From Chat to Trade to Autonomous Execution: The Hidden Risks Retail Investors Inherit

The path into AI trading usually feels harmless. A chatbot summarizes earnings. Then it screens setups. Then it drafts an entry, a stop, and a target. One API key later, it can place the order too.

That last step looks small. It isn’t.

The real shift is not from human research to AI research. It is from advice to authority. Once a system can place, modify, cancel, or manage live orders, you are no longer judging whether the model has useful ideas. You are handing part of your portfolio’s behavior to a live operational stack that can fail in more ways than most retail investors expect.

That is the hidden inheritance of autonomous execution. You do not just gain speed. You inherit control problems that institutions spend heavily to manage.

The shift is from advice to authority

Why chat-based research tools feel low-risk at first

Most AI tools used by retail investors still sit on the research side of the workflow. They summarize filings, compare valuation metrics, rank watchlist names, or turn a rough thesis into a cleaner trade plan.

That feels manageable because the investor still makes the final call. The model can be wrong, but it cannot move capital on its own.

That distinction matters. A flawed research assistant can waste time or distort judgment. A flawed execution agent can place orders, resize exposure, or fail to exit when conditions change.

What changes once a system can place, modify, or cancel orders

The moment automation touches live brokerage execution, the problem expands beyond signal quality.

An order does not go straight from model output to the market. Retail orders move through brokers, routing venues, order types, and execution rules, and that path can affect both timing and price.[^1] Investor.gov is explicit on this point: online investors do not trade directly with the market, and execution is not instantaneous.[^1]

So even a reasonable idea can become a bad trade because of order choice, routing, slippage, latency, liquidity, or a failure in the code between the model and the broker.[^1][^2]

