AI Meets the Power Grid: Where Data Center Demand Becomes Earnings Visibility—and Where It Doesn’t

AI data center demand is real. That is no longer the hard part of the story.

The harder question is where that demand actually becomes visible, durable earnings. Markets often talk about “grid exposure” as if it were one theme. It isn’t. A transformer supplier with qualified products in a tight market is in a very different position from an EPC contractor bidding labor-heavy work. Both are different again from a regulated utility that still needs capital approval and cost recovery.

That distinction matters because the path from a hyperscaler’s load announcement to reported earnings is long, regulated, and full of friction. Interconnection queues, transmission constraints, substation capacity, permitting, labor, and equipment lead times all affect when demand becomes revenue—and whether revenue becomes margin.[^1][^2]

The cleanest way to think about this is simple: follow the bottleneck, then follow the payment mechanism. The best beneficiaries are usually companies that control a real bottleneck and retain some pricing discipline, or utilities that can convert required investment into rate base under constructive regulation. Others may still see more activity. That is not the same as earnings visibility.

The AI-to-grid chain is longer than the market narrative suggests

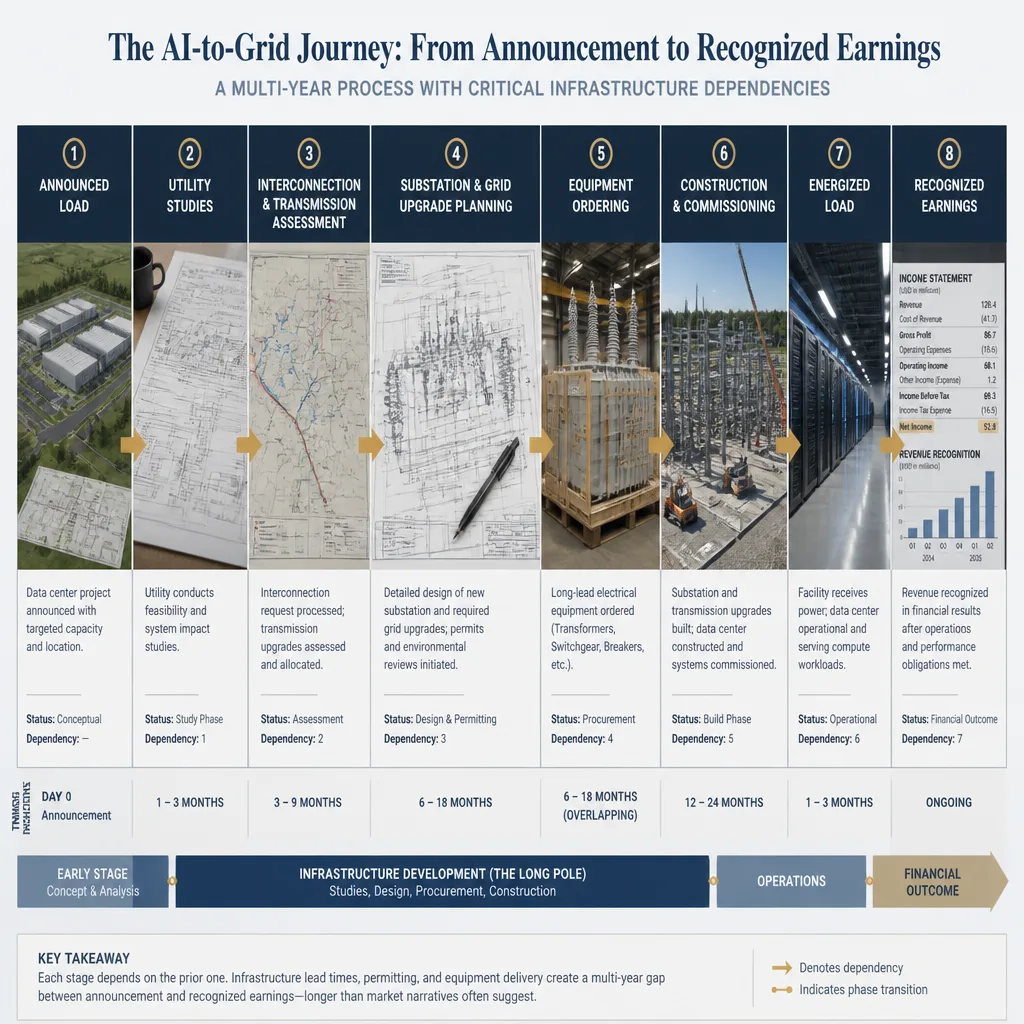

From data center announcement to energized load

A data center announcement is the start of the process, not the end of the investment thesis.

