.

Why this matters more now

This issue matters more in a higher-rate world because tighter financial conditions can raise refinancing risk, pressure weaker borrowers, and widen credit spreads during stress. That does not guarantee a liquidity event. It does mean assumptions formed during easy-money years deserve another look.

The second shift is structural. Private credit, interval funds, tender-offer funds, evergreen structures, and non-traded real asset vehicles now sit deeper inside wealth portfolios. That can be perfectly reasonable. But it turns liquidity from an institutional fund-structure issue into an everyday portfolio construction issue.

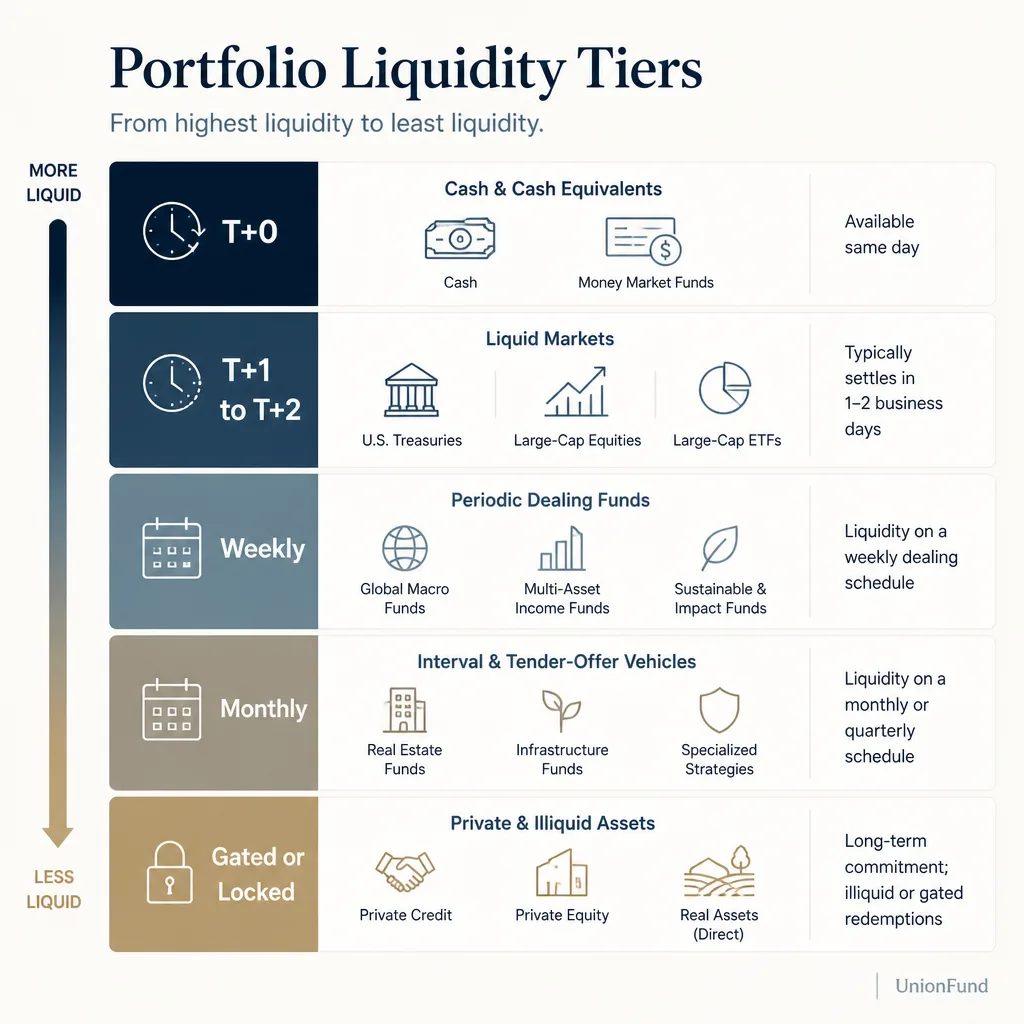

Start by mapping the portfolio into real liquidity tiers

“Liquid” and “illiquid” are too blunt. What you need is a practical map of how quickly holdings can become cash, and what could get in the way.

A simple tiering system works

| Liquidity tier | What it includes | What to watch |

|---|---|---|

| T+0 | Cash, bank sweep balances, some money market holdings | Operational access, counterparty rules |

| T+1 to T+2 | Treasuries, large-cap equities, many ETFs, investment-grade bonds | Size sensitivity, spread widening, settlement timing |

| Weekly / periodic | Funds with scheduled dealing windows | Notice periods, limited redemption capacity |

| Monthly / less frequent | Interval or tender-offer style vehicles, some real asset funds | Repurchase limits, queue risk, valuation lag |

| Gated / locked | Private credit drawdown funds, private equity, direct real assets | Lockups, transfer restrictions, gate provisions |

This is not about false precision. It is about forcing the portfolio to tell the truth.