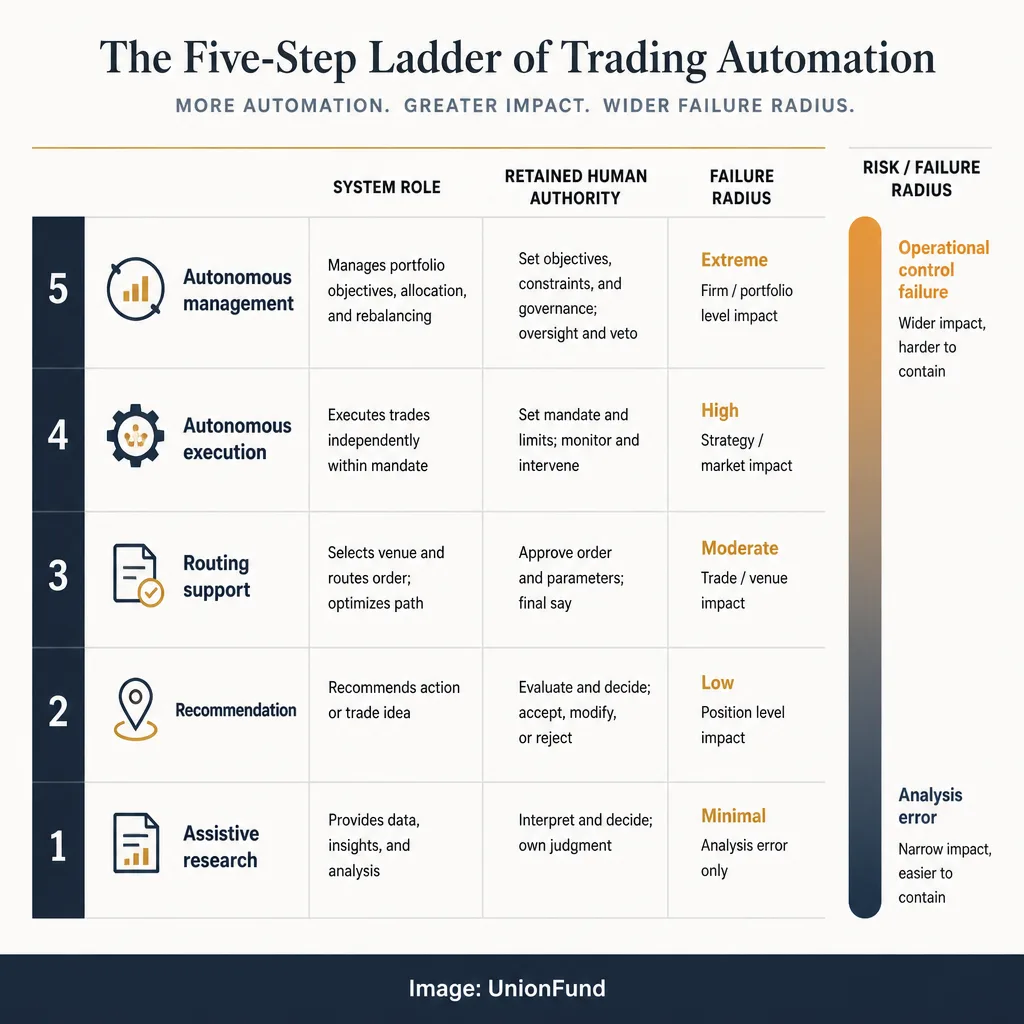

A simple ladder of automation

A useful way to think about AI trading is as a ladder:

| Workflow level | What the system does | Investor authority retained | Main risk |

|---|---|---|---|

| Assistive research | Summarizes, screens, explains | High | Bad analysis |

| Recommendation | Suggests entries, exits, sizing | High | Overreliance |

| Routing support | Prepares tickets or staged orders | Medium-high | Input errors |

| Autonomous execution | Places, cancels, or modifies orders | Medium-low | Control failure |

| Autonomous management | Rebalances, sizes, exits, reallocates | Low | Cascading loss |

The danger is that each step feels like a convenience upgrade. In reality, the jump from recommendation to execution is a transfer of authority.

When execution becomes autonomous, the main risk shifts to operational control

Good signals can still produce bad outcomes

A retail investor can be directionally right and still lose more than expected.

Take a simple example: an AI system decides to exit a falling position with a stop order. In calm conditions, that may look sensible. In a fast market, a stop order becomes a market order when triggered, and the execution price can differ sharply from the stop price.[^2] FINRA has warned about the same issue in volatile conditions.[^3]

So the signal may be right in theory. The live outcome can still be poor because the execution layer behaves differently than the investor imagined.

