AI Investing App Due Diligence: 17 Questions That Reveal What the “AI” Actually Does

Most AI investing apps ask for trust before they earn it.

The pitch is familiar: proprietary models, real-time intelligence, smarter decisions, less emotion. What often goes missing is what investors actually need — a clear explanation of the job the AI performs, evidence that it does that job well, and controls for when it does not.

That matters because “AI-powered” is not a capability. It is a label. An app that summarizes earnings calls is one thing. An app that ranks stocks, sizes positions, or places trades is something else entirely. The more authority the system has over your capital, the more proof it should have to offer.

A polished interface is not an investment process. Due diligence begins when you stop asking whether the app uses AI and start asking what, exactly, the AI is allowed to do.

Start with one question: what job is the AI doing?

Most product pages blur assistance, prediction, and execution. The language is polished enough to sound sophisticated and vague enough to avoid accountability.

So the first step is simple: classify the function before you judge the quality.

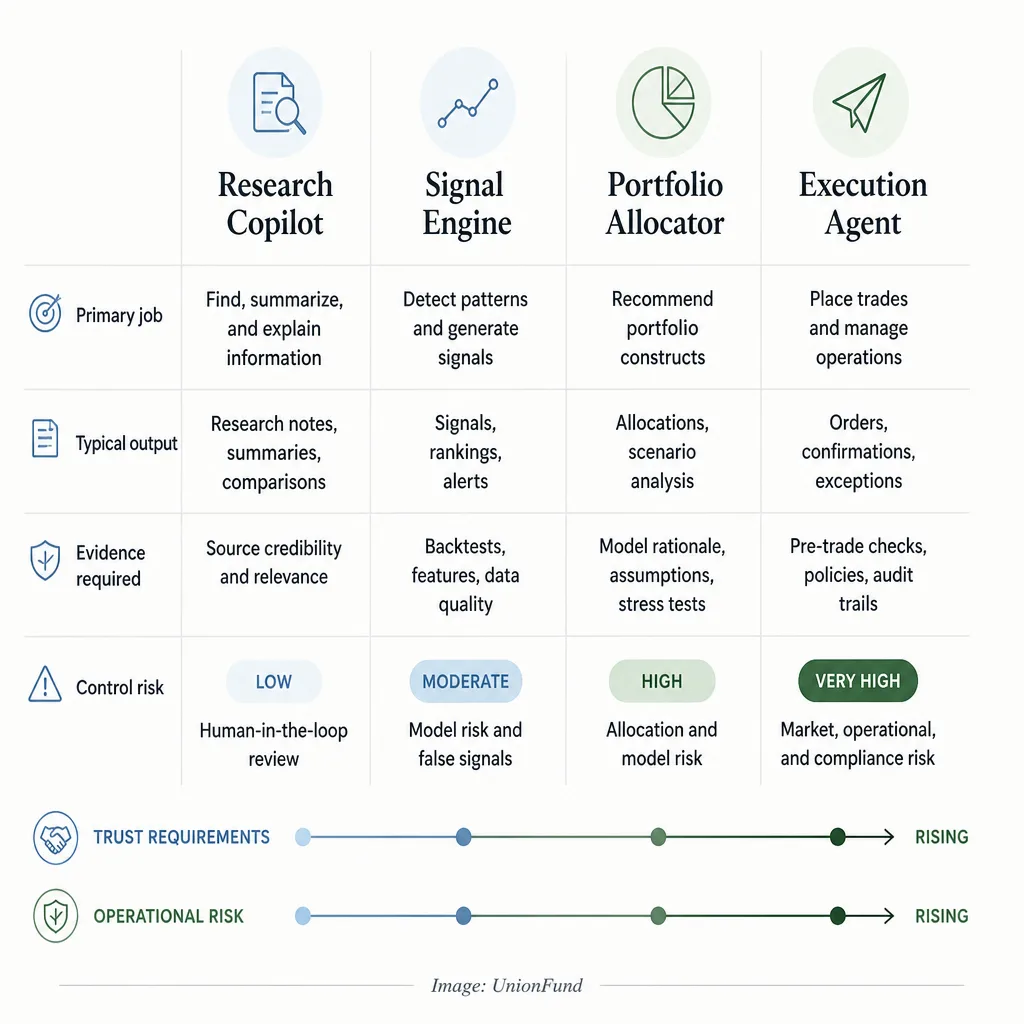

A practical framework looks like this:

- Research copilot: summarizes filings, news, transcripts, screeners, or portfolio data.

- Signal engine: generates rankings, alerts, trade ideas, or forecasts.

- Portfolio allocator: recommends weights, exposures, or rebalancing decisions.

- Execution agent: places trades automatically or with minimal approval.

This is not a formal regulatory framework. It is an investor’s working model. And it matters because the standard of proof changes with the role.