Between announcement and energized load, the chain usually looks like this:

load request -> utility studies -> interconnection and transmission assessment -> substation and grid upgrade planning -> equipment ordering -> construction and commissioning -> energization -> revenue and earnings recognition

Each step matters because different companies get paid at different points. A utility may not earn much until capex is approved, spent, placed in service, and folded into rate base. An equipment vendor may book backlog earlier, but shipment timing, cancellation terms, and product mix still determine when that backlog becomes earnings. A contractor may show backlog growth quickly while margins barely move.

That is why “AI power demand” is not one trade. It is a sequence trade.

Why interconnection queues and transmission capacity are the first reality check

The first real filter is whether the grid can serve the load on schedule.

Across major U.S. regions, interconnection and transmission processes remain congested. FERC has spent years trying to improve queue processing, but the underlying issue is structural: more load and generation requests are competing for systems that often need upgrades before they can absorb either.[^1] Regional operators such as PJM, ERCOT, and MISO regularly publish planning and queue materials that make the same point in different ways: timing is constrained by studies, upgrade requirements, and regional bottlenecks.[^3]

For investors, the key insight is simple: demand can be real and still fail to monetize on the expected timeline.

A hyperscaler may want a campus in 2027. If the utility needs a new substation, transmission reinforcement, and long-lead transformers, that load may slip. The project may still happen. But the earnings timeline for utilities, suppliers, and contractors moves with the grid, not with the press release.

The timing gap between signed leases, utility requests, and recognized earnings

This gap is where a lot of thematic enthusiasm breaks down.

An announced campus can lift utility stocks, electrical OEMs, and construction names at once. In practice, the first hard evidence often appears elsewhere: a large-load service request, a transmission planning document, a substation filing, or capex added to an integrated resource plan. Those signals matter more than a headline because they show conversion.

A useful investor sequence is:

announced load -> requested load -> contracted load -> approved infrastructure -> booked backlog -> shipped product -> in-service asset -> recognized earnings

Each step removes a layer of speculation.

A simple investor framework: volume exposure vs. bottleneck power vs. regulated return

Most of the value chain fits into three buckets.

