EM ex-China ETFs in 2026: What Risk You Actually Remove—and What Risk You Add Back

EM ex-China ETFs are often presented as a cleaner way to own emerging markets with less China risk. That framing makes sense. China brings a distinct mix of policy, regulatory, governance, and geopolitical uncertainty that many investors would rather not underwrite.[^1]

But “ex-China” is not a simple subtraction. It is a portfolio rewrite. Remove roughly 20% China from a broad emerging-markets benchmark, and that weight gets redistributed elsewhere. In 2026, that usually means meaningfully larger positions in Taiwan, South Korea, and India, along with a bigger tilt toward semiconductor-heavy information technology.[^1][^2]

That is the key point. EM ex-China ETFs can make sense for mandate restrictions, governance preferences, or investors who want to size China separately. What they do not offer is a neutral “safer EM” button. In many cases, they swap one concentration for another.[^1][^2]

Introduction: EM ex-China is a portfolio rewrite, not a simple subtraction

The appeal is simple: cut China-specific risk while keeping the rest of emerging markets.

In practice, the result looks very different. As of May 29, 2026, the MSCI Emerging Markets Index was 20.36% China, 26.41% Taiwan, 23.06% South Korea, and 10.87% India. The MSCI Emerging Markets ex China Index, by contrast, was 33.16% Taiwan, 28.96% South Korea, and 13.65% India.[^1][^2] That is not a small adjustment. It is a different portfolio.

The same pattern shows up in sectors. Information technology was already 43.19% of MSCI EM in late May 2026. Remove China, and IT rises to 51.31%.[^1][^2] So the real question is not whether EM ex-China removes risk. It does. The better question is what replaces it.

What risk are investors actually trying to remove?

Most investors are not trying to remove “risk” in the abstract. They are trying to remove a specific China risk cluster.

China-specific policy and regulatory risk

China’s policy environment can change quickly, and state intervention remains a real consideration for foreign investors. That includes regulatory shifts, sector crackdowns, market-access questions, and the broader role of the state in corporate outcomes.[^1]

Geopolitical and sanctions risk

For some investors, the concern is less about valuation and more about tail risk: tariffs, export controls, sanctions spillover, or portfolio restrictions tied to shifting policy.

Governance, state influence, and market-access concerns

Some investors also want less exposure to ADR- and VIE-related complexity, or they simply prefer markets where governance structures and ownership rules feel more familiar.

Why these are real concerns—but only part of the picture

The mistake is turning those concerns into a broad claim that ex-China is simply “less risky.” A more accurate view is that EM ex-China removes one identifiable bundle of country-specific risks. It does not reduce emerging-markets risk across the board, and it can increase concentration elsewhere.[^1][^2]

What usually replaces China weight in EM ex-China indexes

The reallocation is not spread evenly across the EM universe. Because the index remains market-cap weighted, most of the weight flows to the largest remaining markets.[^1][^2]

Taiwan: the biggest beneficiary

This is the most important shift to understand. In the standard MSCI EM index, Taiwan was already the largest country weight at 26.41% as of May 29, 2026. In the ex-China version, it rose to 33.16%.[^1][^2]

That matters because Taiwan is not just a country bet. In 2026, it is also a semiconductor and AI hardware supply-chain bet. Taiwan Semiconductor Manufacturing alone was 14.46% of MSCI EM and 18.16% of MSCI EM ex China.[^1][^2]

India: larger weight, different profile

India also rises, from 10.87% in MSCI EM to 13.65% in MSCI EM ex China.[^1][^2] That changes the character of the portfolio. India brings more domestic-growth exposure and often more valuation sensitivity than the ex-China label suggests.

This is one of the quieter tradeoffs in 2026: investors moving away from China are often moving toward a market with a different earnings structure and a richer valuation backdrop. MSCI’s data showed higher trailing P/E and price-to-book for EM ex China than for broad EM on the same date.[^2][^3]

South Korea and other large markets

South Korea also absorbs a major share of the removed China weight, rising from 23.06% in MSCI EM to 28.96% in the ex-China index.[^1][^2] Brazil, South Africa, and other markets gain incrementally, but not enough to change the overall picture.

Why the replacement is not evenly spread

This is a simple mechanics point. MSCI’s standard EM and EM ex China indexes are built to capture roughly 85% of free-float-adjusted market capitalization in their eligible markets.[^2][^3] Once China is excluded, the rest of the index is reweighted by relative market cap. The result is not broader diversification by design. It is a heavier allocation to the biggest surviving markets.

