AI in Portfolio Management for Client Accounts: Where It Helps and Where It Creates Liability

AI is entering investment workflows the way most tools do: first as a curiosity, then as a productivity promise, and eventually as a governance problem.

For portfolio managers, RIAs, and family offices handling client money, that last stage matters most. The issue is not whether AI can produce useful output. It can. The issue is whether the output is supportable, reviewable, and consistent with fiduciary, supervisory, and recordkeeping obligations when real client accounts are involved.[^1][^2]

That distinction changes the analysis. In practice, AI is often most useful when it reduces information friction by summarizing, organizing, flagging, and monitoring. It becomes far riskier when it starts generating recommendations, rationales, or client explanations that sound polished but are not grounded in verified facts or actual portfolio judgment.

AI can help in portfolio management, but only if you separate assistance from judgment

The clearest way to think about AI in client-account management is simple: it works best as a copilot for handling information and worst as an autonomous advice engine.

That sounds obvious. It is also where firms get into trouble.

A model can summarize a 10-Q, compare policy statements, or flag an unusual change in factor exposure. Those are useful capabilities. But speed is not judgment, and fluency is not accountability.

The core distinction: support the decision-maker, do not replace the decision-maker

In a regulated investment process, AI usually adds value by narrowing the field of attention. It helps analysts and portfolio managers get to the relevant documents faster, scan more material, and surface issues that deserve review.

That is very different from asking a model to decide what a client should own, why a portfolio should change, or how a recommendation should be explained.

The first use supports human judgment. The second tries to substitute for it.

Why fiduciary context changes the standard

In many business settings, a plausible draft may be acceptable if someone cleans it up later. In portfolio management, that standard is too loose.

Advice and communications tied to client assets have to be more than plausible. They have to be accurate, consistent with the client’s mandate, and defensible under review. The SEC’s fiduciary framework for investment advisers does not disappear because part of the workflow ran through an AI tool.[^1] Nor do supervision, books-and-records, confidentiality, and anti-fraud concerns vanish because a vendor labels its product intelligent.[^2][^3]

A plausible answer is not a compliant answer.

Where AI genuinely helps

The safer use cases tend to share three features: the task is bounded, the inputs are visible, and a human can verify the output against primary evidence without much ambiguity.

Summarizing filings, earnings calls, and macro releases

This is one of the strongest early use cases.

An analyst covering an industrial company can use an approved tool to review a current 10-Q and the latest earnings call transcript, then pull out changes in guidance, balance-sheet developments, and management commentary on margins. That can save real time.

But the time savings only matter if the workflow stays disciplined. Every material point that enters a research memo should be checked against the filing or transcript. If a summary says leverage rose because inventory built ahead of demand, that statement should be traceable to the source document, not trusted because it sounds right.

The sequence matters: AI-assisted summary first, analyst verification second, actual conclusion third.

Monitoring news and policy changes that may affect holdings

AI is also useful as a monitoring layer.

A portfolio team can use it to watch for sanctions developments, rating actions, management changes, litigation, dividend policy changes, or central-bank statements that may affect current holdings. This is less about prediction than triage.

The advantage is not that AI knows what the portfolio should do. The advantage is that it can surface signals faster than a human manually scanning everything.

Still, alerts are not conclusions. If a tool flags a policy headline affecting a defense contractor or bank holding company, someone still has to decide whether the news is actually material.

Flagging anomalies in exposures, concentrations, correlations, or mandate drift

This is another area where AI, or related ML-based systems, can be genuinely useful.

A balanced strategy may slowly pick up unintended concentration in a handful of correlated names. A quality-income mandate may drift toward more cyclicality than the PM intended. A good monitoring tool can flag changes in exposure, concentration, style drift, or breach risk before they become obvious in performance.

That is valuable because anomaly detection is a narrower problem than portfolio judgment. The system does not need to know what to buy. It only needs to identify what changed and where a reviewer should look.

Running compliance pre-checks before trades or model changes

AI can also help with compliance support, especially where the firm has explicit internal rules.

That might mean pre-checking a draft model update against concentration limits, restricted lists, watchlists, or mandate language. The key phrase is explicit internal rules. If the task is essentially pattern matching against a defined rule set, AI can reduce friction.

What it should not do is quietly decide that a borderline case is acceptable.

Why these use cases are safer

The common thread is not that AI is smart. It is that the task can be checked.

A reviewer can inspect the filing, transcript, holdings report, policy statement, or rule set and decide whether the output is accurate enough to use. That is what makes narrow AI use cases workable in investment operations.