A research assistant can be useful without having any market edge. A signal engine is making an economic claim and needs stronger evidence. An execution agent needs evidence and hard controls, because it can move money, not just your attention.

Investor guidance from the SEC and FINRA has long emphasized that automated tools may ignore important personal circumstances, rely heavily on the inputs they receive, and still leave the investor responsible for the decision to rely on them.[^1][^2] That logic matters even more when “AI” sits on top.

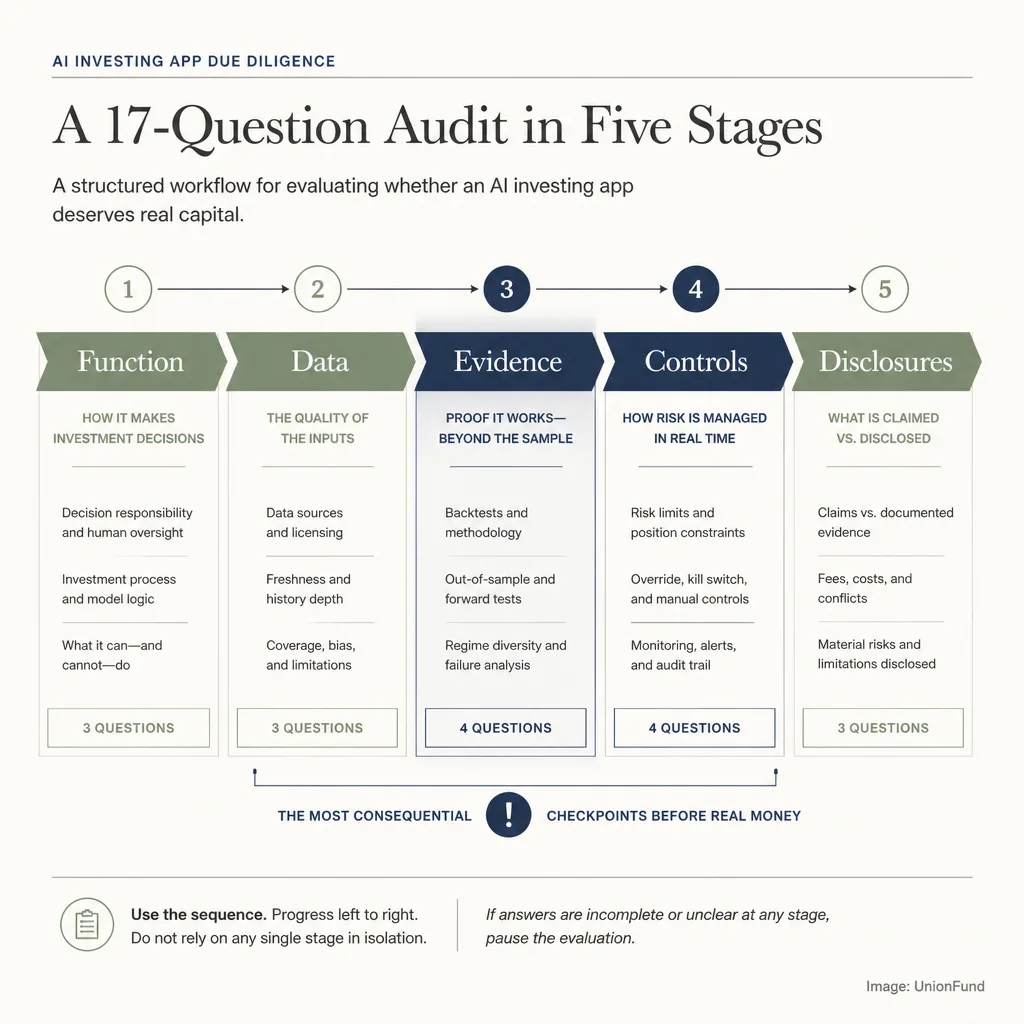

The 17 questions that reveal what the AI actually does

Treat these as an audit sequence, not a checklist. You are trying to understand function, inputs, evidence, controls, and disclosures.

1. What specific decision is the AI responsible for?

Does it summarize, rank, allocate, rebalance, or execute? If the answer is fuzzy, that tells you something already.

2. What data does it use, and where does that data come from?

Price data, fundamentals, filings, news, alternative data, your holdings, and even user behavior can shape the output. SEC robo-adviser guidance specifically tells investors to understand what information a system uses — and what it leaves out.[^1]

3. How current is the data when decisions are made?

A “real-time” claim means little if the inputs are delayed, batch-processed, or stale during volatile markets.

4. Is the model generating original signals or summarizing existing information?

This is one of the most important distinctions in the process. Summarizing public information is a productivity feature. Claiming predictive edge is a performance claim.