How sector and factor exposure change when China comes out

Country weights tell only part of the story. Sector structure changes just as much.

Less China internet exposure, more semiconductor and hardware exposure

In MSCI EM, China contributes meaningful exposure to consumer internet, communication services, and parts of consumer discretionary. Once China is removed, that mix shifts. In MSCI EM ex China, consumer discretionary fell to 4.23% and communication services to 3.00%, while information technology rose to 51.31%.[^1][^2]

Why information technology rises

The answer is mostly composition. Bigger Taiwan and South Korea weights mean more exposure to semiconductors, memory, foundries, components, and hardware exporters. In 2026, that also means greater sensitivity to the AI infrastructure cycle.[^1][^2]

Why other exposures shift too

India’s larger role can add domestic banks, financials, and consumer-linked growth exposure. Brazil, Saudi Arabia, and South Africa can add smaller commodity, financial, and cyclical tilts depending on the index date and fund implementation.[^2][^4]

Factor implications: growth, momentum, quality, cyclicality, and valuation

Some of this is interpretation rather than hard rule, but it is still useful. Removing China often reduces exposure to Chinese platform and property-related complexity while increasing exposure to semiconductor-led growth, momentum, and quality characteristics. It can also increase cyclicality tied to hardware demand and export sensitivity. And it may raise valuation exposure: as of May 29, 2026, MSCI EM ex China had a trailing P/E of 20.51 and price-to-book of 3.21 versus 18.60 and 2.57 for MSCI EM.[^2][^3]

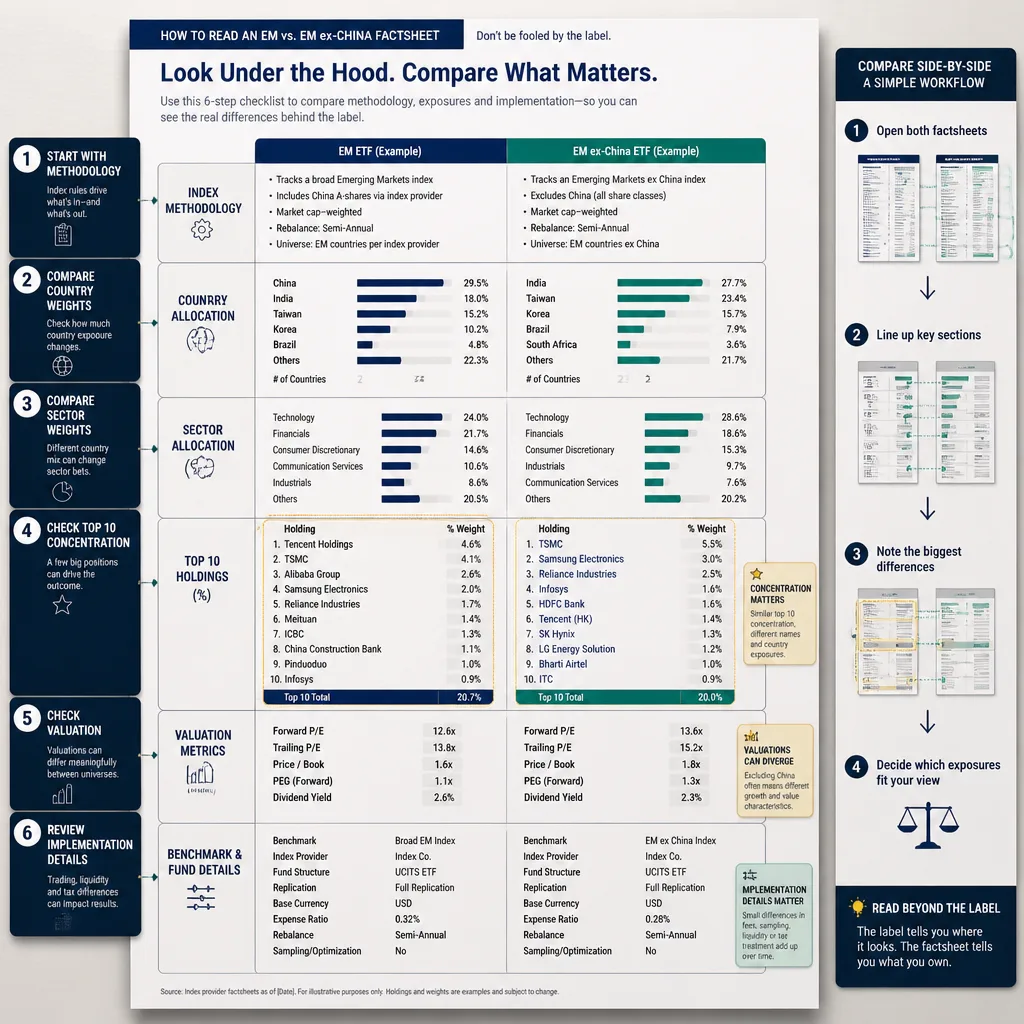

How to read an EM vs. EM ex-China factsheet without fooling yourself

This is where investors can improve their process quickly.

