Prediction Markets for Investors: When Polymarket and Kalshi Prices Carry Real Signal — and When They Mostly Reflect Market Plumbing

A prediction-market quote looks clean: 37%, 61%, 84%. It is tempting to treat that number as a distilled truth about the future.

That is the trap.

Prediction markets can be useful for investors. Sometimes very useful. But a tradable quote is not the same thing as a pure forecast. On platforms like Polymarket and Kalshi, prices are shaped not just by views on the underlying event, but also by order-book depth, fees, settlement rules, liquidity incentives, participant mix, and cross-venue trading.

The better question is not, “What is the market predicting?” It is, “How much of this price reflects real information, and how much reflects market structure?” Asked that way, prediction markets become both more useful and less dangerous.

Prediction market prices are useful, but they are not oracles

A binary contract usually settles at $1 if the event happens and $0 if it does not. That makes it natural to read a 63-cent price as roughly a 63% probability. In many cases, that shorthand is reasonable. But it is still shorthand.

Economists have long treated prediction-market prices as useful probability estimates under certain conditions, while also warning that the interpretation depends on assumptions about trader beliefs, risk preferences, and market design. Investors often skip that second part. They jump from “tradable probability” to “best forecast available” without asking what kind of market produced the quote.

A price is not a committee report. It is the level where the most eager buyer and the most willing seller meet, subject to the venue’s rules. In a thin book, one aggressive order can make it look as though the world changed when only the tape changed. And if a contract is tightly linked to another venue, a move may reflect arbitrage rather than fresh information.

The discipline is simple: treat prediction-market probabilities as inputs, not verdicts.

The key distinction: information-rich pricing vs. mechanical pricing

The most useful way to read these markets is to separate information-rich pricing from mechanical pricing.

Information-rich contracts move because traders are updating on the event itself. New polling, a court ruling, a company filing, a policy headline, an official data release — these are real reasons for implied probability to change. In that setting, the market may genuinely compress dispersed information into something investors can use.

Mechanical pricing is different. Here, the contract moves because of thin liquidity, bots leaning on a spread, hedging pressure, cross-venue arbitrage, fee incentives, or one participant pushing through a shallow book. The displayed probability is still tradable, but it may not contain much independent information.

Most real contracts contain both. That is why the oracle framing fails. A market can be directionally informative and still be noisy from minute to minute. It can become more accurate near resolution and still be distorted by settlement timing or order flow. A market can contain wisdom without being wise on every tick.