5. Does it explain its reasoning in a way that can be audited?

You do not need source code. You do need a comprehensible explanation. “We rank a defined universe weekly using valuation, revisions, and momentum” is meaningful. “Our proprietary AI finds winners” is not.

6. How often is the model updated, retrained, or recalibrated?

A model that never changes can go stale. A model that changes constantly without notice can become impossible to monitor.

7. What market regimes was it trained or tested on?

Bull markets hide a lot of flaws. You want evidence across different conditions: drawdowns, rate shocks, volatility spikes, and flat or choppy periods.

8. Are the backtests net of fees, slippage, spreads, and turnover costs?

This is a non-negotiable question. Hypothetical performance can be made to look much better than reality, and SEC marketing guidance requires fair treatment of risks and limitations, along with supporting information for hypothetical results in many contexts.[^3][^4] If implementation costs are missing, the backtest may be closer to theater than evidence.

9. How was overfitting addressed?

In plain English: how do they know the model did not just memorize historical noise? A serious provider should be able to answer that without hiding behind jargon.

10. What happened in out-of-sample or live performance periods?

A strong backtest is not proof. The harder question is what happened after the strategy left the lab.

11. What risk limits govern position size, concentration, leverage, and drawdown?

A good model without guardrails can still be a bad product.

12. What happens when the model is uncertain, conflicted, or missing data?

Good systems do not just optimize for action. They also know when to do less.

13. Can a human override, pause, or reject recommendations or trades?

FINRA has warned that investors may lose the value of human judgment and oversight when tools do not allow meaningful interaction.[^2] The more automated the app, the more this matters.

14. Does the app execute trades automatically, suggest trades, or rebalance only with approval?

These are not small differences. They define the risk category.

15. How are alerts, monitoring, and incident handling managed?

NIST’s AI risk guidance emphasizes transparency, monitoring, and post-deployment controls, and NIST has also highlighted ongoing monitoring of deployed AI systems as a core practice.[^5][^6][^7]

16. What disclosures describe limitations, conflicts, and model failure cases?

Disclosure quality is evidence. Strong disclosures name boundaries, assumptions, and failure modes. Weak ones mainly reduce liability.

17. Do the product claims match the actual product behavior?

This is the final test. If the homepage implies autonomous intelligence but the app mostly reformats public information through a chatbot, you are not looking at a true investing engine.

A weak answer sounds like this: our proprietary AI identifies winning stocks in real time.

A stronger answer sounds like this: the model ranks a defined universe weekly using stated inputs, signals are reviewed by a human, and trades are never executed without approval.

The second answer is less exciting. It is also far more useful.

How to interpret the answers without getting lost in jargon

The quality of the answer matters at least as much as the answer itself.

Strong answers are specific, bounded, and operational. They tell you what the system does, what it does not do, how often it updates, what types of data it relies on, and where the controls sit.

Evasive answers usually do three things:

- substitute “proprietary” for explanation

- lean on outcomes instead of process

- market certainty while disclosing very little

Transparency matters more than technical complexity. A simpler model with understandable rules, realistic validation, and clear override controls often deserves more trust than a black box wrapped in impressive branding.[^5][^7]

To be fair, some secrecy is reasonable. A firm does not need to hand over its feature engineering or full model recipe. But refusing to answer basic questions about function, data categories, execution authority, monitoring, and limits is not intellectual property protection. It is a red flag.

Three product types, three different standards of proof

Research copilots: usefulness matters more than alpha claims

If the tool mainly summarizes filings, transcripts, or news, the core questions are about accuracy, speed, workflow value, and whether it distorts source material. It does not need to prove market-beating returns to justify a place in your process.

Signal engines: evidence quality and false-positive control matter most

Once a system claims to generate investable signals, the burden rises. Now you need to know whether the signals held up after costs, whether they survived out-of-sample testing, and whether the model was tested across multiple regimes.

Execution agents: controls and governance matter most

An execution system faces the highest bar. Strategy evidence is only the beginning. You also need position caps, concentration limits, drawdown rules, clear account permissions, monitoring, incident response, and a fast way to stop the system if something breaks.[^6][^7]

Red flags investors should take seriously

Some problems show up again and again.

Backtests without implementation costs

If returns are not net of fees, spreads, slippage, and turnover, the headline number may be close to useless.[^3][^4]

Performance claims without regime context

A strategy tested mostly in one favorable environment deserves less confidence than one examined across stress periods.

No clear human control layer

If an app can suggest or place trades but cannot be paused, overridden, or meaningfully supervised, the operational risk is higher than the marketing page suggests.

Disclosure language that sounds legalistic but says little

You should be able to tell what the product does after reading the disclosures. If you cannot, that may be the point.

Marketing that implies autonomy when the product is mostly a chatbot

Many apps sound like portfolio managers and behave like search interfaces. That is not necessarily bad. It becomes a problem when the branding asks for more trust than the product deserves.