Start with index methodology, not the label

First, check which index family the ETF tracks. “EM ex-China” is not one universal portfolio. Providers can use different index rules, rebalance schedules, and security universes.

Compare country weights side by side

Do this before anything else. If you remove China, where did the weight go? In late May 2026, the MSCI answer was mostly Taiwan, South Korea, and India.[^1][^2]

Then compare sector weights

This tells you whether you are still buying broad EM or something closer to a technology-heavy regional expression. In MSCI’s case, the jump from 43.19% IT in EM to 51.31% in EM ex China is too large to ignore.[^1][^2]

Check top-10 holdings concentration

This is where the diversification story often weakens. In the MSCI EM ex China index, the top 10 constituents represented 44.46% of the benchmark as of May 29, 2026.[^2] If your goal is to reduce single-name concentration, that matters.

Look at valuation, earnings, and liquidity differences

Do not stop at geography. Compare trailing and forward valuation metrics, dividend yield, and, if possible, earnings mix. EM ex China is not just a country exclusion. It can also be a style and valuation shift.[^2][^3]

Watch benchmark-family and fund-implementation differences

Even when an ETF tracks the same benchmark family, the fund factsheet can differ from the index snapshot because of timing, cash, sampling, and implementation. For example, BlackRock’s EMXC fact sheet dated March 31, 2026 showed country exposure of 30.02% Taiwan, 20.72% South Korea, and 16.77% India.[^4] Those figures differ from the May 29, 2026 MSCI snapshot for normal reasons, which is exactly why investors should read both documents instead of relying on the label alone.[^2][^4]

The hidden tradeoff: removing one headline risk can create a new concentrated bet

This is the part many investors underestimate.

Taiwan concentration and semiconductor cycle risk

If one-third of the ex-China benchmark is Taiwan, and a large share of the top holdings is tied to the chip supply chain, you are not holding a neutral EM basket. You are expressing a fairly concentrated view on semiconductor leadership, export demand, and the durability of the AI hardware buildout.[^1][^2]

India concentration and valuation risk

India may be an attractive long-term market. That can be true. But paying up for growth is still a risk. If your reason for switching is “I want less uncertainty,” replacing China with a larger India weight may reduce one kind of uncertainty while increasing another.

Correlation risk

This is the subtler issue. You may lower direct China policy risk while increasing dependence on a single global theme: semiconductors and AI-linked capex. That is still concentration. It just looks cleaner because it is spread across Taiwan and South Korea instead of sitting inside China.

Why this matters more in 2026

It matters more now because EM leadership has become unusually tied to large Asian technology names. In the broad MSCI EM index, the top three constituents as of May 29, 2026 were TSMC, Samsung Electronics, and SK Hynix.[^1] Ex-China can amplify that reality rather than diversify away from it.[^2]

A practical decision framework for investors

A useful way to think about EM ex-China is to start with your actual objective.

Question 1: Is your goal exclusion, diversification, or active outperformance?

If the goal is mandate compliance or a hard China exclusion, the case is straightforward. If the goal is better diversification, test that empirically through weights and holdings. If the goal is outperformance, be honest that you are making an active regional and sector bet.

Question 2: Are you comfortable with larger Taiwan and India weights?

Not in theory. In actual percentage terms. If one-third Taiwan and mid-teens India feels too concentrated, the ex-China solution may not match your intent.[^2][^4]

Question 3: Do you want less China, or do you want a barbell of ex-China plus standalone China?

For many investors, this is the cleaner structure. Use EM ex-China as the non-China sleeve, then decide separately how much China to own. That gives you benchmark control without forcing an all-or-nothing decision.

Question 4: Are you solving for politics, volatility, valuation, or benchmark governance?