Where AI creates liability quickly

The most dangerous uses are the ones that appear efficient because they collapse several steps at once: research, judgment, explanation, and recommendation. That is where control starts to break down.

Uncited investment claims and fabricated supporting facts

Large language models can produce investment prose that sounds analyst-grade while including invented figures, stale facts, or citations that do not exist.

In an investment setting, that is not a small drafting flaw. If a model misstates a margin outlook, debt covenant, or regulatory exposure, the error can flow into investment memos, committee materials, and client explanations.

Personalized recommendations without account context

This is where many firms should draw a bright line.

A model that suggests reallocating a taxable client from appreciated equities into municipals or alternatives may sound sophisticated. But unless the workflow incorporates cost basis, cash-flow needs, legal constraints, investment policy statement terms, liquidity considerations, concentration risk, and tax context, the recommendation is incomplete at best and unsuitable at worst.

General-purpose models do not inherently know the client account.

Auto-generated client communications that misstate the real rationale

This risk is easy to underestimate because the output often reads well.

Imagine a PM trims a position mainly for liquidity management. An AI-drafted client note says the sale reflects valuation discipline and risk budgeting. That explanation may sound reasonable, but it rewrites the investment record. It gives the client a rationale the PM did not actually rely on.

In wealth management, polished language can increase liability when the substance is wrong.

Treating AI output as approved research instead of draft input

A subtler failure mode appears when teams stop treating AI as draft material and start treating it as a shortcut to confidence.

That is the point where “help me scan this” turns into “this is probably good enough.” The problem is not only factual error. Fabricated reasoning, omitted context, or unsupported certainty can enter the process before anyone notices.

The bigger risk is often bad process, not one bad answer

This is the part many AI articles miss.

The largest liability may not come from one obviously flawed recommendation. It may come from a broken workflow: unapproved tools, no source verification, confidential data pasted into public systems, weak supervision, and records that no longer show how a decision was actually made.