A 10% allocation to private credit may sound modest. But in a portfolio serving clients with uncertain withdrawal needs, that 10% is also a claim on future flexibility.

Tradable is not the same as dependable

A better test is not just, “Can I sell this?” but, “Can I sell enough of it, fast enough, without taking an ugly discount?”

ETF investors saw this during periods of credit stress. ETF shares may keep trading while the underlying bond market becomes harder to price and less liquid. That does not mean the ETF structure failed. Often the ETF is simply providing real-time price discovery while the underlying market adjusts more slowly. From a liquidity-planning perspective, though, it still matters. Tradable does not always mean painless.

March 2020 was the clearest recent reminder that even high-quality fixed income segments can go through severe liquidity stress before policy support restores market functioning.

Model the other side: when clients may want cash

Many liquidity reviews stop at the asset side. That misses half the problem.

A portfolio is not just a set of holdings. It is a set of holdings owned by people with different spending needs, different outside resources, and different tolerance for bad headlines.

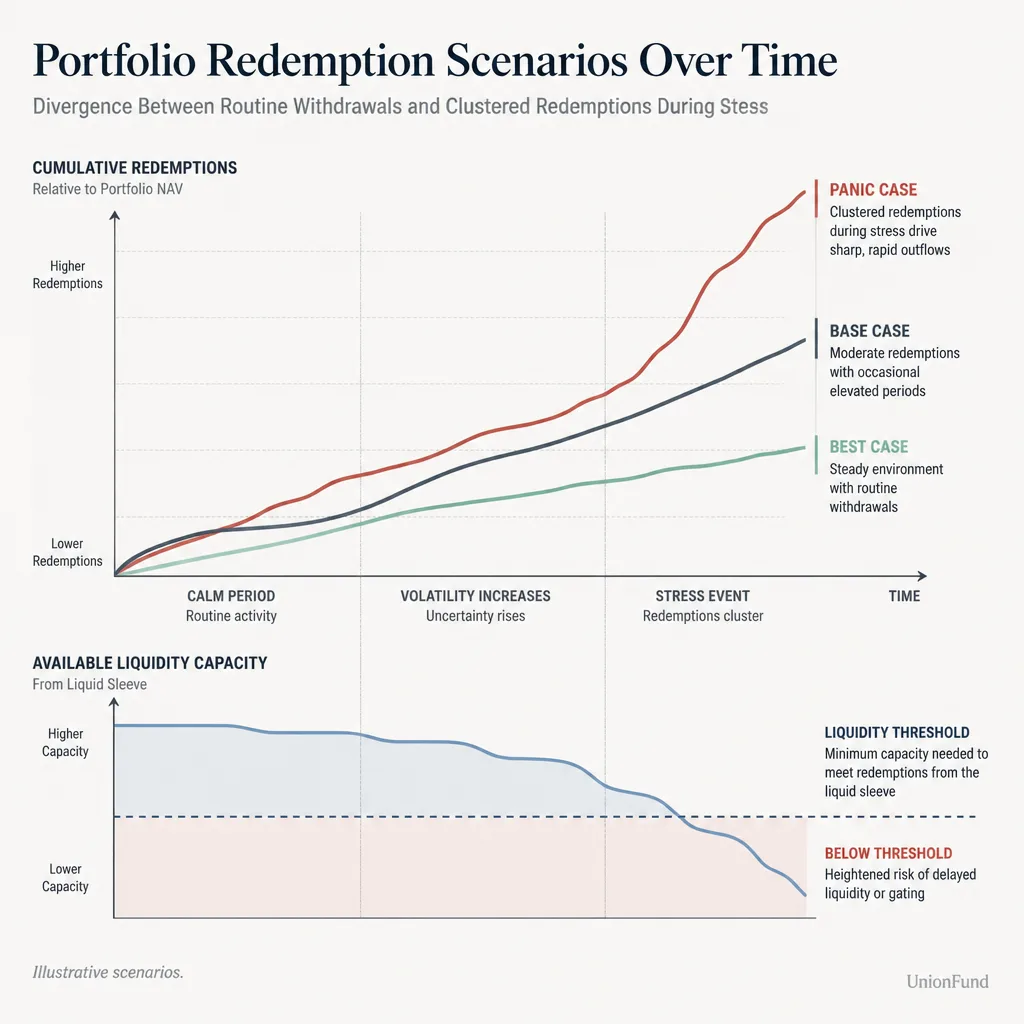

Build three redemption cases

You do not need a heroic model. Three cases are usually enough:

- Best case: ordinary withdrawals, planned distributions, normal spending needs

- Base case: moderate market stress, some client anxiety, withdrawals above normal

- Panic case: clustered withdrawals during a sharp drawdown, possibly alongside negative headlines and cross-asset volatility

These are not forecasts. They are planning cases.