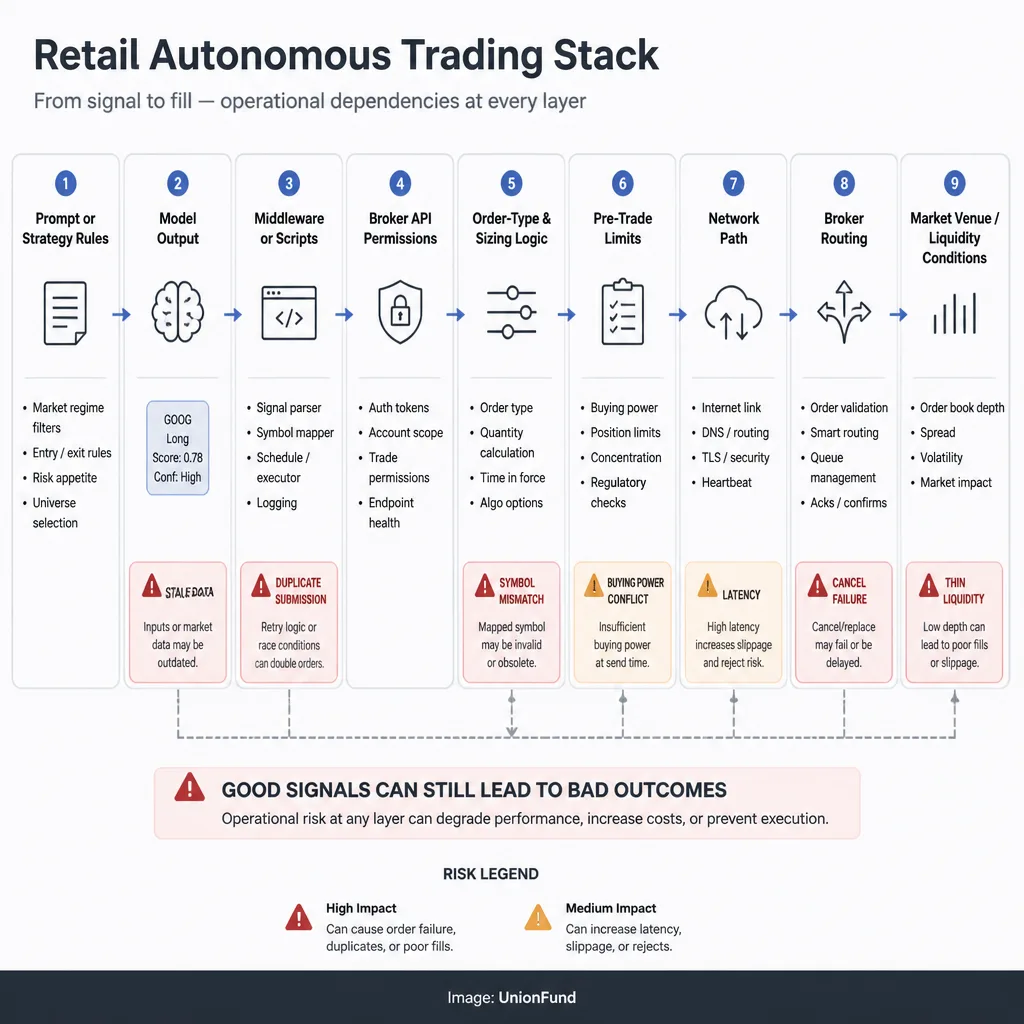

The hidden system stack

Retail investors often picture AI trading as one model making one decision. Live execution is messier.

The real stack includes:

- prompts or strategy rules

- model output formatting

- middleware or scripts

- broker API permissions

- order-type logic

- buying-power and margin checks

- network reliability

- broker routing and market venue behavior

- exchange or liquidity conditions

Every layer can introduce failure. Duplicate submissions, stale prompts, mismatched symbols, broken cancel requests, or sizing logic that rounds up instead of down are not exotic risks. They are the kind that cause real damage.

Why retail investors inherit institutional-style control problems without institutional safeguards

The SEC’s market access rule exists because automated order flow can create risks from erroneous orders, breaches of preset credit or capital thresholds, and regulatory failures when controls are weak.[^4][^5] Institutions build pre-trade risk checks, supervisory procedures, testing protocols, and post-incident reviews around that reality.

Retail traders can now access parts of the same technology stack without anything close to the same control environment.

That asymmetry is the core problem. Automation has become easy to access faster than governance has become easy to maintain.

Five risks that become much more dangerous once AI can trade

Kill-switch failure

A kill switch is not a fancy feature. It is the line between a contained error and a self-amplifying one.

If a bot misreads data, starts duplicating orders, or keeps buying into a feed failure, the key question is simple: what stops it? SEC guidance around market access risk specifically discusses controls to prevent erroneous, oversized, or duplicative orders.[^4]

The important design principle is independence. If the model decides when to stop itself, the safeguard depends on the same layer that may be failing. A credible kill switch should sit outside the model’s judgment path, ideally through broker-side limits, middleware rules, API revocation, or account-level restrictions.

Incident response lag

Manual traders are slow, but that slowness sometimes limits damage. Automated systems reverse that tradeoff.

In a fast market, a human may not even notice abnormal behavior before several orders have been placed, rejected, resubmitted, or partially filled. The SEC adopted Rule 15c3-5 in part because automated flow can create meaningful risk before human intervention is possible.[^5]

That is why “I’ll monitor it and step in if needed” is weaker than it sounds. Monitoring without predefined shutdown logic is often just delayed regret.

Strategy drift

Strategy drift is not only about markets changing.

It can come from prompt edits, model updates, data-source changes, broker-side rule changes, altered position-sizing assumptions, or the investor quietly loosening constraints after a good run. FINRA’s guidance to firms on algorithmic trading emphasizes testing, validation, implementation controls, and review after changes for exactly this reason.[^6]

A retail version of drift might look mundane: the bot began as a swing-trading assistant in liquid large caps, then gradually starts trading smaller names premarket, with looser stops and larger position sizes because the operator kept widening the rules.

Nothing broke. The system just stopped being the strategy the investor thought they had deployed.

Unintended leverage and position concentration

Margin turns bad automation into a force multiplier.

Investor.gov warns that with a margin account, investors can lose more than the amount deposited, may have to deposit more cash on short notice, and can have securities sold by the broker without consultation if account equity falls too far.[^7] That is standard margin risk. Automation makes it more dangerous because sizing, re-entry, and portfolio reallocation can happen faster than the investor can process.

A common retail failure mode is leverage creep. The investor thinks they automated execution efficiency. In practice, the system keeps adding exposure because buying power is available, a sizing formula keys off stale volatility, or multiple signals stack into one symbol or one factor bet.

Gap risk in fast markets

Gap risk is where many “it should have stopped out” assumptions fail.

Investor.gov notes that stop orders can execute at prices far from the intended stop in rapidly moving markets.[^2] FINRA also warns that volatile conditions, halts, or delayed openings can interfere with how stop-based exits behave.[^3]

Many automated strategies quietly assume continuity: that there will be a tradable path from here to there. In stressed markets, that path may not exist. If your automation plan relies on orderly exits exactly when orderliness disappears, it is not much of a plan.