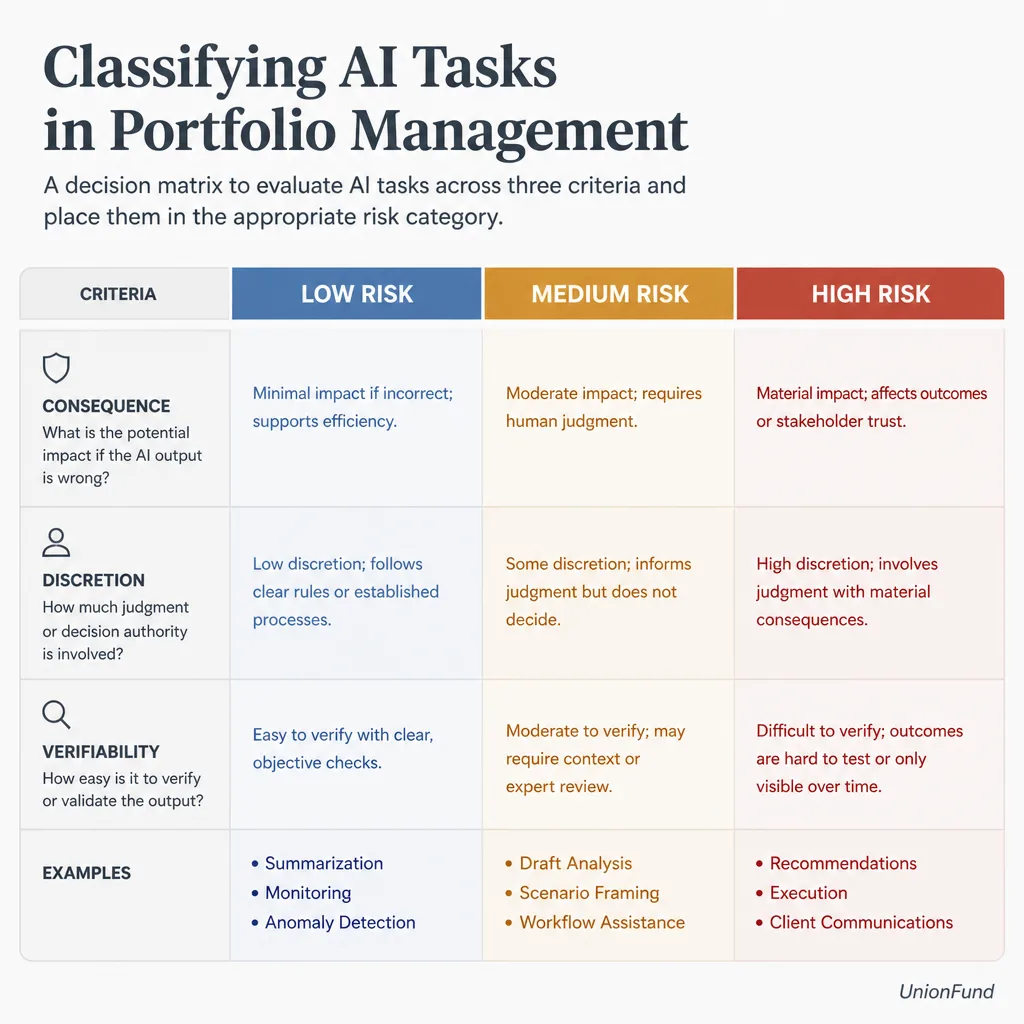

A practical rule: classify AI tasks by consequence, discretion, and verifiability

Firms do not need a 40-page policy to get started. They need a usable sorting rule.

Ask three questions:

- Consequence: What happens if the output is wrong?

- Discretion: Does the task require contextual investment judgment?

- Verifiability: Can a human reviewer check it quickly against primary evidence?

Low-risk tasks: information compression and detection

These are low-consequence, low-discretion, high-verifiability tasks.

Examples include:

- summarizing earnings calls and filings

- extracting changes from fund documents

- monitoring policy or company news tied to holdings

- flagging exposure anomalies

- checklist support for due diligence or compliance reviews

Medium-risk tasks: draft analysis under review

These can be useful, but they need tighter review because they can smuggle weak reasoning into the process.

Examples include:

- draft investment memos

- scenario framing

- internal brainstorming

- first-draft committee materials

- small analytics scripts or data-cleaning help

The output can save time, but only if reviewers treat it skeptically.

High-risk tasks: recommendations, execution, and client-facing explanations

These usually deserve prohibition or separate approval.

Examples include:

- client-specific allocation recommendations

- tax-sensitive rebalancing suggestions

- suitability analysis

- autonomous trade decisions

- automated order generation

- unreviewed client communications

- trade rationales written after the fact by a model

The fastest test

Can a human reviewer verify the output quickly against primary evidence?

If yes, the workflow may be manageable with controls. If no, because the task depends on judgment, hidden assumptions, or account-specific context, the use case is already in more dangerous territory.