Take a balanced portfolio with 55% public equities, 25% high-quality bonds, 10% short-term liquidity, and 10% private credit. In calm conditions, that mix looks sensible. In a panic case, the liquid sleeve may fund nearly all withdrawals. Six months later, the remaining client may own a portfolio with less cash, fewer defensive bonds, and a higher effective weight in private credit than intended.

That is the hidden damage. The problem is not only meeting redemptions. It is what redemptions leave behind.

Behavior belongs in the model

Client behavior is not an unpredictable nuisance outside the model. It is part of the model.

A retiree drawing income is different from a high-net-worth client with ample outside liquidity. A concentrated client base behaves differently from a broad one. Clients who sold in prior drawdowns are different from clients who stayed put.

Headline liquidity ratios can be misleading if the investor base is mixed. One segment may be stable long-term capital. Another may need cash quickly. The relevant unit is not just the model portfolio. It is the model portfolio plus the likely behavior of its owners.

A useful stress test asks one question: what must you sell, and when?

Once you map liquidity supply and model liquidity demand, the exercise becomes concrete.

The question is not “Is this portfolio diversified?” It is “If cash leaves in a bad market, what gets sold first, on what timeline, and what does the portfolio look like afterward?”

Test market stress and withdrawal stress together

A useful liquidity stress test combines cash needs with market dislocation. Scenarios might include:

- a gap-down equity open

- sharp credit spread widening

- thinner dealer balance-sheet support in rates or credit markets

- ETF discounts or premiums widening relative to NAV

- foreign-market holidays or settlement frictions

- simultaneous spikes in client withdrawals

If you test only drawdowns, you may miss the funding problem. If you test only withdrawals in calm conditions, you may miss the execution problem. The mismatch shows up when both happen at once.

Track first-sale risk and forced-sale risk

Two risks deserve names.

First-sale risk is the tendency to meet redemptions by selling the cleanest, easiest assets first: cash, Treasury bills, large-cap equities, liquid ETFs.

Forced-sale risk comes later. If outflows continue, the portfolio eventually has to sell what remains, often with worse pricing, worse liquidity, and worse portfolio consequences.

That is why some portfolios look fine on day one of stress and fragile by month three. They can meet initial cash needs, but only by stripping out their best collateral, best hedges, or highest-quality liquid assets.

Build a liquidity buffer with rules, not instinct

A liquidity buffer is not a vague comfort blanket. It has a specific job: absorb foreseeable cash demands without forcing immediate sales of risk assets into a stressed market.

What belongs in the buffer

For most portfolios, the buffer should favor confidence of convertibility over incremental yield.

That usually points to instruments such as:

- cash

- Treasury bills

- government money market funds, where appropriate

- short-duration high-quality government exposure

The principle matters more than the list. A short-duration credit fund may have low duration risk and still be the wrong buffer asset if liquidity dries up when risk sentiment turns.

The temptation to pick up a little extra yield inside the liquidity sleeve is understandable. It is also how buffers quietly stop being buffers.

Replenishment needs rules

There is no universal cash-buffer percentage that fits every investor, advisor, or strategy. Buffer size depends on withdrawal uncertainty, contribution patterns, client concentration, liability timing, and how quickly the rest of the portfolio can realistically be liquidated.

What matters more than the exact number is the rule set.

A good policy usually defines:

- a minimum buffer threshold

- how often the buffer is reviewed

- which assets replenish it in normal markets

- who approves exceptions

- when not to rebuild aggressively, especially if doing so would lock in panic selling

Without rules, teams tend to delay replenishment in calm markets and discover the problem only when volatility returns.

Private credit and real assets can fit, but only if the liquidity budget is honest

Illiquid assets are not inherently bad. That is the wrong frame.

The real question is whether the liability structure can support them honestly.

Where illiquid assets belong

Private credit, infrastructure, real estate, and other alternatives fit best when:

- capital is genuinely long-term

- liquidity needs are predictable

- investors understand notice periods or lockups

- the portfolio does not rely on those assets to meet short-term cash needs

That is why a liquidity budget is more useful than an allocation target by itself. The key question is not only how much illiquidity you want for income or diversification. It is how much illiquidity the portfolio can afford.

Where they become dangerous

The danger starts when the portfolio promises flexibility the assets cannot support.

That usually happens when:

- clients expect daily access

- withdrawals are uncertain or behaviorally sensitive

- the rest of the portfolio is already expected to fund cash needs

- the illiquid sleeve is sized from return targets rather than liability reality

Vehicle structure matters here. Interval funds, tender-offer funds, drawdown funds, evergreen funds, and direct private holdings all work differently. Gates, side pockets, and suspension tools may exist in some structures, but only under specific governing documents, regulations, and jurisdictions. They are not generic portfolio features.