Why automation changes the shape of loss, not just the speed of trading

Manual trading contains friction; automation removes it

Manual workflows have accidental safeguards: hesitation, order-entry delay, second looks, and simple fatigue.

Those frictions are annoying when markets are calm. They become protective when something is off.

Automation removes them. That is its strength and its hazard.

Small errors compound when execution loops are fast

A manual mistake is often one trade. An automated mistake can become a loop.

One stale input can trigger repeated entries. One broken cancel function can leave multiple live orders. One sizing bug can overshoot exposure across several positions before the dashboard even refreshes.

The operational question is not whether the system can make a bad trade. Of course it can. The real question is how large the error can become before anyone interrupts it.

The worst losses often come from control failures, not bad forecasts

Bad forecasts are part of investing. Control failures are different. They create losses that were never part of the thesis in the first place.

That is why autonomous execution should be treated less like a smarter alert system and more like a delegated risk manager. If it has authority over capital, the quality of its controls matters as much as the quality of its ideas.

Minimum controls retail investors should have before allowing autonomous execution

Before a system can place live trades, a few controls should be non-negotiable.

Hard limits

Set hard rules outside the model where possible:

- maximum order size per trade

- maximum position size per symbol

- maximum sector or factor concentration

- maximum daily realized and unrealized loss

- maximum gross exposure

- maximum leverage or margin usage

- time-of-day restrictions, especially around the open, close, and illiquid sessions

The SEC’s market access framework is built around preset thresholds for financial exposure and controls against erroneous orders.[^4][^5] Retail investors should think the same way, even on a smaller scale.

Kill switches independent of the model

At minimum, you need a way to halt trading that does not require the model to agree.

That can mean:

- revoking API keys

- disabling the order engine

- broker-side trading restrictions

- middleware flags that reject all new orders

- automatic shutdown after abnormal order count or loss thresholds

Human review thresholds

Not every order needs manual approval. Unusual ones often do.

Examples include:

- the first trade in a new asset class

- use of margin beyond a set threshold

- orders outside normal position size

- premarket or after-hours execution

- exits that convert to marketable orders in thin liquidity

- regime changes such as halt-heavy or gap-heavy sessions

Logging, alerts, and audit trails

If something goes wrong, you need to know what happened and in what order.

That means logs for:

- prompts or strategy inputs

- model outputs

- order requests

- broker responses

- fills, rejects, and cancels

- account balances, buying power, and open positions

Without an audit trail, you are guessing. Guessing is how the second mistake gets made.

Paper trading, sandboxing, and staged rollout

Alpaca’s disclosures are blunt: automated systems require monitoring because of connectivity failures, power losses, computer crashes, and programming discrepancies, and it is generally wise to start with small size or paper trading while refining the process.[^8][^9]

Paper trading is not just for beginners. It is how you test the machinery. A sensible rollout looks like this:

- backtest the idea

- paper trade the workflow

- deploy with micro-size live capital

- restrict symbols and sessions

- scale only after stable behavior is proven

What incident response should look like in a retail trading setup

Define a trading incident before one happens

If you wait until something breaks to decide what counts as an incident, you are already behind.

Define incidents in advance. For example:

- unexpected order duplication

- position size outside allowed bounds

- a spike in margin usage

- failed cancel/replace behavior

- a mismatch between expected and actual positions

- repeated rejects from the broker

- unrecognized trading during restricted hours

Make shutdown authority explicit

Someone must have clear shutdown authority. In a solo retail setup, that someone is usually you, but the shutdown path still needs to be operationally clear.

Know the order:

- stop new orders

- cancel resting orders if appropriate

- verify open positions

- confirm broker-side account state

- reconcile fills and exposure

Review the whole chain after a failure

Post-incident review should answer five questions:

- What did the system think it was doing?

- What orders were actually sent?

- How did the broker respond?

- What positions and exposures resulted?

- What market conditions existed at the time?

That is how you separate a bad strategy from a broken workflow.

Why restarting without diagnosis is often the second mistake

A bot that misbehaved once may do so again for the same reason.

Restarting before a root-cause review often turns a contained incident into a pattern. FINRA’s emphasis on testing and post-change review exists because operational problems rarely disappear just because the market has moved on.[^6]

A practical rule: automate what you can supervise, not what you merely trust

Where AI is usually most useful for retail investors

For most self-directed investors, AI is strongest when it improves analysis without taking custody of action.