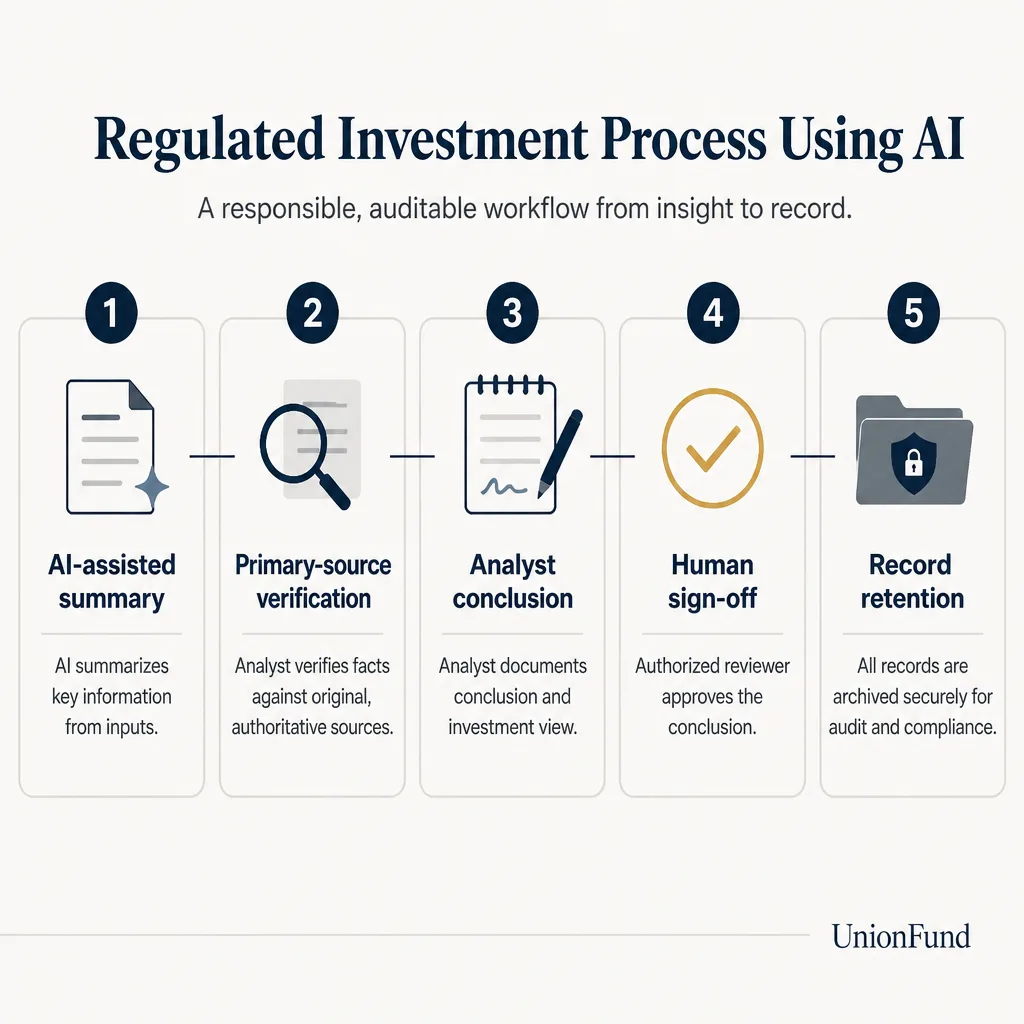

The verification workflow that makes AI usable

The point of verification is not to eliminate every error. It is to stop unverified output from quietly becoming part of the firm’s investment judgment.

Require primary-source citations for factual claims

If a factual statement matters to the thesis, risk view, or recommendation, it should point back to a primary source where possible: a company filing, earnings transcript, official economic release, approved market data source, fund document, or internal portfolio system.

If the tool cannot show its sources, the output should carry much less weight.

Separate AI-generated observations from analyst conclusions

This is a simple but strong control.

Label material clearly:

- AI-assisted summary

- Analyst verification notes

- Analyst conclusion

That makes it harder for unverified language to move downstream as endorsed research.

Require human sign-off before anything affects trades, model changes, or client communication

This should be non-negotiable.

If AI-assisted output touches investment committee materials, trade decisions, model changes, or client-facing explanations, a human reviewer should approve the final content and own it.

Maintain prompts, outputs, edits, and approvals when they form part of the investment record

Exact retention obligations depend on firm structure, jurisdiction, and workflow. But as a practical control, if AI materially informs research, supervision, or communications, firms should consider keeping:

- prompts

- source links

- output versions

- reviewer edits

- approval notes

- final approved use

If you cannot reconstruct how the output was reviewed, you are relying on a process you cannot defend.

Treat model error as operational risk

This mindset helps.

Model behavior can change. Vendors update systems. Retrieval sources may be incomplete. Reviewers may become less careful over time. Those are operational risks, not just drafting issues. The NIST AI Risk Management Framework is useful here because it frames AI in terms of governance, reliability, explainability, privacy, and accountability, not just performance.[^4]

Recordkeeping, audit trails, and vendor due diligence matter more than most teams expect

Many firms focus on the visible output and neglect the control environment around it. That is backwards.

What to retain

Not every interaction with an AI tool needs to become a formal record. But if an output materially shapes research, a recommendation, a supervisory review, or a client communication, the safer approach is to retain enough to show what happened.

That means preserving not just the final polished memo, but the path to it.

What to ask vendors

Before adoption, firms should ask a short list of basic but important questions:

| Area | What to ask |

|---|---|

| Data provenance | What sources does the tool use, and can users inspect them? |

| Retention | Are prompts and outputs stored, and for how long? |

| Training use | Is customer data used for model training? |

| Access control | Can permissions be limited by user or team? |

| Logging | Are activity logs exportable for audit review? |

| Model updates | How often does behavior change, and how are changes disclosed? |

| Explainability | Can the user see why a result was produced, or only the output? |

A specialized finance tool may be better than a general-purpose model in some respects, especially if it uses approved data and preserves source links. But specialization does not remove the need for verification.

Address confidentiality before rollout

One of the easiest preventable failures is also one of the most serious: employees pasting client names, holdings, tax details, or account constraints into consumer AI tools without approval.

That is not an AI strategy problem. It is a data-governance failure.

Firms should decide in advance which tools are approved, what data classes may be entered, whether prompts are logged, and whether outputs can flow into research systems, CRM platforms, or client materials.