There is also a fraud angle here. FINRA has warned about unregistered auto-trading services promoted through websites and apps that claim to be beginner-friendly, low-risk, consistently profitable, or powered by advanced technologies like AI.[^8] FINRA, the SEC, and NASAA have also warned that AI-related claims are increasingly being used in investment fraud.[^9]

If the provider is selling confidence more aggressively than process, slow down.

A simple decision framework before you trust real money

Once you have the answers, translate them into a practical use case.

Use for research only

This makes sense when the tool is mainly a copilot, transparency is limited, or evidence for predictive claims is weak.

Use with small, monitored capital

This may be reasonable when the signal quality appears credible, costs are modeled realistically, and the system has some controls — but not enough to justify larger delegation.

Use only with manual approval

Best when the tool can generate ideas or propose rebalances, but you still want a human to confirm every action.

Avoid until transparency improves

That is the right answer when claims are vague, controls are unclear, performance evidence is mostly hypothetical, or product behavior does not match the marketing.

One more practical step: verify who is behind the product. Investor.gov directs investors to the SEC’s Investment Adviser Public Disclosure database for adviser background checks, and FINRA says BrokerCheck can help research investment professionals, brokerage firms, and investment adviser firms.[^1][^10][^11]

What smart investors are really trying to verify

The real question is not whether the app uses AI.

It is whether its claims, controls, and evidence are proportionate to the trust it asks for.

That is the whole game. An app that helps you organize research can still be useful. An app that wants authority over sizing, timing, or execution needs to earn that authority with specificity, evidence, and restraint.

Investors get into trouble when they mistake polished software for a proven process. The right way to evaluate an AI investing app is to match trust to function, function to evidence, and evidence to controls.

Conclusion

AI investing app due diligence is less about decoding machine-learning jargon and more about refusing to be impressed by vagueness.

If you can identify the job the AI performs, inspect the inputs behind it, pressure-test the evidence, and verify the controls around failure, you will already be ahead of most marketing pages. That does not guarantee you will find a great product. It does make it much harder to hand real money to a system you do not understand.

A useful rule of thumb: the more autonomy the product wants, the less mystery you should accept.

FAQ

What is AI investing app due diligence?

It is the process of verifying what an app’s AI actually does, what data it uses, how it is tested, what risks it creates, and what controls exist before you rely on it with real capital.

How can I tell whether an AI investing app is just a chatbot or a real investing system?

Start by asking what decision the AI is responsible for. A research copilot summarizes information. A signal engine generates investable rankings or alerts. A portfolio allocator recommends weights. An execution agent can place or rebalance trades. The more authority it has over money, the more evidence and control it should provide.

What are the most important questions to ask an AI investing app provider?

The most important questions fall into five areas: function, inputs, evidence, controls, and disclosures. Ask what the AI does, where the data comes from, how current it is, whether backtests are net of fees and slippage, what risk limits exist, whether humans can override decisions, and whether the product claims match the legal disclosures.

Why are backtests not enough when evaluating AI investing apps?

Backtests can be useful, but they are not proof that a strategy works live. They may ignore fees, spreads, slippage, turnover costs, taxes, and changing market conditions. A better question is whether results held up out of sample, in paper trading, or with live capital after realistic costs.

What are common red flags in AI trading or investing apps?

Major red flags include vague claims about proprietary AI, strong performance claims without live evidence, backtests that exclude implementation costs, no clear explanation of model limits, no human override controls, guaranteed-return language, and disclosures that are far less informative than the marketing.

What is the difference between a research copilot and an execution agent?

A research copilot helps you gather, summarize, or organize information, but it does not control trades. An execution agent has authority to place or rebalance trades automatically or with minimal approval. That difference matters because a productivity tool needs usefulness, while an execution system needs evidence, monitoring, risk limits, and emergency controls.

Should investors trust AI investing apps with automatic trading?

Only with much stronger scrutiny. An app that can execute trades should be judged not just on strategy claims, but also on position-sizing rules, drawdown controls, trade limits, incident handling, account permissions, and how quickly a human can pause or override the system.

How do I evaluate the disclosures of an AI investing app?

Good disclosures explain the product’s function, assumptions, limitations, conflicts, costs, failure cases, and whether performance is hypothetical or live. Weak disclosures use broad legal language that reduces liability without helping you understand what the product actually does.

Are all AI investing apps high risk?

No. Risk depends on the job the AI performs. A research assistant used for idea generation is very different from a model that sizes positions or places trades. The right response is not to reject AI outright, but to scale trust to the level of autonomy and capital risk.

How should investors use an AI investing app if transparency is limited?

If transparency is weak, the safest default is to use the tool for research only or avoid it entirely. Limited detail may be acceptable for proprietary model design, but not for basic questions about data categories, update frequency, execution authority, risk controls, and known limitations.