These are different problems. If you are solving for politics or governance, ex-China may help. If you are solving for lower volatility, do not assume it will. MSCI’s own risk data showed higher 5-year and 10-year annualized standard deviation for EM ex China than for the broad EM index as of May 29, 2026.[^2][^3]

Decision checklist: when EM ex-China makes sense—and when it doesn’t

EM ex-China is usually a good fit when:

- you need a formal no-China benchmark for policy or mandate reasons

- you want to size China separately from the rest of EM

- you have a deliberate positive view on Taiwan, South Korea, and India

- you understand that you are accepting more technology and semiconductor concentration

It is a weaker fit when:

- your goal is vaguely defined as “less risk”

- you assume country exclusion automatically means better diversification

- you have not checked top holdings, sector weights, or valuation changes

- you would be uncomfortable discovering that the portfolio is heavily tied to one semiconductor cycle

The biggest red flag is conceptual. If an investor says EM ex-China is “basically EM, but safer,” they probably have not defined what kind of risk they are trying to remove.

Conclusion

EM ex-China ETFs are best understood as an active structural tilt, not a neutral cleanup trade.

Yes, they remove a real set of China-specific risks. For some investors, that is exactly the point. But the replacement matters just as much. In 2026, removing China often means larger Taiwan, South Korea, and India weights, higher information-technology exposure, more sensitivity to semiconductors and AI hardware, and, in some cases, a richer valuation profile.[^1][^2][^3]

Before making the switch, do one simple exercise: write down the specific risk you want out of the portfolio, then identify the exact countries, sectors, and top holdings that take its place. If you still like the answer, EM ex-China may be the right tool. If not, you may be solving the wrong problem with the right-sounding label.

FAQ

Are EM ex-China ETFs safer than standard EM ETFs?

Not automatically. EM ex-China ETFs remove China-specific regulatory, governance, and geopolitical risks, but they often replace that exposure with heavier weights in Taiwan, South Korea, and India, plus more semiconductor-heavy information technology.[^1][^2] Whether that is “safer” depends on which risk you are trying to reduce.

What risk does an EM ex-China ETF actually remove?

It mainly removes China-specific risk clusters: state intervention, regulatory unpredictability, market-access concerns, ADR/VIE-related complexity where relevant, and some sanctions or tariff-related uncertainty. It does not remove emerging-markets risk broadly.

What usually replaces China weight in EM ex-China ETFs?

In many 2026 EM ex-China indexes, the weight removed from China is reallocated mostly to Taiwan, South Korea, and India rather than spread evenly across the emerging-markets universe.[^1][^2] That means country concentration often rises rather than disappears.

Why do Taiwan and India matter so much in EM ex-China ETFs?

Because they are often the biggest beneficiaries of China’s removal. Taiwan can materially increase semiconductor and hardware concentration, while India can raise domestic-growth exposure and valuation sensitivity.[^1][^2][^3] Those are different risks, not neutral replacements.

Why does EM ex-China often have more technology exposure?

Removing China tends to reduce platform internet, communication services, and some consumer discretionary exposure tied to Chinese mega-caps. At the same time, higher Taiwan and South Korea weights can increase exposure to semiconductors, hardware, and broader information technology.[^1][^2]

How should investors compare EM and EM ex-China ETFs?

Start with the index methodology, then compare country weights, sector weights, top-10 holdings concentration, and valuation metrics. After that, check the ETF factsheet for implementation differences such as rebalance dates, sampling, and portfolio construction.[^2][^4]

Does EM ex-China reduce volatility?

Do not assume so. Excluding China may reduce one kind of geopolitical or policy risk, but the resulting portfolio can become more concentrated in semiconductor cycles, export sensitivity, or expensive domestic-growth markets. MSCI’s data also showed higher historical annualized standard deviation for EM ex China than for broad EM at the May 29, 2026 snapshot.[^2][^3]

Is EM ex-China a strategic allocation or a tactical trade?

It can be either, but the distinction matters. For some investors, it is a strategic benchmark choice driven by mandate, governance, or geopolitical constraints. For others, it is a tactical view on China. Those are different decisions and should not be treated as the same thing.

When does an EM ex-China ETF make the most sense?

It makes the most sense when an investor has a clear reason to exclude China, such as policy restrictions, governance concerns, benchmark control, or a deliberate preference for separate country sleeves. It is a weaker fit when the goal is vaguely defined as wanting “less risk.”

Should investors use EM ex-China plus a separate China allocation?

Often, yes. For investors who want more control, that can be the cleaner approach. It lets you choose how much China exposure to hold instead of accepting the default China weight in a broad EM index or removing it entirely without thinking through the replacement.