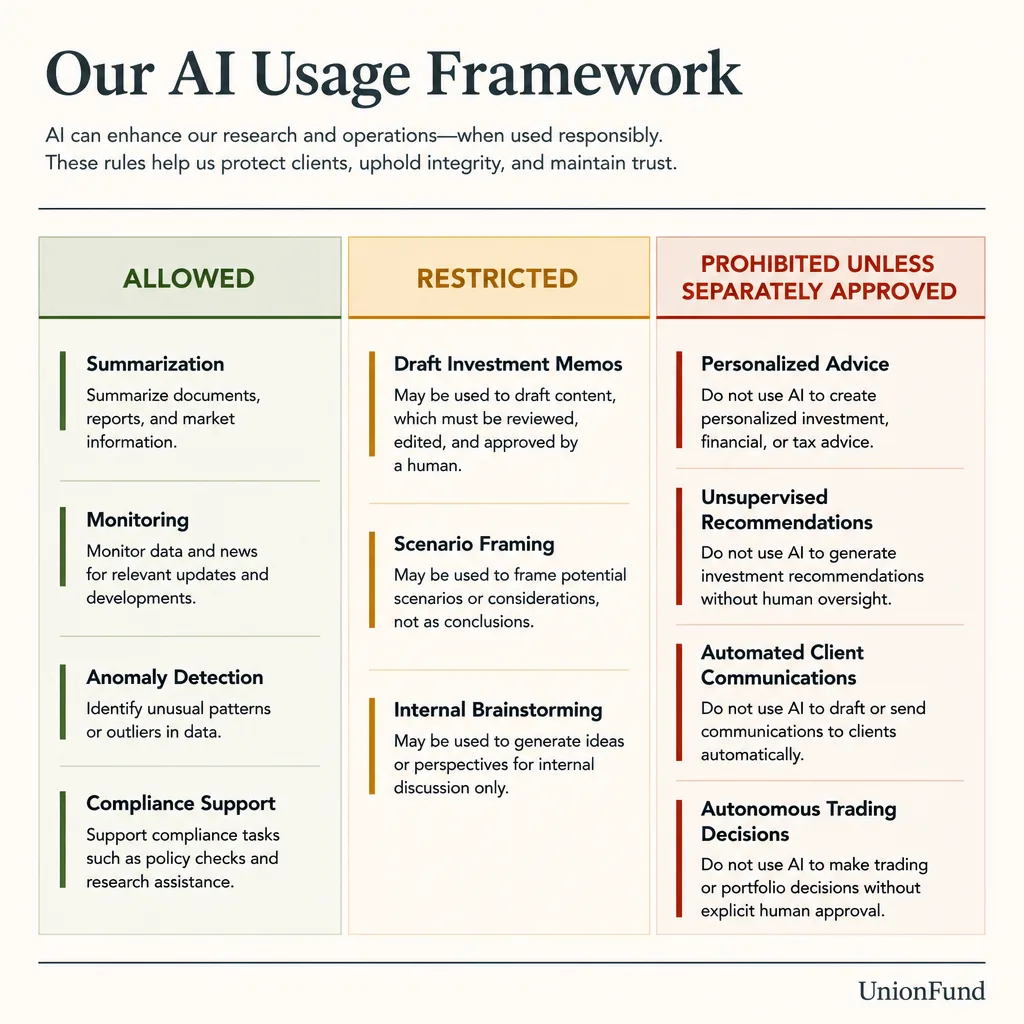

A simple internal policy: allowed, restricted, and prohibited uses

Most firms do not need a perfect policy before they start. They do need a clear one.

Allowed

These are the strongest candidates for early rollout:

- summarizing public filings and earnings calls

- comparing policy statements over time

- monitoring holdings-related news

- flagging concentration or mandate drift

- compliance checklist support tied to explicit rules

Restricted

These can be useful, but only with documented review:

- draft research notes

- sensitivity or scenario framing

- meeting preparation

- due-diligence question generation

- first-pass internal commentary

The rule is simple: no factual or judgment-heavy output moves forward unchecked.

Prohibited unless separately approved

For most firms, this list should be explicit:

- client-specific allocation recommendations

- suitability analysis by a model alone

- tax-aware rebalancing suggestions without approved workflow controls

- unsupervised portfolio changes

- autonomous order generation

- client communications sent without human approval

- post-hoc trade explanations generated by AI

Assign ownership clearly

Even small firms should define who owns what.