Good use cases include:

- summarizing earnings and filings

- screening for setups

- monitoring watchlists

- comparing scenarios

- drafting orders for human review

- surfacing portfolio risk concentrations

That is where AI can reduce friction without removing accountability.

Where full autonomy is hardest to justify

Full autonomy is hardest to justify when:

- the account uses margin

- liquidity is inconsistent

- the strategy depends on stops behaving precisely

- the investor cannot monitor the system reliably

- there is no robust logging or kill switch

- one bug could create outsized concentration quickly

For many retail investors, the right answer is not “never automate.” It is “stop one layer earlier than your confidence suggests.”

A decision framework for choosing the right workflow

| Workflow | Best use case | Supervision burden | Failure radius |

|---|---|---|---|

| Assistive | Research, screening, planning | Low | Low |

| Semi-automated | Prebuilt tickets, alerts, rule-based execution with approval | Medium | Moderate |

| Autonomous | Live order placement and management without approval | High | High |

A simple test helps: if you cannot explain how the system will stop, how it will be audited, and how you will respond when it misbehaves, it should not have execution authority.

Conclusion

The seductive story about AI trading is that the smarter model wins. That is only half true.

Once a system can execute, the decisive question is no longer whether it can find good trades. It is whether you can control what happens when the workflow meets real markets, real brokerage plumbing, and real stress. That is where retail investors inherit risks that look less like research errors and more like governance failures.

Automation can be useful. Sometimes very useful. But the line that matters is simple: advice can be ignored; authority has to be supervised.

FAQ

What is the difference between AI-assisted trading and autonomous execution?

AI-assisted trading helps with research, screening, summaries, or trade ideas while the investor still decides whether and how to place the order. Autonomous execution begins when the system can place, modify, cancel, size, or manage live orders on its own. That is the point where the problem shifts from idea quality to operational control.

Why does risk increase when AI can execute trades directly?

Because the investor is no longer only evaluating whether the model has a good view. They are also relying on a live system that includes prompts, code, APIs, brokerage permissions, order logic, position sizing, and market execution. A decent signal can still produce a bad outcome if the workflow breaks under real conditions.[^1][^4]

What are the main hidden risks of autonomous trading for retail investors?

The biggest risks include kill-switch failure, slow incident response, strategy drift, unintended leverage, concentrated exposure, duplicate or erroneous orders, and larger losses during fast or illiquid markets. The common thread is that automation can scale small mistakes before a human has time to intervene.[^4][^5]

What is a kill switch in automated trading?

A kill switch is a control that can immediately halt trading activity when predefined conditions are breached. In a retail setup, that may mean disabling API access, stopping the order engine, or triggering hard limits on daily loss, position size, or exposure. The key point is that it should sit outside the model’s own judgment layer.

Why should a kill switch be independent of the AI model?

If the same system that is failing is also responsible for deciding when to stop, the safeguard may fail with it. Independent controls reduce that circular dependency. Hard stops at the broker, middleware, or account-rule layer are usually more credible than asking the model to police itself.[^4]

How does automation increase leverage risk?

Automation can increase leverage risk through aggressive sizing logic, repeated entries, faster reallocation, or unnoticed interaction with margin-enabled accounts. A retail investor may think they are improving execution efficiency while actually allowing the system to scale exposure faster than they can supervise. Margin accounts can also produce losses greater than the amount invested and forced liquidations if equity falls too far.[^7]

What is strategy drift in an AI-driven trading workflow?

Strategy drift is when the live system gradually stops behaving like the strategy the investor believes they deployed. That can happen because of prompt changes, model updates, new data inputs, brokerage rule changes, market regime shifts, or the investor quietly loosening constraints after a period of good performance.

How does autonomous execution affect gap risk?

Gap risk does not disappear under automation. In some cases it becomes more dangerous. Stops may fill far from expected levels, liquidity can vanish, and a system that assumes orderly execution may fail exactly when markets open sharply lower, halt, or reprice too quickly for planned exits to work cleanly.[^2][^3]

What minimum safeguards should exist before allowing AI to place trades?

At minimum, investors should have hard limits on order size, daily loss, open exposure, leverage, and symbol concentration; independent kill switches; clear human review thresholds; logging and alerts; paper trading and staged rollout; and a defined incident-response process for unexpected orders or position behavior.[^4][^8]

Is full autonomous trading appropriate for most retail investors?

Usually not by default. Many retail investors benefit more from assistive or semi-automated workflows, where AI helps with research, monitoring, or trade preparation but not unrestricted execution. Full autonomy only makes sense if the investor can supervise the system, constrain its authority, and respond quickly when something breaks.