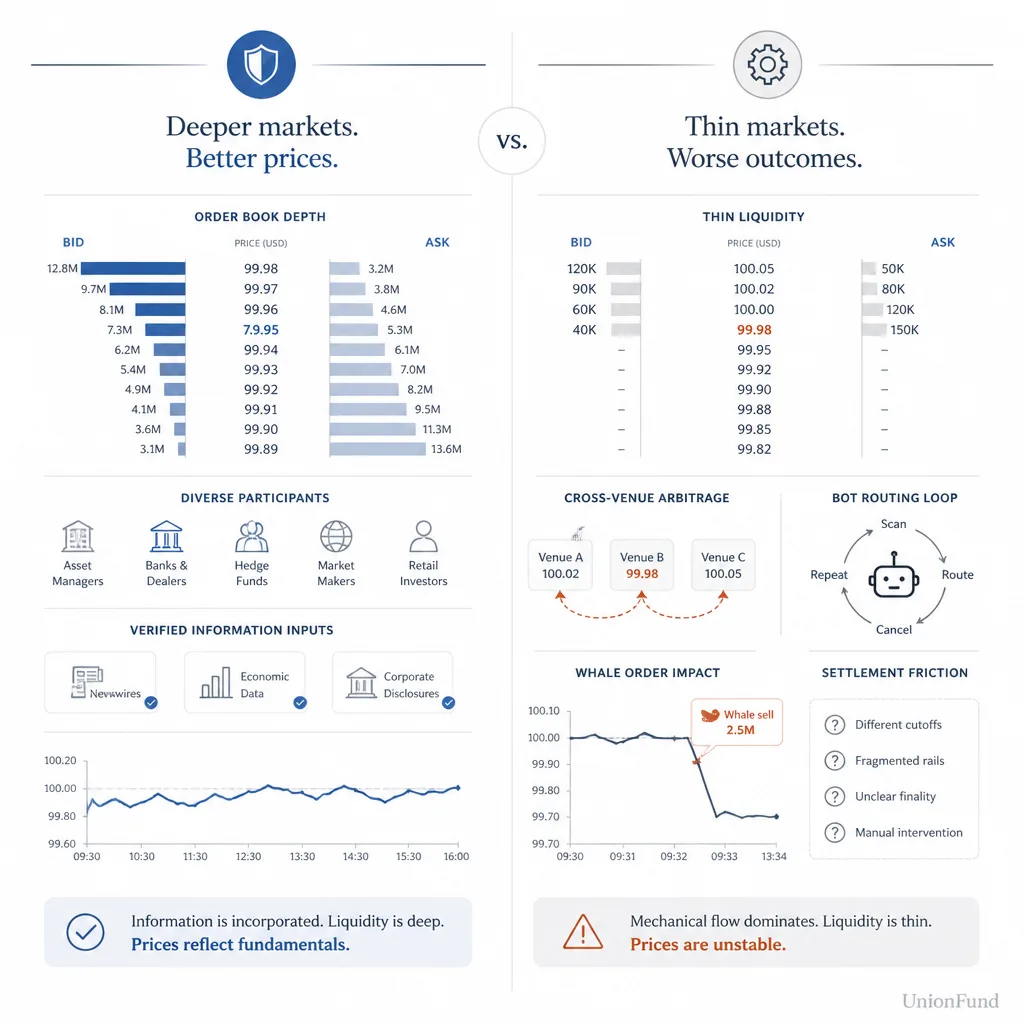

What distorts prediction-market prices in practice

Thin liquidity is the obvious problem. On both venues, prices come from order books, not from some magical consensus engine. If there is little resting size at the best bid or ask, a small order can move the displayed probability a lot.

Cross-venue arbitrage is the less obvious problem. If Kalshi and Polymarket show similar prices, that may reflect shared public information. But it may also mean traders and bots have closed visible gaps between the two. Convergence is context, not proof.

Whale activity matters too. In a thin contract, one large participant can push the tape around for a while without doing anything dramatic or illegal. Sometimes the explanation is simple: one trader is more urgent than the available liquidity. A quote that moved 10 points on modest size should not be read the same way as one that moved 10 points through deep, two-sided flow.

Then there is contract design. Settlement rules matter. Resolution timing matters. Official-source definitions matter. For investors, that means event uncertainty and settlement uncertainty are not always the same thing.

Finally, attention can overwhelm information. A contract that goes viral can attract one-sided retail flow much faster than the underlying facts change. Volume does not always mean insight. Sometimes it just means the market became interesting to watch.