Governance matters most when markets stop behaving normally

Liquidity planning is not complete until it becomes an operating discipline.

Pre-approved actions beat improvisation

When markets are disorderly, decision time compresses. That is when improvisation does the most damage.

A workable governance checklist should cover:

- sell-order sequencing

- which assets are protected unless conditions worsen

- who approves exceptions

- how often liquidity dashboards are reviewed

- escalation protocols if withdrawals breach thresholds

- structure-specific tools, where legally available, such as gates or side pockets

The details vary by vehicle and jurisdiction. The principle does not: hard decisions get worse when they are made for the first time in the middle of stress.

Communication is part of the risk plan

Silence often makes liquidity pressure worse.

Clients do not need spin. They need clarity on what the portfolio owns, what liquidity is available, what the process is, and what is not changing. Pre-defined communication triggers help. So do pre-written explanations of redemption mechanics, dealing windows, and why certain assets cannot or should not be sold immediately.

Good communication will not eliminate withdrawals. It can reduce withdrawals driven purely by uncertainty.

The right question is not “Is this asset liquid?” but “Liquid for whom, against what demand?”

Liquidity mismatch hides in good times because nobody notices the missing fire exit until the room gets crowded.

That is why this risk belongs in portfolio design, not just crisis response. Map holdings into real liquidity tiers. Model client cash behavior in best, base, and panic cases. Stress markets and withdrawals together. Build a liquidity buffer for function, not yield. And size private assets from a liquidity budget, not a return wish list.

A portfolio is not resilient because it holds quality assets. It is resilient because it can meet real cash demands without being forced to sell the wrong assets at the worst time.

FAQ

What is liquidity mismatch in a portfolio?

Liquidity mismatch happens when a portfolio cannot reliably raise cash fast enough to meet withdrawals or other cash needs. The issue is not just whether assets are tradable, but whether they can be sold in size, on time, and at tolerable cost during stress.

How is liquidity mismatch different from normal market risk?

Market risk is about prices falling. Liquidity mismatch is about needing cash when converting assets into cash becomes harder or more expensive. A portfolio may survive a drawdown if left alone and still fail operationally if withdrawals force sales into a weak market.

How should investors classify portfolio liquidity?

A practical approach is to map holdings into tiers such as T+0 cash, T+1 to T+2 liquid public assets, weekly or monthly dealing vehicles, and gated or locked capital. The useful detail is not just settlement time, but execution reliability, market depth, notice periods, and redemption restrictions.

What is the difference between tradable liquidity and executable liquidity?

Tradable liquidity means an asset can still change hands. Executable liquidity asks whether you can actually raise meaningful cash at a reasonable price under stress. Daily trading does not guarantee tight spreads, deep bids, or stable pricing in a disorderly market.

How do you stress-test a portfolio for withdrawals?

Start with two inputs: the liquidity profile of the assets and the likely cash demands of the clients. Then run scenarios that combine withdrawal pressure with market stress, asking how much cash is needed, over what time frame, which assets would fund it, and what the portfolio would look like after those sales.

What withdrawal scenarios should be modeled?

A simple framework uses three cases: best case for routine cash needs, base case for moderate stress and some redemptions, and panic case for clustered withdrawals during a drawdown. These are planning scenarios, not forecasts.

What is first-sale risk?

First-sale risk is the tendency to meet redemptions by selling the cleanest and most liquid assets first. That can leave behind a weaker residual portfolio with greater exposure to lower-quality, less liquid, or harder-to-value holdings.

What belongs in a liquidity buffer?

The buffer should focus on high-confidence liquidity, not yield maximization. Depending on the portfolio and structure, that may include cash, Treasury bills, government money market funds, or short-duration high-quality government exposure. The right mix depends on withdrawal uncertainty and the rest of the portfolio.

How large should a portfolio liquidity buffer be?

There is no universal percentage that fits every investor or advisory practice. Buffer size depends on client behavior, spending needs, concentration risk, access to outside funding, contribution patterns, and how quickly the rest of the portfolio can realistically be liquidated.

Do private credit and real assets always create dangerous liquidity risk?

No. They can fit well when capital is genuinely long-term, liquidity needs are predictable, and investors understand lockups or periodic redemption terms. They become risky when daily flexibility is expected but the assets cannot support it.

Does ETF liquidity solve underlying market liquidity problems?

Not necessarily. ETF shares may continue trading when the underlying bonds or loans are harder to transact, but that does not make the underlying market liquid. Premiums or discounts can widen, and trading prices may reflect stressed price discovery rather than easy exit conditions.

Why do governance and communication matter in liquidity events?

Liquidity failures are often made worse by improvisation. Pre-approved sell rules, escalation protocols, review thresholds, and communication triggers help teams act faster and reduce avoidable redemption pressure when markets stop behaving normally.