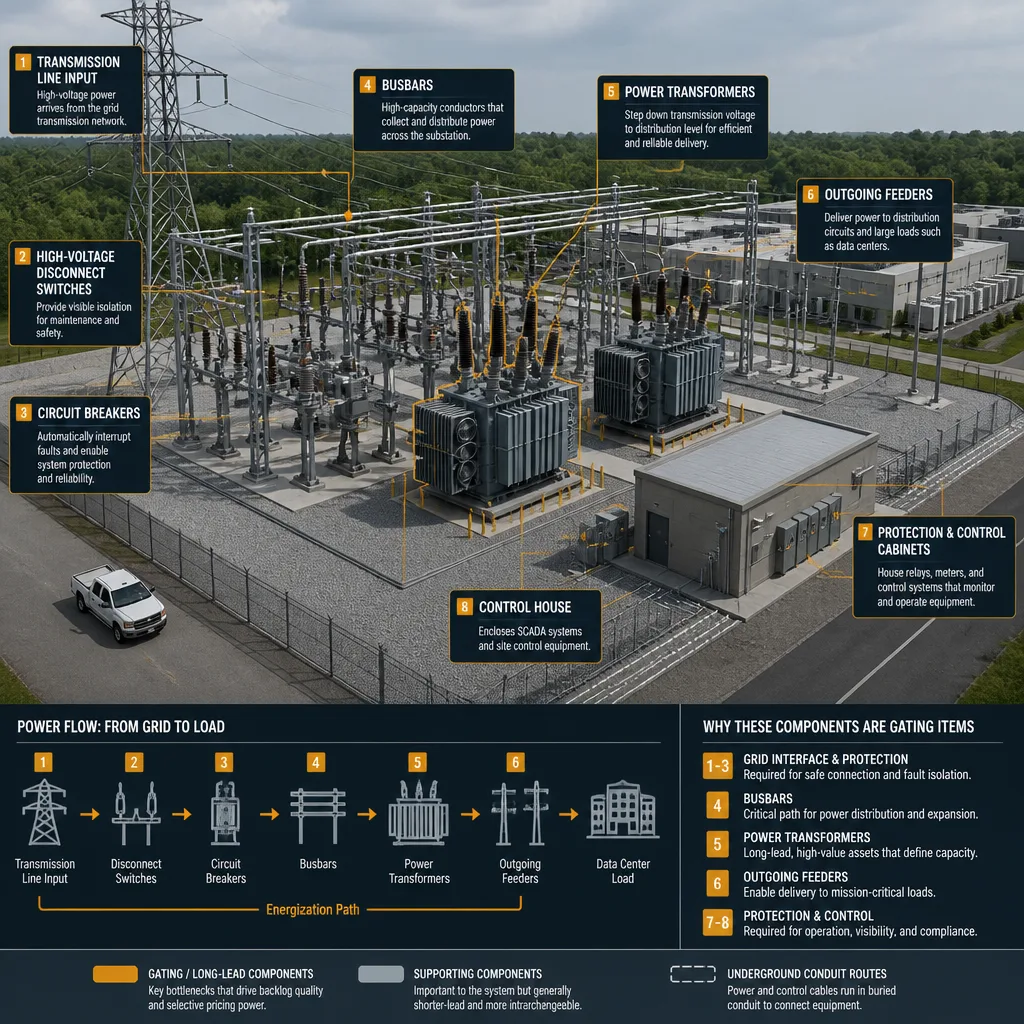

The first is bottleneck suppliers. These companies sell equipment that is hard to substitute, slow to qualify, and constrained enough to support backlog quality and some pricing discipline. Think selected utility-grade transformers, high-voltage switchgear, breakers, and protection-and-control systems.

The second is regulated capital converters. These are utilities and transmission owners that can turn growing load into approved capital investment and then into rate base. Their upside depends less on spot pricing power and more on approved spending, allowed returns, rider mechanisms, and the speed of recovery.

The third is volume-only participants. These companies benefit from more projects moving through the system, but they do not necessarily capture much incremental profit. EPC firms, broad construction services, and commodity-like electrical balance-of-plant often land here.

This framework is more useful than asking who “has AI exposure.” The better question is: where is the bottleneck, who gets paid to relieve it, and under what mechanism does that payment become earnings?

Where earnings visibility is strongest

Transformers and critical electrical components

Transformer exposure is not uniformly attractive. The better economics tend to sit in categories with long qualification cycles, utility-grade reliability requirements, and manufacturing constraints.

That is why “transformers” as a headline can mislead. A standardized product may benefit from volume but remain competitive. A higher-voltage or heavily specified product with fewer approved suppliers is more likely to support stronger pricing and better backlog visibility.

This is one of the clearest cases where scarcity matters. If a utility or data center project cannot move forward without a specific class of equipment, the supplier has leverage. But investors still need to separate true margin expansion from inflation pass-through. If pricing rises and margins stay flat, the company may simply be preserving economics, not capturing scarcity rents.

That is still better than commoditized exposure. It just is not the same as structurally higher returns.

Switchgear, breakers, and grid control equipment

Switchgear is similar, but more selective.

The attractive part of the market is not “all switchgear.” It is the subset where certification, installed-base compatibility, outage costs, and reliability make substitution painful. Utilities and large-load customers do not treat mission-critical protection systems like generic electrical boxes.

That creates a practical moat. If the cost of failure is high, buyers optimize for reliability and qualification, not just price. That can support healthier margins and more stable backlog than lower-end electrical products.

Still, scarcity here is at least partly cyclical. If manufacturers expand capacity and lead times normalize, pricing power can narrow faster than the market expects. Confidence in near-term demand is fairly high. Confidence in the duration of excess returns is lower.

Utilities with credible load growth and approved capital plans

Utilities may offer the most durable earnings visibility, but only when three things line up:

- The load is credible.

- The capital need is identifiable.

- The regulatory framework allows timely recovery.

That sounds obvious, but many “AI utility beneficiary” narratives skip the second and third steps.