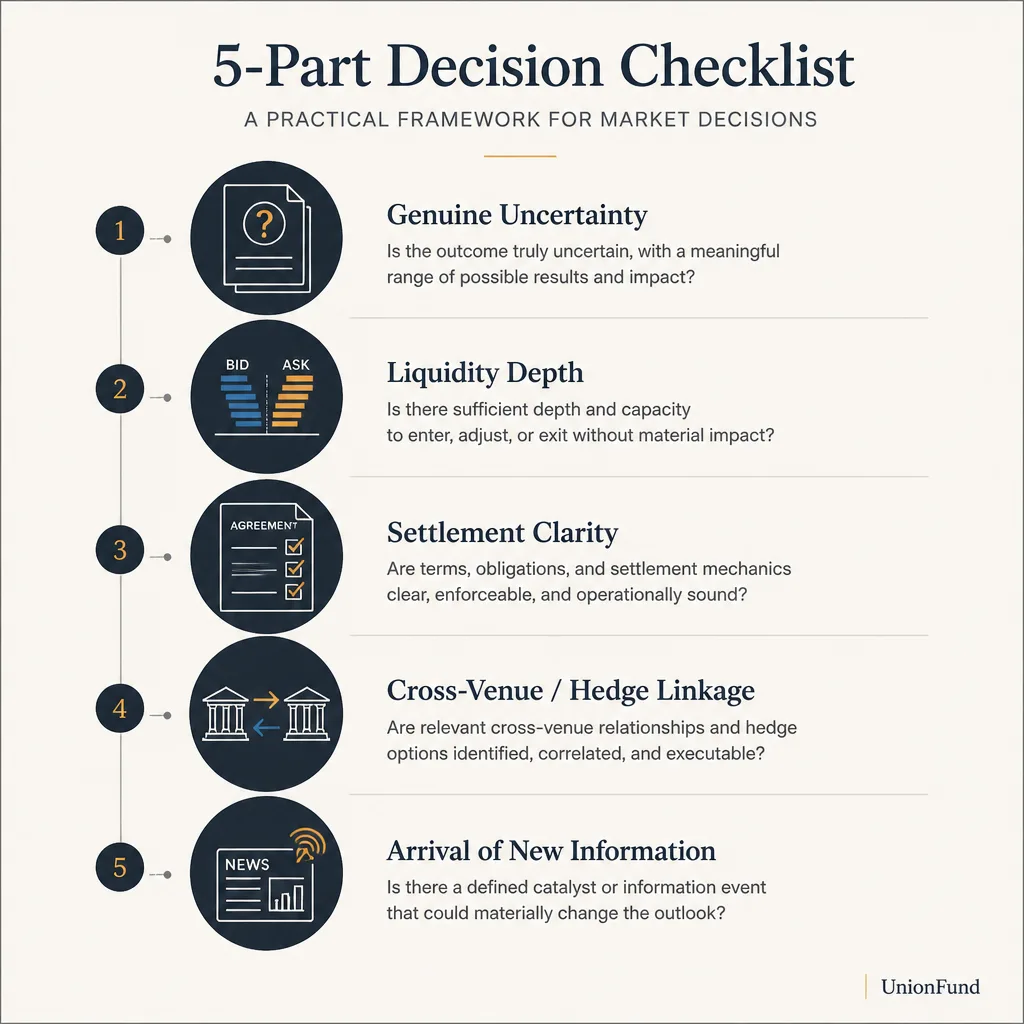

A practical framework for judging whether a contract is signal-rich

The simplest test is to ask five questions.

1. Is there real uncertainty that informed traders can improve on?

Some contracts are mostly waiting rooms for public information everyone will soon see. Others involve interpretation, fragmented evidence, or fast-moving news. The second group is more likely to produce useful discovery.

A contract on a scheduled macro release just before the number drops may offer little room for edge. A contract on a policy decision shaped by legal interpretation, political vote counts, or fragmented reporting may offer much more.

2. Is liquidity deep enough that one order does not dominate the quote?

This is the first practical filter. If a small order can move the market materially, the displayed probability is fragile.

You do not need to become a microstructure specialist. But you should ask a basic question: How much size would it take to move this quote by 2 or 3 points?

3. Are settlement terms clear, objective, and hard to dispute?

If resolution language is ambiguous, the market is not pricing only the event. It is also pricing edge cases, legal wording, and venue-specific interpretation risk. Clear contracts deserve more weight than messy ones.

4. Is the contract tied to other venues or related hedges that can force repricing?

A contract linked closely to another venue, a related multi-outcome market, or a synthetic hedge can trade more like a relative-value instrument than an independent forecast. The price may still be efficient in a narrow sense, but its information content is thinner.

5. Is new information actually arriving?

This sounds obvious, but it is where many readers go wrong. If no meaningful news is hitting the market, price movement is more likely to be flow-driven. If the contract is responding to verifiable headlines, filings, rulings, or data releases, the move deserves more respect.

What signal-rich contracts tend to look like

Signal-rich contracts usually share a few traits.

They have clear resolution criteria. You know what source determines the outcome, when the contract can resolve, and how edge cases are handled.

They attract broad participation. Not “the wisdom of the crowd” in some romantic sense, but enough different participants that one narrative bloc does not dominate the tape.

They have reasonable liquidity relative to their importance. Not perfect depth, but enough that the quote is not hostage to one impatient order.

They update to verifiable news. Elections when credible results arrive. Policy contracts when official agencies release information. Corporate-event markets tied to filings or disclosures.