- PM/CIO: sets investment-use boundaries and approval thresholds

- Compliance: defines review, supervision, and retention expectations

- Operations/technology: manages access, logging, and system controls

- Legal/privacy, where applicable: reviews vendor contracts and data handling

Without ownership, “allowed” and “prohibited” quickly become theoretical.

The right posture is not “use AI” or “ban AI.” It is “govern it.”

The firms most likely to benefit first are not the ones making the boldest claims. They are the ones choosing narrow, high-verifiability workflows and supervising them well.

Why narrow, supervised use cases are the best starting point

A good pilot is not “let the team use AI and see what happens.” It is something smaller and testable.

For example:

- summarize ten historical earnings transcripts and measure source fidelity

- test whether exposure-alert workflows catch known anomalies

- compare gross time saved with net time saved after verification

- track hallucination rate, stale facts, and reviewer correction burden

That last point matters. The real benefit is not draft speed. It is net process improvement after controls.

What to do next

If you manage client accounts, the next step is fairly straightforward:

- Map where information friction is highest in your current process.

- Identify tasks with low consequence, low discretion, and high verifiability.

- Approve a narrow tool set.

- Define data boundaries before anyone starts improvising.

- Require source verification and human sign-off where output affects investment action or client communication.

- Scale only after you can show the process is actually safer and faster.

Broad autonomous use cases tend to create liability before they create efficiency.

Conclusion

AI has a real place in portfolio management for client accounts. But that place is narrower than the marketing suggests.

Used well, it can compress information, improve monitoring, and make investment workflows less tedious. Used poorly, it can introduce uncited claims, unsuitable recommendations, misleading client language, and a recordkeeping mess that leaves the firm unable to explain how a decision was made.

The useful distinction is simple: let AI reduce information friction, but do not let it impersonate fiduciary judgment. In client-account management, the right posture is controlled adoption with clear boundaries, verifiable evidence, and human accountability where it matters most.

FAQ

Can portfolio managers use AI in client-account management?

Yes, but the safer uses are narrow and verifiable. AI is generally more defensible as a copilot for research support, document summarization, monitoring, anomaly detection, and compliance pre-checks than as a source of investment judgment or client-specific advice.

Where does AI help most in portfolio management?

It tends to help most with information-heavy but bounded tasks: summarizing earnings transcripts and filings, monitoring policy or company developments affecting holdings, flagging unusual exposure changes, and organizing compliance or due-diligence workflows. These tasks are easier to review against primary sources.

What are the biggest AI risks for investment advisers and wealth managers?

The main risks are not just bad answers. They include fabricated facts, uncited claims, stale information presented as current, unsuitable personalized recommendations, misleading client communications, confidentiality failures, weak supervision, and poor recordkeeping.

Why is AI-generated investment advice higher risk than AI-assisted research?

Advice requires account-specific judgment, suitability review, mandate awareness, tax context, liquidity constraints, and human accountability. Research support is usually easier to verify. A plausible AI answer is not enough when client money and fiduciary duties are involved.

Should firms allow AI to generate client communications?

Only under tight controls, if at all. Auto-generated client notes can sound polished while misstating the real portfolio rationale, overstating certainty, or implying analysis the firm did not actually perform. Any client-facing output should require human review and approval.

How should firms verify AI-generated research?

A practical workflow is to require primary-source citations for factual claims, separate AI-assisted summaries from analyst conclusions, and require human sign-off before output influences trades, model changes, investment committee materials, or client communications.

What records should firms retain when AI is used in investment workflows?

If AI materially informs research, supervision, or communications, firms should consider retaining prompts, source links, output versions, reviewer notes, edits, approvals, and the final approved use. Exact retention duties depend on firm status, jurisdiction, and workflow, so compliance review matters.

What should investment firms ask AI vendors before adoption?

Key questions include where data comes from, whether customer data is retained or used for training, how access controls work, whether logs are exportable, how model updates are managed, whether sources are visible, and how the tool supports auditability and explainability.

Can a general-purpose AI model be used for portfolio recommendations?

That is usually a high-liability use case unless the workflow is tightly controlled and separately approved. General-purpose models do not inherently understand a client’s investment policy statement, tax situation, legal constraints, or suitability profile.

What is a simple rule for deciding whether an AI task is acceptable?

Use three tests: consequence, discretion, and verifiability. If the cost of being wrong is high, the task requires judgment, and the output cannot be quickly checked against primary evidence, the use case should be restricted or prohibited.