The best evidence usually comes from utility filings, not investor slogans: integrated resource plans, transmission plans, rate cases, large-load tariff discussions, and capex updates tied to substations, transmission, and generation.[^4][^5] A service territory with rising large-load requests is interesting. A filed and approved plan to invest against that load is much more valuable.

Utilities also have a built-in limit. They do not usually earn scarcity margins. They earn allowed returns on approved capital. That can be attractive because it is durable, but the bridge takes time. Rate lag, prudence reviews, and political sensitivity around retail bills can all slow conversion.

Customer concentration is another underappreciated risk. If a few hyperscalers account for much of the growth outlook, delays or renegotiations matter more than headline load numbers suggest.

Where the story is real but margins may disappoint

EPC and construction services

EPC firms may be among the most visible volume beneficiaries, but that does not make them the best earnings beneficiaries.

This is a classic case where backlog can look strong while economics remain mediocre. Labor-heavy execution, subcontractor inflation, fixed-price exposure, schedule penalties, and permitting delays all limit margin expansion. In some contracts, the upside is mostly pass-through volume.

That is why backlog quality matters more than backlog size. Investors should ask whether backlog is repricable, margin-accretive, and tied to projects with firm power access and financing. If not, rising backlog can increase execution risk faster than profit.

Commodity-like electrical balance-of-plant

Electrical balance-of-plant can benefit from rising project activity, but this is often where the market over-extrapolates.

More volume can lift utilization. It does not automatically create pricing power. Unless a supplier has local market concentration, certification advantages, or bundled-service leverage, the economics often remain competitive.

This is the part of the theme where revenue enthusiasm most often outruns earnings reality. It is not a fake story. It is just a lower-quality one.

Generation equipment and turbines

Generation is probably the easiest place to tell the right story too early.

Yes, incremental data center load can support new generation requirements, whether through utility buildouts, peakers, or behind-the-meter solutions. But turbine OEM earnings depend on much more than demand in megawatts. Manufacturing slots, site permitting, emissions constraints, financing, grid connection, and long-term service attachment all matter.

A turbine order is not the same as near-term earnings. A manufacturing slot is not the same as a completed project. And a project without attractive service economics may be less valuable than the headline suggests.

For investors, this category often belongs in the medium- to longer-duration bucket rather than the immediate-beneficiary bucket.

The constraints that cap returns even when demand is genuine

Permitting and siting delays

Permitting is not a side issue. It can determine whether capacity additions happen on a market-relevant timeline at all.

Transmission, substations, and new generation all face local opposition, environmental review, land issues, and overlapping state and federal approvals. That means even strong demand can sit in the system longer than equity markets initially assume.

Skilled labor shortages

Labor is another real cap on monetization.

Substation work, utility construction, commissioning, and specialized electrical engineering are not infinitely scalable. Equipment can arrive on time and projects can still slip if the labor stack is not there. That tends to hurt contractors first, but it also pushes out energization across the chain.

Transformer, switchgear, and substation equipment lead times

Long lead times support some bottleneck economics, but they also cap system-level returns.

If a project is waiting on transformers or high-voltage gear, the supplier may benefit. Everyone else downstream may simply wait. That distinction matters: a bottleneck can create profit for one node while delaying earnings for several others.

Regulatory lag, cost recovery disputes, and customer concentration risk

For utilities, regulation is both the opportunity and the constraint.

A jurisdiction with constructive riders or timely recovery can convert grid investment into earnings with reasonable visibility. A slower or more contentious process can leave the same utility with real demand but weaker near-term EPS conversion.

That is why broad statements about “utilities winning from AI” are too loose. The right lens is jurisdiction-specific.

What investors should actually track

If the theme is real, the evidence should move through the chain.

Start with public signals from utilities and grid operators: interconnection materials, large-load service requests, transmission planning, and regional commentary from PJM, ERCOT, and MISO.[^3]

Then move to utility filings: capex tied to transmission, substations, and generation; integrated resource plans; special tariff discussions; rate cases; and disclosures around contracted versus merely requested load.

For suppliers, watch book-to-bill, backlog duration, lead times, cancellation language, and whether margin progression exceeds cost inflation. A company claiming tight supply but showing no margin improvement may have preservation, not pricing power.