And they leave less room for one participant to bully the tape. Whales do not disappear, but their flow meets enough opposing liquidity that the resulting move contains more real information.

What arbitrage-dominated contracts tend to look like

Mechanical or arbitrage-heavy contracts have a different feel.

The price often looks pinned to another contract or venue.

Small visible size moves the quote too easily.

Settlement language is confusing or operationally messy, so traders are partly pricing the resolution process rather than the underlying event.

There is often one-sided enthusiasm, especially when social media turns the contract into a narrative object.

And the market contains little independent information beyond its own mechanics. In those cases, the quote may be perfectly real as a tradable level while still being weak as a forecasting input.

How investors should actually use these probabilities

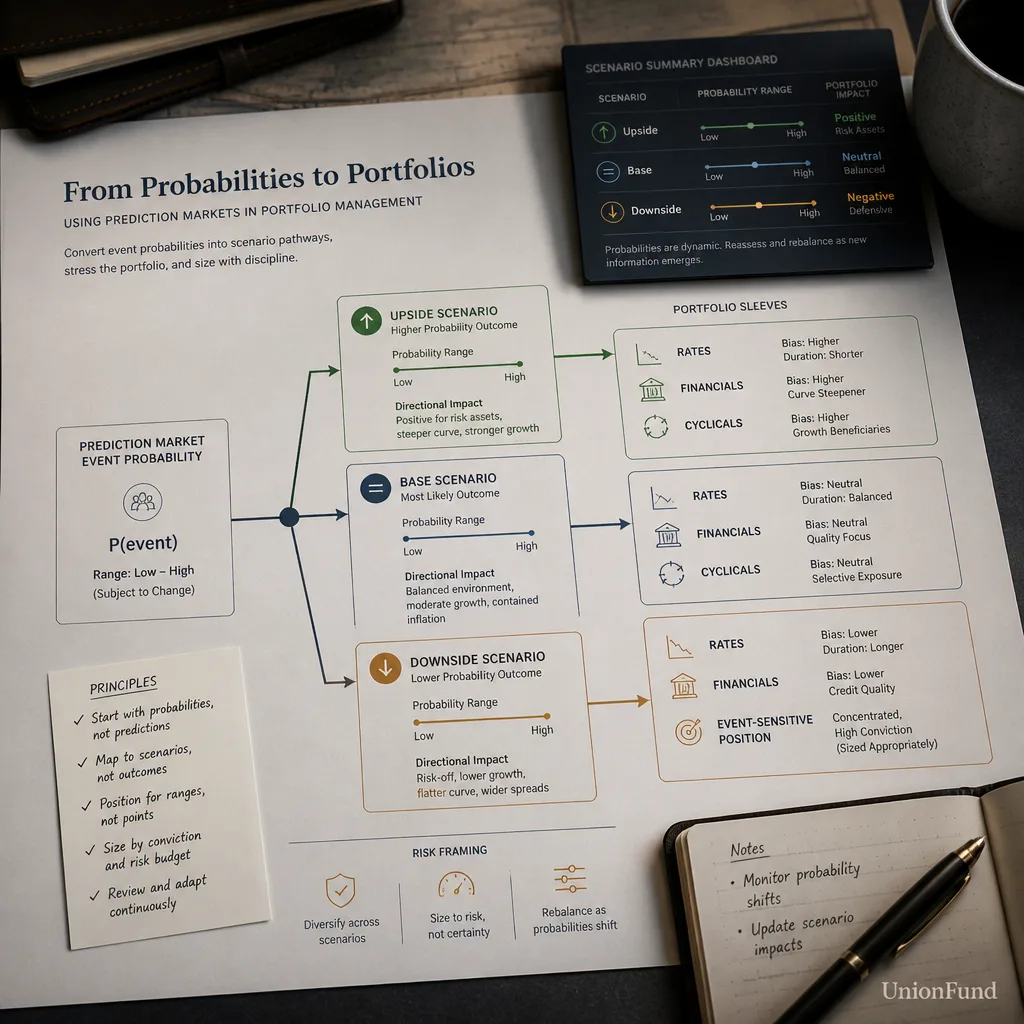

The best use of prediction markets is not signal-chasing. It is scenario framing.

Suppose a policy contract moves from 35% to 50%. The wrong response is to buy or sell every exposed asset automatically. The right response is to ask what changed, whether the move reflects real information, and which holdings are actually sensitive to the event.

That means mapping the event to asset pathways. A policy outcome might affect rates first, then banks, then small caps, then certain cyclicals. An election outcome might matter less for the broad index than for a narrow set of regulated industries. A regulatory-approval contract may be highly relevant to one stock and almost irrelevant to its suppliers.

Prediction-market odds should sit beside other market signals, not above them. Options pricing, rates, credit spreads, analyst revisions, and company-specific exposure often tell you more about magnitude than a binary market does. A prediction market may be directionally right about the event while telling you very little about how large the asset move will be.

That is the discipline that matters: event probability is one input into a broader risk map.

A simple portfolio use case

Imagine you own a basket of stocks with meaningful exposure to a regulatory decision. A prediction market puts approval odds at 40%.

Do not turn 40% into a trade trigger. Turn it into scenarios.

- Base case: approval fails or is delayed; portfolio impact is modestly negative.

- Upside case: approval arrives on time; your most exposed names rerate sharply.

- Downside case: the market is directionally right about higher approval odds, but the economic payoff is smaller than investors expect.

Now assign rough impact ranges rather than false precision. Maybe the upside is +6% to +10% for the exposed sleeve, the downside is -4% to -7%, and the broader portfolio effect is smaller because position sizes are controlled.

Then update only when the probability move appears information-driven. If the contract jumps because official documents changed, that matters. If it jumps because a shallow market got pushed around during a burst of attention, it deserves less weight.

This is slower than treating the quote as an oracle. It is also how investors avoid turning someone else’s binary market into their own portfolio mistake.

The discipline that matters most

Prediction markets are valuable because they force probabilities into the open. Investors need more probabilistic thinking, not less.

But the number on the screen never explains itself. You still have to ask what the market knows, who is trading it, how deep the book is, what the contract actually settles on, and whether the move reflects information or mechanics.

The best use of Polymarket and Kalshi is not blind imitation. It is better risk framing. When the contract is signal-rich, the probability deserves attention. When it is mechanically driven, it deserves skepticism.

Conclusion

Prediction markets can sharpen judgment, but only if you do not outsource judgment to them.

For investors, the useful habit is not “follow the probability.” It is “interrogate the probability.” Ask how much of the quote reflects real information, how much reflects market plumbing, and what would actually change in your portfolio if the event resolves one way or the other.

A binary market is good at forcing a view into a price. It is much less reliable as a substitute for thinking. Used well, that price can improve scenario analysis. Used lazily, it becomes just another way to confuse movement with insight.

FAQ

Are prediction-market prices the same as true probabilities?

No. A prediction-market price is a tradable quote shaped by supply and demand, liquidity, settlement rules, fees, and trader behavior. It can be a useful probability estimate, but only after you account for market structure.

When are Polymarket or Kalshi prices most informative for investors?

They are usually most useful when contracts have clear resolution rules, broad participation, decent liquidity, and frequent updates tied to verifiable news. In those conditions, prices are more likely to reflect real information rather than isolated flow.

What makes a prediction-market contract arbitrage-dominated?

A contract becomes more mechanical when pricing is driven mainly by thin books, cross-venue arbitrage, bots, whale activity, confusing settlement terms, or one-sided narrative trading. In those markets, the quote may say more about market structure than underlying probability.

Should investors trade related assets when a prediction-market probability moves?

Not automatically. A probability move is often more useful as an input for scenario analysis than as a direct trade signal. The first question is whether the move reflects new information, temporary flow, or mechanical repricing.

How should investors use prediction-market odds in portfolio management?

Use them to update base, upside, and downside scenarios for exposed assets or sectors. Their best use is to sharpen risk framing, stress testing, and position sizing — not to replace judgment.

Does agreement between Polymarket and Kalshi confirm that a forecast is reliable?

Not necessarily. Similar odds can reflect shared public information, but they can also result from cross-venue arbitrage, copycat flow, or traders closing visible price gaps. Agreement is useful context, not proof.