Finally, track sequencing milestones. Substation awards, transmission upgrades, onsite generation planning, commissioning updates, and energization dates often tell you more than generalized AI commentary.

If you want one test, use this: is the story moving from announcement to approval to shipment to in-service earnings? If not, the market may be paying for narrative rather than conversion.

Counterpoint: why some apparent bottlenecks may not stay profitable

The bullish bottleneck argument is real, but it has limits.

Scarcity attracts capacity. Manufacturers add lines, customers diversify sourcing, competitors enter niche categories, and procurement teams learn where they can standardize. That can compress margins even while volumes remain healthy.

There is also demand-side risk. AI power forecasts may prove directionally right but too aggressive on timing. Better chip efficiency, slower model deployment, campus delays, or more disciplined hyperscaler spending could reduce the urgency of some projected buildouts.

And some apparently commoditized suppliers can outperform if they have hidden advantages: local dominance, installed-base compatibility, unusual certifications, or contract structures that protect margins better than the category stereotype suggests.

So this framework should be a starting point, not a rigid label. Categories matter, but company-specific economics still decide the outcome.

Conclusion

AI-driven data center power demand is a real structural force, but it does not create equal profit pools across the grid.

The strongest earnings visibility usually sits in two places: companies relieving genuine bottlenecks with qualification-driven pricing power, and utilities that can turn credible load growth into approved rate-base expansion. The weakest visibility tends to sit with participants that benefit from rising spend without controlling a constraint or a recovery mechanism.

The practical takeaway is straightforward: follow conversion, not announcements. Track where load becomes a service request, where a request becomes approved infrastructure, where infrastructure becomes backlog, and where backlog becomes in-service earnings. The theme is real. The dispersion inside it is the opportunity.

FAQ

Which parts of the power value chain are most likely to benefit from AI data center demand?

The strongest candidates are usually true bottleneck suppliers and regulated utilities with approved capital plans. In practice, that can include selected transformer makers, high-voltage switchgear and control equipment vendors, and utilities that can turn large-load growth into rate-base expansion. The weaker beneficiaries are often companies with volume exposure but limited pricing power.

Why doesn’t a data center announcement immediately translate into earnings?

Because the chain is longer than the headline suggests. A project typically moves from load request to utility studies, interconnection review, transmission or substation upgrades, equipment procurement, construction, commissioning, and only then to energized load. Revenue recognition and earnings visibility arrive at different points for utilities, equipment suppliers, and contractors.

Why are interconnection queues and transmission constraints so important to investors?

They are gating variables, not side details. If a utility or grid region cannot deliver power on schedule, the project may be delayed, resized, or relocated. That means demand may exist in theory but not convert into backlog, shipments, rate base, or earnings on the timeline investors expect.

Do transformer and switchgear shortages automatically lead to higher margins?

Not always. Tight supply can support better pricing and stronger backlog quality, especially in qualified, utility-grade categories with long lead times. But margin expansion depends on product mix, qualification barriers, contract terms, and whether price gains exceed cost inflation. Scarcity can protect economics without creating lasting excess returns.

Are utilities clear winners from AI-related power demand?

Only selectively. Utilities can offer strong visibility when three conditions align: the load is credible, the required capital investment is identifiable, and regulators allow timely recovery. If approvals lag, customer concentration is high, or political resistance grows around rate impacts, the earnings bridge weakens.

Why might EPC and construction firms see revenue growth without strong profit growth?

Because those businesses are often labor-intensive, competitively bid, and exposed to schedule risk. Backlog can rise quickly while margins stay capped by fixed-price contracts, subcontractor costs, labor shortages, weather delays, and pass-through structures that limit incremental profitability.

What should investors track to verify that AI-power demand is really converting into earnings?

Watch the sequence: large-load service requests, interconnection and transmission milestones, utility capex plans, rate case and integrated resource plan filings, supplier book-to-bill and backlog quality, lead times, shipment timing, margin progression, and in-service asset growth. The key is conversion, not announcement volume.

What could weaken or delay the AI-power infrastructure thesis?

Several things: slower hyperscaler buildouts, efficiency gains that reduce power intensity, permitting delays, labor shortages, component lead-time normalization, weak backlog quality, regulatory pushback, and customer concentration risk. Even when long-term demand is real, timing and returns can disappoint.